In the era of advancing digital transformation, the impact of the digital divide on residents’ financial behavior has garnered considerable attention, yet there exists a gap in understanding its implications for financial advisors. Employing the analytical framework of “access gap-usage gap-utility gap” and utilizing a Probit model with sample selectivity, this paper systematically explores the impacts, heterogeneity, and mechanisms of the three levels of the digital divide on the demand for and engagement with financial advisors among residents in six eastern provinces of China in 2022. Key findings are as follows: (1) The impact of the access gap isn't significantly, whereas the effects of the usage gap and utility gap are significantly negative. This implies that residents’ internet usage itself does not affect the likelihood of seeking and engaging financial advisors, but lower frequency and perceived importance of internet usage decrease the likelihood of seeking and engaging financial advisors. (2) Heterogeneity analysis reveals that the inhibitory effects of the usage gap and utility gap are more pronounced in rural households, those with debt, and householders lacking financial education. (3) Mechanism studies uncover that both the usage gap and utility gap diminish residents’ demand for and engagement with financial advisors by weakening social networks and reducing information attention. This study contributes to a deeper understanding of the profound impact of digital transformation on financial markets, offering policy suggestions and practical guidance to enhance financial services.

As is well-known, due to market incompleteness and the irrationality and limitations of individual cognition, individuals consistently find themselves unable to make rational financial decisions (Dalen et al., 2017; Liu & Lu, 2023; Rodrigues et al., 2019). Consequently, the majority of investors hold investment portfolios that are insufficiently diversified and rational, leading to lower investment returns and higher investment risks (Lu et al., 2020; MacDonald et al., 2023). Numerous studies have found that financial professionals, represented by financial advisors, aid individuals in avoiding making erroneous decisions (Fong & Lee, 2023). In fact, with the continuous development of economic levels and the general increase in wealth accumulation, residents' financial awareness is gradually strengthening. Consequently, there is a sustained increase in the demand for financial advisors among residents in pursuit of financial goals, wealth appreciation, and risk mitigation (Liu, 2023). Moreover, the ever-evolving nature of financial markets has increased the complexity of investment decision-making for ordinary investors, prompting many to seek personalized financial planning advice from professional financial advisors (Burke & Fry, 2019; Rodrigues et al., 2019). In sharp contrast, the proportion of residents expressing demand for financial advisors and actually hiring them is not particularly high (Amaral & Kolsarici, 2020; Liu & Lu, 2023). Consequently, understanding the factors influencing residents’ behavior regarding financial advisors has become a crucial area of investigation.

Early research on residents’ financial behavior predominantly centered on the allocation of financial products, demand for and engagement with financial or retirement planning. MacDonald et al. (2023) conducted a comprehensive review of the literature on the value of financial advice, revealing a predominant focus on financial benefits while lacking a holistic view of value and the factors impacting it. In recent years, some scholars have shifted toward emphasizing residents’ financial advisory behavior and analyzing influencing factors from various perspectives (Amaral & Kolsarici, 2020; Barthel & Lei, 2021; Bhattacharya et al., 2023; Burke & Hung, 2021; Kim et al., 2021). These factors encompass micro-level individual characteristics (such as gender, education level, financial knowledge, and social networks, etc.), meso-level family characteristics (such as household income, assets, and social networks, etc.), and macro-level contextual factors (including regional economic development, financial consumer protection, and policies and regulations).

With the proliferation of digital technology and the ensuing digital transformation of financial markets, individuals face increasingly intricate and diverse financial choices. Consequently, the demand for professional financial advisors is on the rise, with expectations that they can furnish personalized financial plans and investment strategies (Brenne & Meyll, 2020; Piehlmaier, 2022). However, concurrently, residents grapple with the adverse effects of the digital divide, significantly influencing their access to, understanding of, and ability to utilize financial advice. The digital divide refers to disparities in individuals’ ability to access, comprehend, and use digital information, encompassing imbalances in technological capabilities, digital literacy, and information acquisition channels (Lu et al., 2023). There is a compelling reason to believe that the digital divide imposes constraints on residents’ engagement with financial advisory services. On the one hand, disparities in individuals’ access to financial-related information, exacerbated by the digital divide, may hinder certain residents from easily acquiring relevant financial knowledge and information, thereby diminishing their likelihood of seeking financial advisory services (Lythreatis et al., 2022; Vassilakopoulou & Hustad, 2023). On the other hand, the digital divide might leave certain residents struggling to comprehend and apply complex financial concepts and data analysis, resulting in challenges in receiving financial advice and potentially making erroneous decisions (Aissaoui, 2022). Furthermore, the digital divide may impact individuals’ ability to leverage technological tools for financial management and advisory services, with some residents lacking the necessary skills and experience to utilize digital financial tools, thus facing barriers in accessing financial advisory services (Scheerder et al., 2017). Therefore, there is a pressing need for in-depth research on the effects to formulate targeted policies and measures, ensuring that all residents can fully benefit from professional financial advisory services.

Currently, China's “Digital China” strategy has led to continuous improvements in internet infrastructure. Despite these advancements, the proportion of Chinese residents expressing a need for financial advisors and those who actually engage financial advisors remains relatively low. According to the CHFS2019 database, merely 3.03 % of Chinese residents express a need for financial advisors, and among them, only 13.02 % have utilized financial advisory services (Liu & Lu, 2023). Is the digital divide influencing the demand for and engagement with financial advisors among Chinese residents? Does this influence vary across distinct levels of the digital divide and show heterogeneity across diverse demographic profiles? How does this influence manifest its effects? Answers to these questions are crucial. To address this research gap, this article utilizes survey data collected from residents in six provinces of East China in 2022 and employs the analytical framework of “Access gap-Usage gap-Utility gap” to systematically investigate the impact, heterogeneity, and mechanism of the digital divide on the demand for and engagement with financial advisors among residents. In this context, "Access gap" refers to the situation where residents, relative to internet usage, either have no access to or do not use the internet, thus experiencing an access gap. "Usage gap" pertains to the scenario where residents' overall frequency of internet usage is lower, indicating a more severe case of usage hap. "Utility gap" denotes that the lower the perceived importance of the internet among residents, the more severe the utility gap they experience. Compared to existing research, this paper introduces several innovations:

Firstly, a comprehensive analysis of residents’ financial advisory behavior necessitates considering two perspectives: the demand for and engagement with financial advisors. The demand for financial advisors reflects individuals’ cognitive needs and psychological expectations for financial advisory services, while engagement with financial advisors focuses on individuals’ choices and decisions regarding engaging in financial advisory services. When scrutinizing the factors impacting the decision to hire a financial advisor, overcoming the sample selectivity issue concerning the demand for financial advisors is crucial. However, prior research has often overlooked this issue. For example, Kim et al. (2021) used a Probit model to analyze the impact of financial literacy on the demand for financial advice and its influence on the selection of different sources of financial advice within the group with a demand for financial advice. However, due to sample selectivity issues, their estimation results may be biased. To address this issue, this paper introduces the Probit model with sample selectivity (referred to as the PSS model) for research purposes (Chaudhuri & Cheric, 2012; Liu & Lu, 2023), providing essential methodological insights for research in this field.

Secondly, a plethora of research indicates that the digital divide has severe adverse consequences on residents’ well-being, encompassing objective facets such as employment, income, assets, educational opportunities, physical health, and life participation prospects, along with subjective aspects like happiness, relative deprivation, mental health, and depression (Aissaoui, 2022; Goncalves et al., 2018; Lu et al., 2023; Lythreatis et al., 2022; Vassilakopoulou & Hustad, 2023). In recent years, despite some scholars beginning to concentrate on the ramifications of the digital divide on residents’ financial behaviors, such as asset allocation, retirement planning, or financial planning (Lythreatis et al., 2022; Yu et al., 2023), limited research has delved into financial advisory behavior. Therefore, the primary objective of this paper is to enrich the comprehension of the impact of the digital divide by scrutinizing its effects on residents’ demand for and engagement with financial advisors through theoretical hypotheses and empirical analysis.

