Edited by: Abbas Mardari

More infoImproving firms’ innovation capability is crucial for promoting growth. In 2006 and 2009, China deregulated the banking industry and allowed city banks to set up branches across regions, which changed the banking structure and competition. Using data from financial licence information and 1,012,321 manufacturing firms in China during the 2004–2010 period, this study investigates the effects of banking deregulation on research and development (R&D) investment and provides a reference for firm innovation. The results show that city bank entry increases R&D investment by 0.084% and R&D investment increases by 0.037 percentage points with a 1% increase in cross-regional branches of city banks. The robustness and endogeneity tests confirm these findings. Mechanism tests reveal that city banks’ deregulation encourages firms to participate in R&D activities and improve R&D investment by reducing financing constraints. The impacts of city banks’ cross-regional operations on R&D investment are heterogeneous due to the variety in the geographical location, ownership, size, industry and age of firms. The promotion of banking deregulation on R&D investment comes from firms in the eastern region. The positive effect of banking deregulation is stronger for state-owned enterprises than private and foreign enterprises, stronger for large firms than small and medium firms, stronger for high-tech firms than ordinary firms and stronger for old firms than new firms. These findings provide evidence and implications for optimising financial structure to promote firm innovation and economic growth.

The mode of economic growth driven by factor input is unsustainable in developing countries, and it is essential to establish an innovation-driven growth pattern with strong research and development (R&D) capabilities (Nielsen, 2020). Although innovation is an endogenous power source for economic growth, R&D intensity is still at a low level in developing countries (Chen et al., 2021). The National Bureau of Statistics of China announced that R&D expenditure intensity was 2.55% in 2022 and innovation quality needed to be improved. Enhancing the innovation ability of firms is crucial for developing countries to skip the middle-income trap (Wei et al., 2017).

Finance is a leading factor, and a perfect financial market helps to collect innovative resources for firms and promote innovation. The threshold of direct financing in developing countries is high; thus, small firms have limited opportunities to obtain funds through stock and bond markets to support R&D activities than large firms (Liu & Li, 2020). Therefore, indirect financing is crucial to the smooth progress of R&D activities in a financial market dominated by banks. In the 1990s, the deregulation of interstate banks in the United States enhanced financial inclusiveness, financial security and firm innovation (Célerier & Matray, 2019). China's financial system has made remarkable achievements and met the needs of the economy. In 2006, the Chinese government relaxed the regulation of small banks’ cross-regional operation, and city commercial banks (hereinafter referred to as city banks) can set up branches across prefecture-level cities or even provinces. Competition between city banks and other financial institutions reduces firm financing constraints and volatility, especially for firms that rely on external financing (Jiang et al., 2020). However, the mismatch between the financial structure of capital supply and microstructure of capital demand leads to the misallocation of financial resources and hinders innovation (Lin et al., 2015). There are few studies on the effect of banking deregulation on R&D activities and its mechanisms. Newly industrialised countries are in the stage of transforming the old and new driving forces of growth, and the lack of evidence on the effect of bank branching deregulation on R&D activities is regrettable to promote economic growth (Matthess & Kunkel, 2020).

This study matches firm data with financial licence information according to firms’ addresses and exploits a quasi-natural experiment with the difference in the establishment time of city bank branches in different regions to investigate the effects of banking deregulation on R&D activities. (1) What impact does city banks’ cross-regional operation have on R&D investment? (2) What is the impact mechanism of banking deregulation on R&D investment? (3) Does firm heterogeneity affect the effect of banking deregulation on R&D investment? Answers to these questions can evaluate the effect of banking deregulation and provide a useful reference for promoting firm innovation, which is important for improving the efficiency of capital allocation and the transformation of growth mode.