Thirdly, it is crucial to acknowledge that the triad of digital division levels is not isolated but intricately linked through chain effects, with influences cascading from the initial to the ultimate tier (Wei et al., 2011). Despite researchers recognizing the existence of these three levels, constraints in available data have posed challenges in systematically gauging and characterizing the extent and status of the digital divide across all three tiers for individuals (Loh & Chib, 2021; Lu et al., 2023; Ragnedda, 2017; Scheerder et al., 2017; Zhao et al., 2022). In this study, we embrace the intricacies and variations within the digital divide and employ diverse perspectives to measure the usage and utility gap. Through this comprehensive approach, our aim is to furnish an exhaustive understanding and analysis of the prevailing state of the digital divide at various levels. Indeed, the usage gap delves into residents’ objective internet utilization patterns, while the utility gap encapsulates residents’ subjective assessments of internet usage. These two dimensions should not be conflated. Nevertheless, there exists a dearth of literature systematically investigating the impact of distinct levels of the digital divide on residents’ financial behaviors, with even fewer comparative studies on the repercussions for residents’ demand for and engagement with financial advisors. This paper strives to redress this research gap and fundamentally grapple with this issue.

Finally, there is scant literature scrutinizing the underlying mechanisms by which the digital divide shapes residents’ financial advisory behavior. In this context, this paper aspires to enhance comprehension by probing whether the digital divide influences the demand for and engagement with financial advisors through the extent of information attention and social networks. Undoubtedly, this approach adds to a more holistic examination of this domain.

The remaining sections of the paper are organized as follows: Chapter 2 conducts a review of the existing literature, followed by the research hypotheses. Chapter 3 will introduce the data sources, followed by the construction of variables. In Chapter 4, we will initially present the baseline estimation results, followed by robustness checks, heterogeneity analysis, and mechanism tests. Chapter 5 will initiate with a “discussion” section, offering insights from both academic and policy perspectives. Finally, a succinct summary of the conclusions will be provided, followed by the identification of limitations and suggestions for potential areas of future improvement.

Literature review and hypothesisLiterature reviewThe concept and measurement of digital divideEarly research on the digital divide primarily focused on the access level, which examined the gap between individuals with internet access and those without it, based on material conditions. This first level digital divide, also known as the digital access divide or access gap, primarily revolves around internet device ownership and internet accessibility (Van Dijk, 2006). As internet infrastructure improved and access gaps narrowed, scholars shifted their attention to the usage level. They found that even with equal access, individuals might not use the internet in the same way or to the same extent. This variation in internet usage is evident in factors such as content, skills, motivation, frequency, and preferences (Liao et al., 2022; Loh & Chib, 2021; Lythreatis et al., 2022; Scheerder et al., 2017). This distinction in internet usage patterns is referred to as the second level digital divide. Existing literature predominantly centers on two main categories: one underscores the frequency of internet usage, often termed as the “usage gap,” while the other highlights internet usage skills, commonly referred to as the “digital capability divide” (Lu et al., 2023).

In recent years, some scholars have expanded their research to focus on the “effect” level, studying differences in cognition, attitudes, values, and behavioral patterns among populations after accessing and using the internet. This concept is known as the third level digital divide. However, there is still some controversy surrounding this concept. Some scholars emphasize analyzing the objective consequences of internet use, such as the inequalities in work, learning, entertainment, and interpersonal relationships caused by differences in internet access or usage, and they refer to it as the digital outcome divide (Scheerder et al., 2017; Zhao et al., 2022). Others highlight the subjective utility difference in internet usage, which pertains to differences in perceived importance, and they refer to it as the utility gap (Gómez, 2018; Ragnedda, 2017).

Factors influencing residents’ financial advisory behaviorRecently, some scholars have identified various factors influencing residents’ financial advisory behavior from different perspectives. For example, Amaral and Kolsarici (2020) observed a significant inverse correlation between the likelihood of seeking advice from a financial planner and investment in financial literacy. Brenner and Meyll (2020) identified a robust negative relationship between the utilization of robot-advisors and the inclination to seek human financial advice. Barthel and Lei (2021) investigated the association between cognitive ability and the propensity to seek financial advice, revealing no significant relationship between three dimensions of cognitive ability (memory, objective numeracy, and subjective numeracy) and the pursuit of financial advice. Burke and Hung (2021) discovered a correlation between financial trust and the usage of advice as well as the inclination to seek advisory services. Piehlmaier (2022) found that investors exhibiting overconfidence display a notably higher tendency to adopt robot-advice. Bhattacharya et al. (2023) revealed gender disparities in advice provision within financial planning firms, with women being more inclined than men to receive advice regarding individual or local securities, a trend not observed in securities firms. Delis et al. (2023) demonstrated that hard priming elicits a heightened positive intention to consult a bank advisor. Fong and Lee (2023) investigated the impact of consumers’ trust in financial institutions on both their seeking and adopting behaviors of financial advice, establishing financial trust as a potent predictor of both behavioral outcomes. Liu (2023) identified essential factors such as subjective norms, financial knowledge, financial risk tolerance, and personal traits as positively influencing an individual's decision to seek advice from financial planners, while financial stress stemming from financial constraints exerted a significant negative effect. Liu and Lu (2023) concluded that heightened levels of financial literacy positively impact both the demand for and employment of financial advisers.

Regrettably, prevailing literature seldom segregates subjective demand from actual engagement behavior within residents’ financial advisory conduct, not to mention amalgamating the two within a holistic analytical framework. Moreover, there exists a dearth of research delving into the ramifications of the digital divide on residents’ financial advisory behavior, let alone juxtaposing these consequences across various tiers of the digital divide and elucidating the underlying mechanisms.

HypothesesThis article posits that the digital divide has adverse effects on both residents’ demand for and engagement with financial advisors. The primary rationales are outlined as follows: (1) The digital divide results in inequalities in information access (Ragnedda, 2017; Vassilakopoulou & Hustad, 2023). Residents with limited digital literacy or constrained internet access face difficulties in accessing up-to-date financial information and market trends. This informational gap makes them less acquainted with new financial products and investment opportunities, reducing their inclination to seek guidance from financial advisors.(2) The digital divide may contribute to deficiencies in digital financial literacy among certain residents, indicating a lack of understanding and proficiency in utilizing financial technology tools and digitalized financial methodologies (Aissaoui, 2022). Consequently, there is a decreased receptivity towards digital financial services, with individuals perceiving offerings from financial advisors as overly complex or daunting, thereby avoiding seeking guidance from financial advisors. (3) The digital divide may hinder interaction and communication between residents and financial advisors (Lythreatis et al., 2022). For those unfamiliar with digital communication tools, engaging remotely with financial advisors may seem cumbersome or arduous. Face-to-face communication may require proximity in time and geography, presenting challenges for residents residing in remote locales or with limited mobility. Moreover, concerns about the security and reliability of online financial services may further reduce residents’ willingness to seek assistance from financial advisors. As a result, this study proposes hypotheses H1a and H1b as follows:

H1a The digital divide at different levels exhibits a negative impact on the demand for financial advisors, including the access gap, usage gap, and utility gap. This implies that residents who do not use the internet, have lower internet usage frequency, and perceive the internet as less important, are less prone to seek financial advisors.

H1b The digital divide at different levels exhibits a negative impact on the engagement of financial advisors. This suggests that residents who do not use the internet, have lower internet usage frequency, and perceive the internet as less important, are less likely to engage financial advisors.

Firstly, this paper posits that the digital divide undermines residents' social networks due to the following reasons (Aissaoui, 2022; Hooghe & Oser, 2015; Lu et al., 2023): (1) In the contemporary digital era, social networks predominantly flourish on internet-based platforms, fostering information exchange through online social media and communities. However, residents lacking digital literacy or convenient internet access face barriers to participating in these networks, leading to uneven access to information. Consequently, their connection to digital social networks weakens, limiting avenues for communication and interpersonal connection. (2) The digital divide may create barriers to digital socialization for certain residents. Those unfamiliar with digital communication tools may perceive online social media and communities as unfamiliar and unreliable, resulting in a decreased inclination for active engagement. These barriers impede interaction and communication, affecting the growth and strength of social networks. (3) Unequal access to information and obstacles to digital socialization stemming from the digital divide may cause certain residents to experience detachment from digital social networks, fostering feelings of digital isolation. This gradual alienation diminishes their presence within social networks, leading to reduced interaction and weakening the breadth and density of these networks. (4) The digital divide may intersect with social cognition and cultural dynamics, sparking biases or misconceptions towards digital social networks. Some residents may perceive traditional modes of socialization as more dependable and trustworthy, viewing digital social media and online communities with skepticism or distrust. This sociocultural influence diminishes residents' desire to engage in digital social networks, hindering their expansion and reinforcement.

Furthermore, the enhancement of residents’ social networks serves as a catalyst in facilitating the demand for and engagement with financial advisors owing to the following reasons (Chaudhry et al., 2022; Fong & Lee, 2023; He & Li, 2020; Heimer, 2016):(1) Social networks act as conduits for the dissemination and exchange of financial insights. Improved social networks enable residents to share and access financial information among peers through platforms like social media, online communities, and digital forums. This facilitates the spread of financial knowledge, enhancing residents’ awareness of their financial circumstances and predisposing them to seek guidance from financial advisors. (2) The amplification of social networks fosters the exchange of professional acumen and expertise. Residents may connect with individuals possessing substantial financial prowess or a background in finance, gaining nuanced counsel on investments and financial strategies. This knowledge-sharing dynamic could as the potential to drive an increased demand for financial advisors as residents recognize the potential for professional advisors to provide tailored and comprehensive financial planning services. (3) The reinforcement of social networks bolsters social influence and fosters trust-based relationships among residents. Active engagement with financial advisors within social spheres allows resident to share positive experiences, enhancing faith and rapport with financial advisors. This social endorsement increases the inclination to enlist financial services. (4) Within social networks, individuals are influenced by the conduct and attitudes of their peers. As certain residents benefit from financial advisors’ services and achieve commendable financial outcomes, others may be inspired to seek similar professional assistance. This ripple effect can lead to the proliferation and permeation of the demand for financial advisors within social networks. Therefore, hypothesis H2 is proposed as follows:

H2 The digital divide exerts a suppressing effect on the demand for and engagement of financial advisors among residents by weakening their social networks.

This paper contends that the digital divide hampers residents' information attention levels due to the following factors (Aydin, 2021; Chetty et al., 2018; Vassilakopoulou & Hustad, 2023): (1) The digital divide creates scenarios where certain residents cannot access the latest information disseminated through digital channels like the Internet and social media. Residents lacking digital literacy or convenient internet access face challenges in accessing relevant information, constraining their ability to attend to news, current events, and other critical information. (2) The digital divide may leave some residents with a deficit in digital literacy, marked by a lack of proficiency in information and communication technologies. In an era heavily reliant on digital platforms for information dissemination, individuals unfamiliar with these technologies may have difficulty navigating the vast repository of information available online, resulting in diminished attention to pertinent such information. (3) While some residents may possess adept digital literacy skills, the sheer vastness of information in the digital age can lead to information overload and decision paralysis. Confronted with a deluge of information sources and content, residents may find themselves overwhelmed, making it challenging to discern and prioritize relevant information. Consequently, individuals may choose to limit their attention to information or limit their focus to a few familiar sources while disregarding others.

Furthermore, the enhancement in residents’ information attention levels sparks an upswing in the demand for and engagement with financial advisors, driven by the following rationales (Liu & Lu, 2023; Nekrasov et al., 2023; Sicherman et al., 2016): (1) With heightened information attention, residents demonstrate a propensity to actively seek the latest financial insights and professional expertise. Gaining knowledge about financial market dynamics, intricacies of investment products, and strategies for financial planning enhances residents' financial acumen and understanding. This increased awareness enables residents to discern their financial imperatives and aspirations more discerningly, thus amplifying their inclination to seek guidance from financial advisors. (2) The elevation in information attention leads to an increase in residents' demand for financial planning services. Heightened awareness of their financial standing and future objectives compels residents to strive for financial growth and risk mitigation through thoughtful financial planning. In this context, residents exhibit an enhanced predisposition to engage professional financial advisors for personalized financial counsel and planning. (3) By intensifying their focus on information, residents cultivate a profound understanding of the intricacies and sophistication inherent in the realm of finance. Recognizing the challenging nature of navigating complex investment landscapes and volatile financial markets independently, residents display an increased openness to seeking assistance from seasoned financial advisors. Equipped with expertise, financial advisors provide residents with tailored financial solutions aligned with their risk tolerance and financial objectives. (4) Augmented information attention equips residents with a nuanced understanding of the intricacies associated with various financial alternatives, enabling them to systematically evaluate risks and returns. This heightened proficiency instills confidence in residents' financial decision-making abilities, fostering a greater inclination for active engagement in financial endeavors. Simultaneously, residents demonstrate an increased propensity to seek the professional insights and guidance of financial advisors in making prudent financial choices. Therefore, this article proposes the following hypothesis H3:

H3 The digital divide exerts a suppressing effect on the demand for and engagement of financial advisors among residents by diminishing their level of information attention.

The data for this study was initially gathered during the Chinese New Year period in 2022 and subsequently augmented through additional surveys conducted between July and September 2022. The survey predominantly focused on soliciting pertinent information concerning households in the year 2021, incorporating a retrospective analysis of various crucial aspects dating back to 2019, encompassing provinces such as Jiangsu, Shandong, Anhui, Zhejiang, Jiangxi, and Fujian. The survey team predominantly comprised young faculty members, graduate students, and undergraduates from the author's university and collaborating institutions. The selection of the East China six provinces is underpinned by various factors. Primarily, this region stands out as one of China's economically prosperous areas, distinguished by a high urbanization rate and relatively elevated per capital income levels. Furthermore, it boasts a notable level of engagement in financial markets and a discernible diversification in asset allocation practices, indicative of a pronounced demand for financial management services among residents and a heightened propensity towards enlisting the services of financial advisors. Moreover, the East China six provinces exhibit a spectrum of geographical locations and economic structures, manifesting substantial disparities in economic development across different locales. This heterogeneity affords a more nuanced depiction of the diverse population groups and regional dynamics present within the area. Consequently, opting to focus on the East China six provinces for research purposes is deemed a judicious choice. It is imperative to acknowledge that while the East China six provinces may not comprehensively represent the entirety of China's population, their status as economically developed regions suggests that the financial advisory behaviors observed within this context may, to a certain extent, reflect broader trends among Chinese residents. As such, the insights gleaned and policy recommendations formulated through this research endeavor hold the potential to furnish valuable perspectives applicable to other regions.

The survey employed a multi-stage random sampling methodology, as follows: Initially, from each of these selected provinces, 3-4 prefecture-level cities or counties were randomly chosen, totaling 19 selections. Subsequently, from each selected prefecture-level city or county, 3 districts or counties were randomly selected based on criteria such as local economic development and urban population size. From these chosen districts or counties, 3 neighborhood committees and 3 village committees were randomly selected, with consideration given to the population size of the community. Finally, approximately 20 households were randomly chosen from each neighborhood or village committee, resulting in a total of 6800 households surveyed. This comprehensive survey collected detailed information encompassing various aspects of society, including population demographics, income and expenditure patterns, production and business activities, credit-related behavior, and the fundamental characteristics of the communities in which the sampled households were situated. The data collected provided a wealth of micro-level information to support the analysis and findings of this study.