The existing research has not obtained a system theory with explanatory power on the relationship between banking deregulation and R&D activities. This study contributes to the literature in the following respects. First, this study is related to the literature that investigates the effect of city banks setting up branches across regions on R&D investment and provides suggestions for formulating policies on banking deregulation and firm innovation. The existing literature focuses on the effect of bank competition on firm financing and wages (Beck et al., 2013; Bens et al., 2022), whereas the effect on R&D activities has not yet led to conclusions (Cornaggia et al., 2015). Second, this study contributes to the literature on the effect of banking deregulation that leads to bank competition on R&D activities and to banking deregulation measurement (Chava et al., 2013; Xin et al., 2022), whereas the previous studies focused on the effect of bank competition on firm financing (Chemmanur et al., 2020; Avramidis et al., 2022). This study uses the changes in the number of cross-regional branches of city banks around firms to proxy banking deregulation. Third, this study contributes to the research on the determinants of firm R&D investment (Hall et al., 2015; Adegboye & Iweriebor, 2018). Based on manufacturing firm data, this study investigates the effects and mechanisms of the cross-regional expansion of city banks and examines the heterogeneous effects of firm location, ownership structure, size, industry and age attributes on R&D investment, which provides evidence for firm innovation and a reference for the study of banking deregulation. Finally, this study empirically examines the effect of banking deregulation on R&D activities by using econometric models, including instrumental variables and the Heckman model (Benfratello et al., 2008; Tian et al., 2019). This study reveals that not only do firms hardly affect macro-level banking deregulation but also that banking deregulation comes from exogenous shocks, which provides ideas for future research.

Section 2 summarizes the literature review and assumptions. Section 3 describes the methodology and data. Section 4 and Section 5 present the results and discussions. Section 6 is the findings and practical implications.

Literature review and research hypothesisChina's banking reformThe Chinese financial system makes remarkable reforms that meet the demand for economic growth and financial stability (Brunnermeier et al., 2022). This study focuses on banking deregulation in China for two reasons. First, China is the largest developing country and the second-largest economy in the world. China's financial system is dominated by banks. The proportion of direct financing is still low compared with indirect financing, such as bank loans, which occupy a dominant position. Second, to enhance the ability of financial services to benefit the real economy, the Chinese government relaxes its control over the banking industry. The deregulation of small banks to set up branches across regions intensifies the competition among banks and changes the banking structure (Pu & Yang, 2022). These banking reforms increase the role of market mechanisms in capital allocation and reduce the difficulty and cost of corporate financing (Lin et al., 2009).

Before the reform and opening-up in 1978, the People's Bank of China was the only bank in China that had the functions of commercial and policy financial business. In 1979, the first city credit cooperative was established. However, its cooperative nature was unclear, and the management system was imperfect. Several city credit cooperatives had been in trouble because they relied on high-interest rates to support securities and real estate speculation. After the mid-1990s, the city credit cooperatives were transformed into city banks to improve operating efficiency and reduce non-performing loans, which were mainly to provide financial services for local firms and residents. The development of city banks promotes the local economy and overcomes the dilemma that the financial market is monopolised by large state-owned banks. After China's entry into the WTO, China lowered the conditions for foreign banks to enter, which enhanced banking competition and firm supervision. The deregulation of foreign banks entering China reduces the capital costs of domestic firms and extends loan maturity (Lin et al., 2022).

Large state-owned and joint-stock banks can set up branches nationwide, whereas small banks, such as city banks, cannot set up branches in other cities. The cross-regional operation of city banks goes through three stages. Before 2006, it was forbidden for city banks to set up branches across cities. A city can only set up one city bank, and the city bank can only set up branches in its own city. A more strictly regulated banking market is less competitive (Claessens & Laeven, 2004). Therefore, this limits the geographical scope of financial services for city banks, which is not conducive to enhancing bank competition and hindering scale economies. Moreover, due to geographical restrictions, it is difficult for city banks to improve their brand influence and popularity across regions. The regulations of city banks increase operational risk. When the operations of city banks are limited to a city, their operating performance is easily affected by local economic fluctuations. Government intervention in the banking industry reduces banks’ size and market share, because the regulation forces banks to lower deposit interest rates (Nielsen & Weinrich, 2023).