Prior to the analysis, the data underwent various preprocessing procedures. Initially, invalid samples, including erroneous responses, extreme values, and unanswered questions, were excluded, yielding 6618 valid samples. Following this, samples with missing values related to key variables were filtered out, leaving 6524 valid samples. Lastly, samples corresponding to household heads younger than 18 years old or older than 80 years old were omitted, resulting in a final data set of 6056 valid samples.

VariablesDependent variableThis study employs a research approach akin to that of Brenner and Meyll (2020) and Liu and Lu (2023) to gauge the demand for and engagement with financial advisors among residents.

Need for financial advisors (need)The survey questionnaire included the question, “Do you require financial advisors or investment consultants?” Based on responses of “yes” or “no,” a binary dummy variable, denoted as “need,” was created to signify the presence of demand for financial advisors. A response of “yes” was considered a demand for financial advisors, assigned a value of 1. Conversely, a response of “no” indicated no demand for financial advisors among households, assigned a value of 0.

Engagement of financial advisors (engage)For respondents expressing a demand for financial advisors, further inquiry was made: “Does your household currently employ a financial advisor or investment consultant?” Based on responses of “yes” or “no,” a binary dummy variable, denoted as “engage,” was constructed to indicate whether a financial advisor was hired. A “yes” response signified engagement with a financial advisor, thus assigned a value of 1. Conversely, a “no” response indicated no engagement with a financial advisor, assigned a value of 0. Notably, observations of the “engage” variable are only applicable when “need” equals 1.

Therefore, “need” delineates the subjective demand for a financial advisor, while “engage” encapsulates the objective behavior of engaging a financial advisor subsequent to expressing the subjective need.

Independent variableBuilding upon the conceptual framework outlined by Ragnedda (2017) and Gómez (2018), this study evaluates the digital divide across three distinct levels:

Access GapThe first level, known as the Access Gap, is gauged through internet accessibility. Householders are queried on two aspects: “Do you have mobile internet access?” and “Do you have computer internet access?” If a householder responds negatively to both questions, they are considered to have encountered an access gap. If a householder responds positively to at least one question, they are considered not to have suffered an access gap. A binary variable named “access gap” is crafted to identify whether the householder is affected by an access gap. A value of 1 denotes the presence of an access gap, while 0 signifies its absence.

Usage GapThe second level of the digital divide, termed the Usage Gap, is quantified by the frequency of internet usage. For householders without suffering access gap (i.e., with internet access), the questionnaire explores their internet use frequency for learning, work, social activities, entertainment, and commercial activities. Response options include “almost daily,” “3-4 times a week,” “1-2 times a week,” etc., each assigned a numerical value. Variables are generated for each category (e.g., Study Usage Gap, Work Usage Gap, Social Usage Gap, Entertainment Usage Gap, and Commerce Usage Gap). Subsequently, factor analysis is employed on these five indicators to establish the variable “Usage Gap.” A higher value signifies a decreased overall frequency of internet usage by the householder, thereby indicating a more pronounced severity of the experienced usage gap.

Utility GapThe third level, referred to as the Utility Gap, is determined by the perceived importance of the Internet. For householders without suffering access gap, the questionnaire investigates the importance of the Internet for various activities, like learning, work, social activities, entertainment, and business activities. Response options are assigned values from 1 to 5, with 1 indicating “very important” and 5 indicating “very unimportant.” Variables are constructed for each category (e.g., Study Utility Gap, Work Utility Gap, Social Utility Gap, Entertainment Utility Gap, and Commerce Utility Gap). Building on this foundation, factor analysis is applied to the five mentioned indicators, yielding the variable termed “Utility Gap.” A higher value signifies a reduced overall perceived importance of the internet for the householder, reflecting a heightened severity of the experienced Utility Gap.

Control variableTaking cues from existing literature (Bhattacharya et al., 2023; Burke & Hung, 2021; Delis et al., 2023; Fong & Lee, 2023; Liu, 2023; Piehlmaier, 2022), this study incorporates the following control variables:

Individual Characteristics of the Householder:

Gender (gender): Binary variable (male=1, female=0).

Age (age): Continuous variable representing the age of the householder denoting the years of education.

Education Level (edu): Continuous variable denoting the years of education.

Marital Status (marriage): Binary variable (married=1, otherwise=0).

Financial Literacy (knowledge): calculated based on classic “Big 3″ questions.

Risk Preference (risk): Binary variable (preference for risk=1, otherwise=0).

Family Characteristics:

Size of Household Population (pop): Continuous variable representing the total number of individuals in the household.

Proportion of Labor Force (ratio): Continuous variable indicating the percentage of the household involved in the labor force.

Ownership of House (house): Binary variable (yes=1, no=0).

Purchase of Commercial Insurance (insurance): Binary variable (whether to purchase commercial insurance: yes=1, no=0).

Total Household Income (income): Continuous variable representing the total income of the household.

Regional Differences: Using Zhejiang Province as a reference group, binary dummy variables for five other provinces are introduced to control for regional disparities.1

Identification variableAs previously mentioned, to ensure identifiability, it becomes crucial to introduce identification variables at this point. Specifically, the mean digital divide experienced by households within the community serves as the identification variable. To elaborate further, when examining the consequences of the access gap, the identification variable corresponds to the proportion of the community grappling with the access gap. Similarly, when exploring the usage gap, the identification variable is represented by the mean usage gap experienced within the community. Finally, in the examination of the utility gap, the identification variable is represented by the mean utility gap experienced across the community.

Mechanism variableSocial network (network)Drawing from existing literature (Cull et al., 2022; Yang et al., 2021), this study employs household gift expenditures as a proxy to measure social networks. Respondents were asked in the survey questionnaire, “In the past 12 months, how much money did your family spend on gifts for relatives and friends? (in RMB).” Consequently, a social network variable, indicated as “network,” was constructed. A higher value indicates a more developed social network within the household.

Information attention (attention)In alignment with insights from the existing literature, this paper employs residents’ level of attention to economic or financial information as a metric for information attention (Nekrasov et al., 2023; Sicherman et al., 2016). The survey questionnaire inquires, “How much attention do you usually pay to economic and financial information?” The response options are: “Very much attention,” “Quite some attention,” “Average,” “Very little attention,” and “Never pay attention,” which are assigned values of 5, 4, 3, 2, and 1, respectively. Using these responses, a variable termed “attention” is created to indicate the extent of attention to economic and financial information by the householder. A higher value signifies a greater degree of attention by the householder to economic and financial information.

To facilitate heterogeneity analysis, this study introduces additional variables:

- 1.

Rural Residence (rural): This binary variable takes a value of 1 if the household resides in a rural area and 0 otherwise.

- 2.

Debt Status (debt): This binary variable takes a value of 1 if the household has any form of debt and 0 otherwise.

- 3.

Financial Education (train): The survey questionnaire evaluates the householder's engagement in financial knowledge learning by asking, “How much time do you spend on financial knowledge learning each week?” Responses range from “No time spent” to “More than 5 h.” A binary dummy variable, train, is constructed based on this question, taking a value of 1 if the time spent is more than 1 h, indicating receipt of financial education, and 0 otherwise.

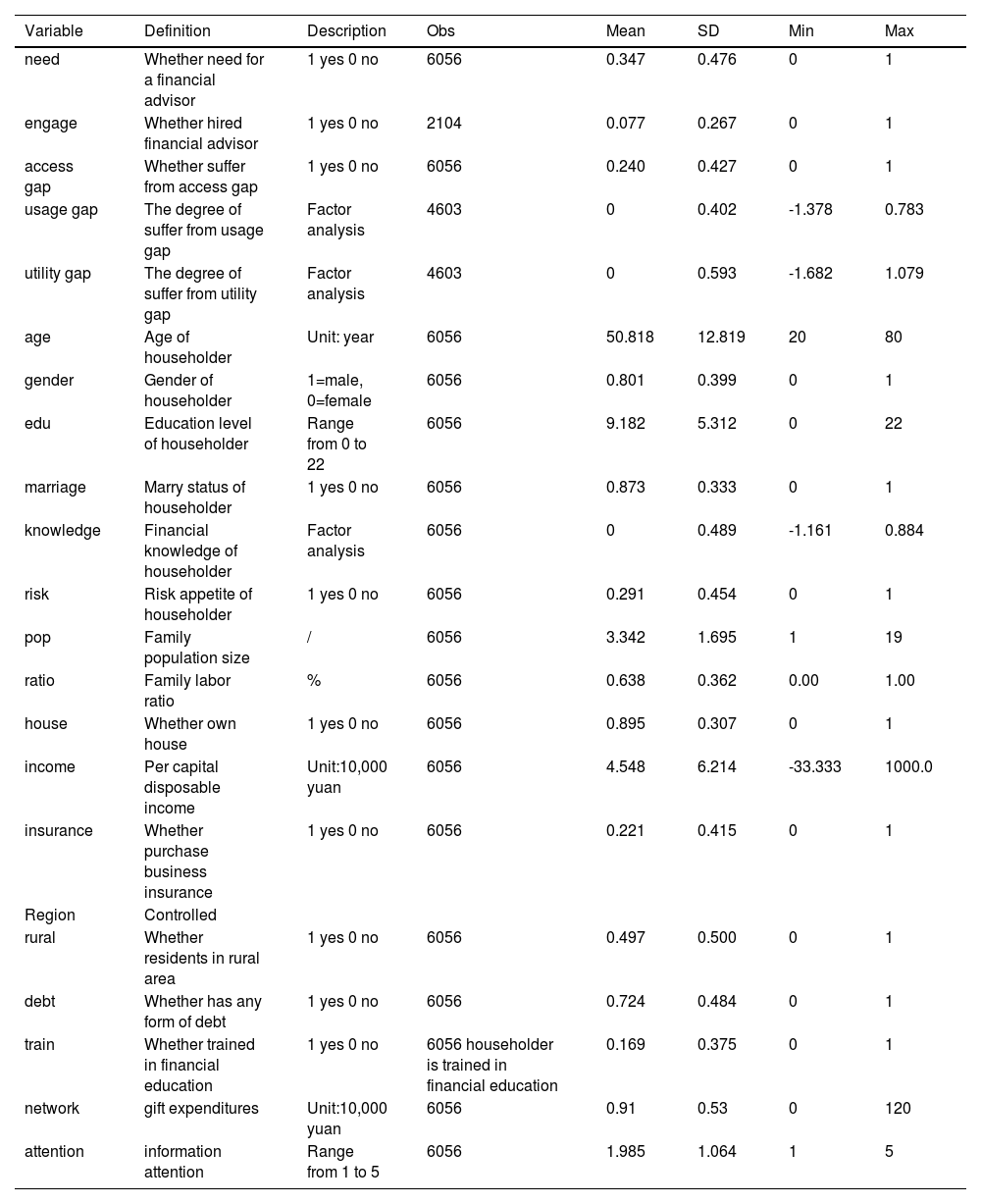

Table 1 provides a descriptive result of the variables.

Descriptive results.

In examining the factors influencing residents’ decisions to hire financial advisors, it is crucial to consider the sample selectivity issue related to the demand for financial advisors, as revealed in the earlier analysis. To tackle this consideration, this study employs the Probit model with sample selectivity, referred to as the PSS model (Chaudhuri & Cheric, 2012; Liu & Lu, 2023). The specific details are as follows:

The demand for financial advisers (the first-stage selection equation):

The engagement of financial advisers (the second stage outcome equation):

The need and engage with an asterisk (*) indicate the potential outcomes; the need and engage without an asterisk (*) are the actual observed outcomes (i.e. the demand for financial advisers, and the engagement of financial advisers). Where I(

▪) represents an in dicator function, X1 represents the explanatory variables in the selection equation, and X2 represents the explanatory variables in the outcome equation. To ensure model identification, the explanatory variables must satisfy the condition X1 ≠ X2, which means that they are not exactly the same. In addition, the error term (ε1,ε2) follows a multivariate normal distribution with mean 0 and a correlation matrix with the correlation coefficient ρ. If this correlation coefficient ρ is significant, this indicates that a sample selection problem exists. However, if the correlation coefficient ρis not significant, this indicates that the sample selection problem is negligible and the probit model can be used directly.

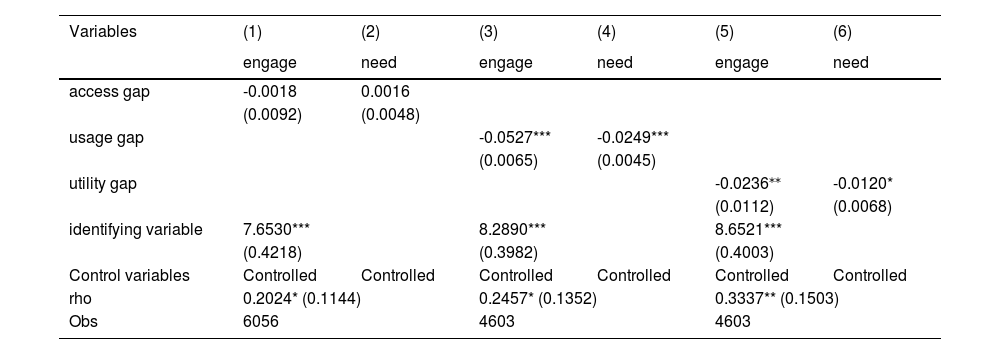

The results are outlined in Table 2. Based on the results (1) and (2), it is evident that within the first-stage selection equation, the impact of the access gap on the demand for financial advisors is insignificant. This implies that residents’ utilization of the internet does not significantly alter the probability of requiring financial advisors. In the subsequent second-stage results equation, the impact of the access gap on the engagement of financial advisors also insignificant, suggesting that subsequent to establishing a demand for financial advisors, residents’ internet usage does not markedly influence their likelihood of engaging financial advisors. Therefore, the access gap does not significantly influence whether residents have a demand for financial advisors or engagement them. This conclusion can be explained as follows: Firstly, the demand for and hiring of financial advisors typically depend on individuals’ financial status, investment goals, and urgent need for financial knowledge. Compared to the situation of internet access, individuals’ economic conditions and financial objectives may be more critical, directly affecting their inclination to seek assistance from financial advisors. Even in the absence of internet access, residents may still acquire financial knowledge through other means, such as traditional media, social circles, or physical financial institutions, to meet their demand for financial advisors. On the other hand, financial advisors are usually professionals who provide services within specific socioeconomic contexts, and their hiring is often influenced more by individuals' economic capacity and social networks. Even in the presence of an access gap, individuals with higher economic means and broader social networks are still likely to engage financial advisors, as they are better positioned to afford the fees and access relevant information.

Benchmark results.

Note: ① *, * *, and * * * respectively represent significant levels at 10 %, 5 %, and 1 %; ② The total household income and social capital are measured in tens of thousands of yuan. ③ The values within parentheses represent robust standard errors; ④For simplicity, only the estimated results of the independent variables and identifying variable are reported here.

Moving on to results (3) and (4), within the first-stage selection equation, the impact of the usage gap on the demand for financial advisors emerges as significantly negative at the 1 % level. This indicates that a decrease in the frequency of internet usage correlates with a reduced probability of necessitating financial advisors. Subsequently, in the second-stage results equation, the influence of the usage gap on the engagement of financial advisors is significantly negative at the 1 % level. This underscores that subsequent to establishing a demand for financial advisors, a lower frequency of internet usage corresponds to a diminished likelihood of engaging financial advisors. Lastly, results (5) and (6) elucidate that within the first-stage selection equation, the impact of the utility gap on the demand for financial advisors is significantly negative at the 5 % level. This implies that a diminished perception of the Internet's importance correlates with a decreased likelihood of requiring financial advisors. In the ensuing second-stage results equation, the effect of the utility gap on the engagement of financial advisors appears significantly negative at the 10 % level. This suggests that post-establishment of a demand for financial advisors, a lower perceived importance of the internet corresponds to a reduced likelihood of engaging financial advisors. In summary, the article's findings partially support hypotheses H1a and H1b.

Detailed discussions of the control variables are omitted here, given the secondary focus of this analysis. As depicted in Table 1, the coefficients of the two-stage equations exhibit positive significance at the 10 %, 10 %, and 5 % levels, respectively. This underscores the imperative nature of addressing sample selectivity issues, necessitating the implementation of the PSS model. Additionally, the identification variable manifests positive and significant impacts at the 1 % level, affirming the feasibility and identifiability of the PSS model. Consequently, the incorporation of the PSS model in this study is considered both necessary and viable.

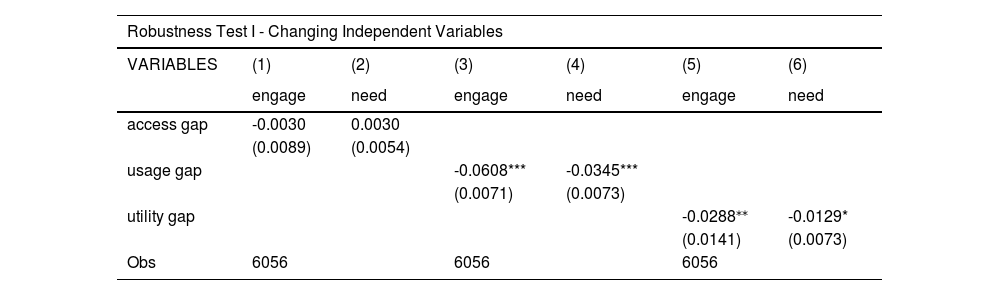

Robust testRobustness Test I - Changing Independent Variables. In this test, the independent variable measuring the access gap is modified to reflect whether the user utilizes the internet for access. Additionally, the factor analysis method for assessing the use of channels and utility channel is substituted with aggregation via mean calculation. The results are delineated in Table 3.

Robustness test results.

For simplicity, only the estimated results of the independent variables are reported here, the other notes are the same as Table 2.

Robustness Test II - Changing Control Variables. This test involves replacing several control variables: The family labor ratio is substituted with the family support ratio (computed as 1 minus the family labor ratio). The definition of the householder's education level is revised to assign a value of 1 to heads of households with a high school education or higher, and 0 to those with lower educational attainment. In addition, add the per capital GDP of the province. The results are presented in Table 3.

Robustness Test III - Changing Extreme Value Samples. In this test, extreme values within the datasets, specifically the 1 % sample comprising the lowest and highest income, undergo Winsorization. The results are exhibited in Table 3.

Robustness Testing IV - Endogeneity Discussion. When examining the impact of the digital divide on residents’ demand for and engagement of financial advisors, endogeneity concerns may arise, potentially leading to estimation biases. Among these concerns, bidirectional causality stands out as particularly noteworthy. While the digital divide may influence residents’ demand for and engagement of financial advisors, residents, in determining whether to manifest such demand or engage advisors, may exhibit a proclivity towards active internet usage and a heightened awareness of its significance, thereby affecting the extent of the digital divide. To mitigate this issue, the current study incorporates lagged variables of the independent variable for analysis.2 The results are detailed in Table 3.

In summary, the results of these robustness tests consistently demonstrate the stability and reliability of the estimation results presented in the paper. Whether changing extreme values, modifying the definition of independent or control variables, or considering the endogeneity problem, the estimation results remain robust.

Heterogeneity analysisHeterogeneity analysis I: urban-rural disparityIn this analysis, residents are stratified into two groups based on their household location: rural and urban. As depicted in Heterogeneity Analysisthe heterogeneity analysis I in Table 4, it is evident that, in terms of both significance levels and coefficient values, the inhibitory effects of the usage gap and utility gap on the demand for and engagement with financial advisors among urban residents are more pronounced compared to rural residents. The reasons for this discrepancy are primarily twofold: Firstly, rural areas often contend with relatively underdeveloped digital infrastructure, characterized by limited network coverage and slower internet access speeds. This condition renders rural residents more vulnerable to the influence of the usage gap. Facing challenges in accessing financial information and services online, rural residents are less likely to comprehend and acknowledge the necessity of financial advisors in comparison to their urban counterparts.

Heterogeneity analysis.

Notes are the same as Table 3.

Consequently, this diminishes their demand for and willingness to hire financial advisors. Secondly, the economic status in rural areas is comparatively lower, and residents generally exhibit weaker financial literacy and awareness. Conversely, urban residents lean towards active participation in online financial activities and attribute greater significance to the Internet in financial matters. The perception of the internet's importance is less pronounced among rural residents, rendering them more susceptible to the influence of the utility gap. Consequently, this weakens their demand for and willingness to hire financial advisors. Lastly, information dissemination channels in rural areas are relatively scarce, limiting information exchange and communication among residents. In contrast to urban residents who rely more on traditional word-of-mouth and social networks for information, the restricted access to information among rural residents exacerbates the reduction in their perceived importance of the internet. This deepens the inhibiting effect of the utility gap.

Heterogeneity analysis II: debt status disparityIn this analysis, residents are categorized into two groups based on their debt status: households with debt and households without debt. According to heterogeneity analysis II in Table 4, it is evident that, both in terms of significance levels and coefficient values, the inhibitory effects of the usage gap and utility gap on the demand for and engagement of financial advisors among households with debt are stronger compared to households without debt. The reasons for this disparity are primarily as follows: Firstly, households with debt typically face more urgent financial pressures and difficulties. They may need to allocate more time and energy to address debt issues, potentially allocating fewer resources to financial advisory services. This financial pressure may lead them to be more cautious in their financial expenditure, thereby reducing their demand for and willingness to hire financial advisors. Secondly, households with debt may have a lower level of financial service awareness and understanding. As they focus more on addressing immediate financial issues, they may devote less attention to learning about financial knowledge and skills. Consequently, compared to households without debt, they perceive the importance of the internet and financial services less, making them more susceptible to the influence of the utility gap, thereby weakening their demand for and willingness to hire financial advisors. Lastly, households with debt may adopt a more cautious and conservative approach to financial decision-making. As they are already in a state of indebtedness, they may approach new financial investments more cautiously and prefer safer and more conservative investment options. This conservative financial attitude may lead to a decreased demand for and willingness to hire financial advisors, further exacerbating the inhibitory effects of the usage gap and utility gap on their demand for financial advisors.

Heterogeneity analysis III: financial education disparityIn this analysis, residents are divided based on whether they have received financial education. According to heterogeneity analysis III in Table 4, it is evident that, both in terms of significance levels and coefficient values, the inhibitory effects of the usage gap and utility gap on the demand for and engagement of financial advisors among residents without financial education are stronger compared to those with financial education. The reasons for this discrepancy are primarily as follows: Firstly, residents who have received financial education often possess higher financial literacy and management abilities. They have a deeper understanding of financial products and services and are better equipped to handle financial planning and investment decisions. Therefore, compared to residents without financial education, they are more likely to fully utilize the internet for financial activities, thereby reducing the negative impact of the usage gap and maintaining a relatively stable demand for and willingness to hire financial advisors. Secondly, residents who have received financial education typically attach greater importance to the internet and digital financial services. They have higher levels of internet awareness and usage frequency and are more aware of the convenience and efficiency enhancement that the internet brings to financial activities. Therefore, compared to residents without financial education, they are more likely to maintain a high utility of the internet, reducing the negative impact of the utility gap and thereby maintaining a relatively stable demand for and willingness to hire financial advisors. Lastly, residents who have received financial education often possess better abilities to access and evaluate financial information. They can more accurately discern and evaluate the authenticity and credibility of financial information online, thus having better capabilities to utilize the internet for financial activities. Therefore, compared to residents without financial education, they are less restricted by information acquisition channels, reducing the negative impact of the utility gap and consequently maintaining a relatively stable demand for and willingness to hire financial advisors.

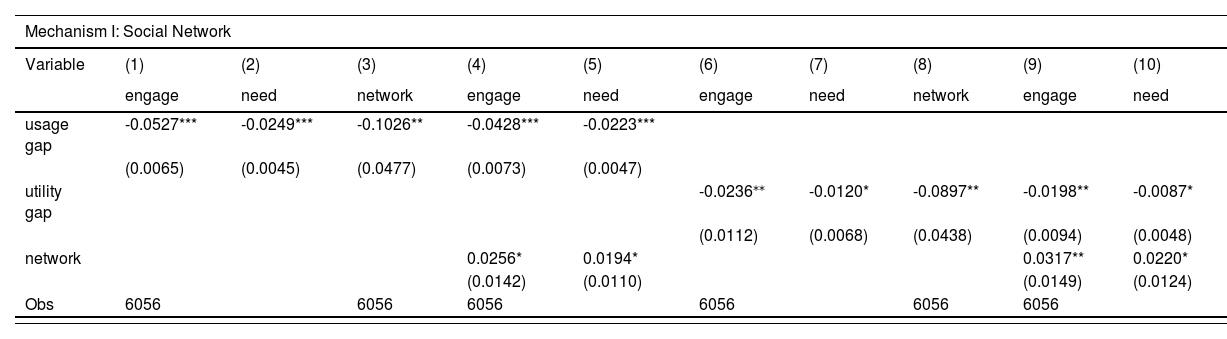

MechanismsFollowing the methodology in existing literature (Lu et al., 2023), this study investigates whether social networks and information attention act as mechanisms for the influence of the digital divide on residents’ demand for and engagement with financial advisors. Given the non-significant effect of the access gap, the analysis focuses solely on the usage gap and utility gap in this context.

Social network mechanismAccording to the findings from Mechanism Test I presented in Table 5, it is apparent that the impact of the usage gap on both the demand for and engagement with financial advisors is negatively significant at the 1 % level, with coefficients of -0.0527 and -0.0249, respectively. Moreover, result (3) underscores the substantial influence of the usage gap on social networks at the 5 % level. Subsequent analysis from results (4) to (5) reveals that upon introducing social network variables, the impact of social networks becomes significantly positive at the 10 % level, while the effect of the usage gap on both the demand for and engagement with financial advisors remains significantly negative at the 1 % level. However, it is notable that the absolute value of the coefficient for the usage gap has decreased compared to the initial findings (-0.0428 vs -0.0527; -0.0223 vs -0.0249). Similarly, from results (6) to (10), it becomes apparent that the utility gap diminishes residents’ demand for financial advisors and their likelihood to engage financial advisors by weakening social networks. Consequently, hypothesis H2 is partially affirmed, suggesting that both the usage gap and the utility gap contribute to a reduction in residents’ demand for and engagement with financial advisors by eroding social networks.

Mechanism.

Notes are the Same as Table 3.

In the findings of results (1) to (5) outlined in Table 5, it is evident that the usage gap reduces the probability of urban residents expressing a demand for financial advisors and engaging financial advisors by lowering their level of information attention. Similarly, from results (6) to (10), it becomes clear that the utility gap decreases the likelihood of urban residents expressing a demand for financial advisors and engaging financial advisors by dampening their level of information attention. Consequently, hypothesis H3 is partially validated, suggesting that both the usage gap and the utility gap contribute to a decline in residents' demand for and engagement with financial advisors by reducing their level of information attention.

Discussion and implicationDiscussionIn the realm of widely acknowledged science and technology, specifically Information and Communication Technology (ICT), their profound impact on people's lifestyles and well-being is undeniable. However, the internet, a pivotal element in these advancements, does not merely usher in digital opportunities and advantages; it also introduces new challenges in social governance, commonly known as the digital divide. The swift evolution of digital technology has broadened the scope of the digital divide, now encompassing nuanced dimensions beyond mere access, including the usage gap and utility gap. As the internet becomes increasingly ingrained in daily life, the impact of the digital divide on residents’ economic and financial decision-making gains prominence.

In contemporary digital societies, the digital divide is acknowledged as a potential contributor to financial inequality among residents (Benković & Milosavljević, 2023; Vassilakopoulou & Hustad, 2023). On one side of the coin, the digital divide may result in inequities in financial information access. Residents with robust digital literacy and skills may find it easier to access high-quality financial information, empowering them to grasp market dynamics and financial product nuances, thereby facilitating more knowledgeable financial decisions. Conversely, individuals lacking digital skills or access to digital financial channels may grapple with obtaining sufficient information, placing them at a disadvantage in financial markets.

On the flip side, the digital divide can also give rise to disparities in financial services. As financial services undergo increased digitization, many institutions shift their offerings to online platforms. However, not every resident can readily access or navigate these digital services, particularly those lacking digital skills or internet connectivity. Consequently, these individuals may miss out on the convenience and advantages associated with digital financial services, intensifying disparities in financial service accessibility.

This study draws on data from a 2022 survey of Chinese residents to thoroughly investigate the impact of the digital divide on residents’ demand for and engagement with financial advisors. The results indicate that while the access gap may not significantly influence residents’ demand for or engagement with financial advisors, both the usage gap—derived from observable internet usage patterns—and the utility gap—stemming from subjective assessments of internet utility—exhibit inhibitory effects on residents’ demand for and engagement with financial advisors. Heterogeneity analysis reveals that the inhibitory impacts of the usage gap and the utility gap are more prominent in rural households, households burdened with debt, and households with individuals lacking financial education. Furthermore, mechanism analysis demonstrates that both the usage gap and the utility gap diminish residents’ demand for and engagement with financial advisors by undermining social networks and reducing levels of information attention.

Undoubtedly, the Internet has evolved beyond being a mere information source, now encompassing diverse activities and services integral to residents’ daily lives. China, in the span of several decades, has transitioned from catchhing up in the 1980s and 1990s to emerging as a global leader in the 21st century. Despite significant advancements, the persistent challenge of the digital divide remains a pressing issue. The COVID-19 pandemic further highlighted the indispensable role of digital devices and literacy in various aspects of life in China, such as travel, work, and daily routines. Unfortunately, individuals lacking access to adequate digital resources and skills faced exclusion and disadvantages during the pandemic (Lythreatis et al., 2022; Zhao et al., 2022). Excessive digitization, in certain contexts, can indeed lead to new forms of the digital divide or worsen the challenges faced by digitally disadvantaged groups. As we navigate the digital age, striking a balance between embracing technological advancements and ensuring equitable distribution of benefits across society is crucial. Addressing and mitigating the digital divide becomes imperative for promoting more inclusive and sustainable development.

Chinese residents are increasingly reliant on the Internet; however, there are significant variations in Internet usage patterns among individuals. According to the recently published Digital China Development Report for 2021, approximately 32 % of residents either rarely or never utilize the Internet for self-presentation, online work, social interactions, or online learning. Despite a general decrease in the prevalence of the usage gap among Chinese Internet users over time, substantial disparities persist, hindering many individuals from fully exploiting the Internet's potential. Proficiency in harnessing new technologies positions certain individuals to enjoy increased opportunities, resources, and influence amid the ongoing deluge of technological advancements (Liao et al., 2022; Lu et al., 2023; Scheerder et al., 2017).

However, the emergence of the digital divide presents entirely new challenges for residents’ participation in financial advisory services (Benković et al., 2023; Nadkarni & Prügl, 2021; Yigitbasioglu et al., 2023). Firstly, the digital divide may lead to disparities among residents in accessing channels and avenues for financial information. Residents with digital skills and access to digital platforms may find it easier to access a wide range of financial information, while individuals lacking digital literacy or internet access may face limitations in information acquisition. This unequal access to information may result in certain residents lacking comprehensive and accurate information support in their financial decision-making process. Secondly, the digital divide may make it difficult for residents to understand and utilize complex financial concepts and data analysis. The digital transformation has brought about vast amounts of financial data and sophisticated financial tools; however, for some residents, a lack of necessary digital literacy and skills may hinder their ability to effectively comprehend and utilize this information. This may impede individual engagement in financial advisory services, leaving them confused and helpless when faced with complex investment decisions. Additionally, the digital divide can affect individuals’ ability to use technological tools for financial management and advisory. With the continuous development of financial technology, many financial advisory services have become digitized, such as online wealth management platforms and robot-advisors. However, residents lacking digital skills may struggle to proficiently use these tools, thus missing out on the convenience and benefits of digitized financial advisory services.

In summary, prioritizing the digital divide issue is of paramount importance as it facilitates broader access for individuals to fully partake in the opportunities and advantages ushered in by digital progress during the era of digital transformation. Therefore, enhancing residents’ financial well-being, such as by increasing the demand for and hiring of financial advisors among residents, can better facilitate financial planning and implementation, underscoring the significance of this matter warranting meticulous attention and consideration.

ImplicationAcademic inspirationFirstly, the research on residents’ financial advisory behavior mandates attention not only towards subjective demand but also towards actual engagement practices. When exploring the factors influencing the engagement of financial advisors, addressing the issue of sample selectivity concerning the demand for financial advisors becomes imperative. Moreover, despite recent endeavors to identify factors shaping residents’ financial advisory behavior, limited literature exists on the impact of the digital divide. This paper categorizes the digital divide into three distinct levels and employs the PSS model to examine the effects of varying digital divide levels on residents’ demand for and engagement of financial advisors. This approach aids in mitigating estimation bias stemming from sample selectivity while offering a fresh perspective on elucidating the limited engagement of residents especially in China in financial advisory behavior.

Secondly, with the ongoing advancement of digital technology, the content and information encompassed within the scope of the digital divide have evolved into a domain characterized by heightened complexity and diversity. In light of this evolution, enhancing the information within the existing analytical framework dedicated to the scrutiny of digital divide issues is deemed imperative. Consequently, conducting more comprehensive and nuanced research and fostering extensive discourse on this evolving landscape holds significant merit.

Lastly, it is essential to comprehensively investigate the effect of the digital divide on residents’ financial counseling behavior. This inquiry should encompass an examination of potential variations across diverse scenarios and population groups. Additionally, there is a need to scrutinize the potential mechanisms through which this impact materializes and ascertain whether disparities exist in these findings across distinct levels of the digital divide. To accomplish this, a broader body of micro-empirical research is warranted to substantiate these assertions and refine our understanding of these multifaceted dynamics.

Policy inspirationFirstly, it is imperative for the government to formulate and promote policies aimed at digital financial inclusion. These policies should focus on enhancing digital literacy and proficiency in using digital financial services. By promoting digital financial platforms and providing comprehensive training and education in digital finance, residents can acquire the necessary skills to effectively utilize digital tools for financial decision-making. This, in turn, can help alleviate barriers to the demand for financial advisors.

Secondly, efforts should be made to disseminate financial knowledge and foster financial education initiatives to enhance residents’ awareness and comprehension of financial matters. Collaborative initiatives between the government and financial institutions can facilitate the organization of financial lectures, financial planning workshops, and similar activities. These endeavors aim to instill correct financial principles, bolster residents’ autonomous financial management capabilities, and consequently reduce their reliance on financial advisors.

Thirdly, financial institutions should strive to offer accessible financial products tailored to individuals less familiar with or less trusting of digital financial services. Introducing simplified and low-risk financial products can effectively lower barriers and mitigate perceived risks associated with financial management. This approach can attract a broader segment of residents to engage in financial activities independently, thereby diminishing the demand for financial advisors.

Lastly, governmental support for the financial advisory industry is essential to foster its digital transformation and innovation. Encouraging financial advisors to adopt online consulting and digital financial planning services can enhance service convenience and flexibility, aligning with the evolving needs of residents in the digital era. Such initiatives can play a pivotal role in meeting residents’ financial advisory needs effectively.

Conclusions, limitations and research prospectsThis study first provides operational definitions for the three levels of the digital divide. Introducing the analytical framework of “access gap - use gap - utility gap” helps to systematically understand the current situation of the digital divide in China. Secondly, the study uncovers that while the access gap demonstrates negligible influence on residents’ inclination towards seeking and engaging financial advisors, both the use gap and utility gap exhibit inhibitory effects, albeit with variances across diverse demographic segments. The third finding is that social networks and information attention serve as mechanisms through which the use gap and utility gap influence residents’ demand for and engagement of financial advisors.

Certainly, this study is not devoid of limitations that warrant acknowledgement. Firstly, the research scope is confined to residents within the eastern region of China. Although this restriction enhances the study's precision and relevance within a specific context, it concurrently curtails its generalizability to broader populations. Expanding the scope to encompass global or national comparisons could potentially facilitate a more comprehensive examination; however, such an endeavor would introduce heightened uncertainty into the analysis. Secondly, the measurement of the digital divide in this paper requires refinement. While the paper analyzes the second-level digital divide based on usage frequency, it overlooks crucial aspects such as the digital capability divide, which is a significant manifestation of the second-level digital divide. Similarly, the digital outcome divide, which is an important facet of the third-level digital divide, is not adequately addressed. Although the paper measures the utility gap (i.e., the perceived importance of the Internet), it fails to directly assess the consequences of internet usage. Additionally, relying solely on perceived importance may not accurately discern whether the consequences of internet usage are positive or negative. Finally, this study utilizes cross-sectional data, which limits its ability to capture the dynamic impact of the digital divide on residents’ demand for and engagement of financial advisors, as well as their causal relationships. Subsequent research endeavors will seek to address these limitations by conducting longitudinal surveys and forming panel data to provide a more understanding of these relationships over time.

FundingThis work is supported by the Jiangsu Office of Philosophy and Social Science (Grant No. 2021SJZDA122); National Social Science Fund of China (No's. 21&ZD115, 22&ZD123, 23AJY014); National Natural Science Foundation of China (No. 72073060).

Data and code availabilityThe data and code used to support the findings of this study are available from the corresponding author upon request.

CRediT authorship contribution statementPeng Li: Writing – review & editing, Writing – original draft, Formal analysis, Data curation, Conceptualization. Qinghai Li: Writing – review & editing, Writing – original draft, Formal analysis, Data curation, Conceptualization. Xing Li: Writing – review & editing, Writing – original draft, Validation, Supervision, Software, Conceptualization.

We many thank the National Bureau of Statistics of China for their provide database, and the anonymous reviewers of the article.

It is noteworthy that the highest value of absolute correlation coefficient among the explanatory variables (comprising independent and control variables) is 0.62, which falls below the threshold of 0.65. Additionally, the value in the VIF test for the explanatory variables is merely 7.5, indicating the absence of multicollinearity issues among these variables.

Notably, residents’ experience of the digital divide tends to manifest as a continuous phenomenon, with correlation coefficient analysis indicating strong correlations between the current values of access gaps, usage gaps, and utility gaps, and their respective values in previous periods (The coefficients associated with the three levels of the digital divide are 0.7916, 0.7035, and 0.7328, respectively, all exhibiting statistical significance at the 1% level). However, it is crucial to note that residents’ prior experience of the digital divide does not directly influence their demand for or engagement of financial advisors in the current period.