In 2006, the National Administration of Financial Regulation (NAFR) promulgated ‘The Measures for the Administration of Branches of City Commercial Banks in Different Places’. The law lowers the conditions for the cross-regional operation of city banks, and city banks compete for market share with large state-owned and joint-stock banks. The deregulation of city banks changes the banking market structure and enhances banking competition. Majority of the largest shareholders of city banks are local governments and state-owned enterprises. City banks gain more deposits by adding branches and expanding the scope of services, which is an important channel for governments to increase investment and stimulate economic growth (Chen et al., 2020).

In 2009, NAFR gave the approval authority for city banks to set up branches in the province to the provincial regulatory authorities. There are no longer restrictions on the number of cross-regional branches for city banks, and city banks enter a period of rapid development that enhances banking competition. Although interstate banking deregulation has no effect on economic growth, intrastate branching deregulation is beneficial to improving the local long-term economy by 0.5 percentage points in the United States (Spierdijk et al., 2021).

The cross-regional operation of city banks provides an opportunity to clarify the effect of banking deregulation on R&D activities by separating the role of city banks in stimulating R&D investment from that of large banks. The expansion of city banks intensifies financial competition, forming new ways to ease financing constraints (Gao et al., 2019). The mechanism by which banking deregulation affects loan quality lies in the fact that the diversification of operating areas reduces the customer concentration of banks after deregulation, which reduces systemic risk. Therefore, this study investigates the effects of the cross-regional operation of city banks owing to banking deregulation on firm R&D activities.

Banking deregulation and R&D investmentAn imperfect financial market and weak handling ability of soft information by financial institutions lead to financing constraints, whereas a perfect financial structure, low government intervention and financial agglomeration help firms obtain funds (Berger et al., 2017). It is an inherent requirement of firm management to reduce financing constraints. Financial institutions’ expansion alleviates financing constraints by collecting information footprints, reducing information asymmetry and financial exclusion, correcting resource mismatches, controlling innovation risk and improving capital allocation efficiency (Fungacova et al., 2017; Caggese et al., 2019). Moreover, financial development reduces finance costs and promotes R&D activities; however, financial friction hinders firm R&D activities (Hall et al., 2015; Bazot, 2018).

There are two views on the impact of banking competition on firm financing. The information hypothesis holds that weakening financial competition encourages banks to establish contact with borrowers to obtain information, reduces the adverse effects of information asymmetry and increases relational financing. Information asymmetry and agency problems cause an increase in firm costs, namely, financing constraints (Myers & Majluf, 1984; Gertler, 1992). Compared with big banks, small banks have a more flexible operating mechanism and a higher enthusiasm for obtaining the soft information from firms, thus narrowing the information asymmetry between banks and firms (King & Levine, 1993; Berger & Udell, 2002). In the asymmetric information market, a banking monopoly helps banks overcome adverse selection and moral hazard, encourages banks to obtain borrower information and expands financing supply (González, 2020). A medium level of banking deregulation improves financial efficiency, which is the best state of banking competition (Biswas & Koufopoulos, 2020).

The market power hypothesis argues that banking deregulation is beneficial to firms as it improves financing availability and alleviates financial constraints (Santiago et al., 2009; Wang et al., 2020). When the monopoly of the banking industry weakens, and banking competition intensifies, banks will provide more attractive terms to compete for high-quality customers. Branching deregulation and increasing small financial institutions promote banking competition, reduce financing costs and stimulate firm innovation (Rice & Strahan, 2010). The deregulation of the British banking industry strengthens the relationship between banks and firms and stimulates firms to increase leverage and R&D investment (Braggion & Ongena, 2019). Branching deregulation reduces bank concentration and results in low market share and loan interest, which are stronger in the competitive industry of strategic alternatives with negative externalities (Saidi & Streitz, 2021).

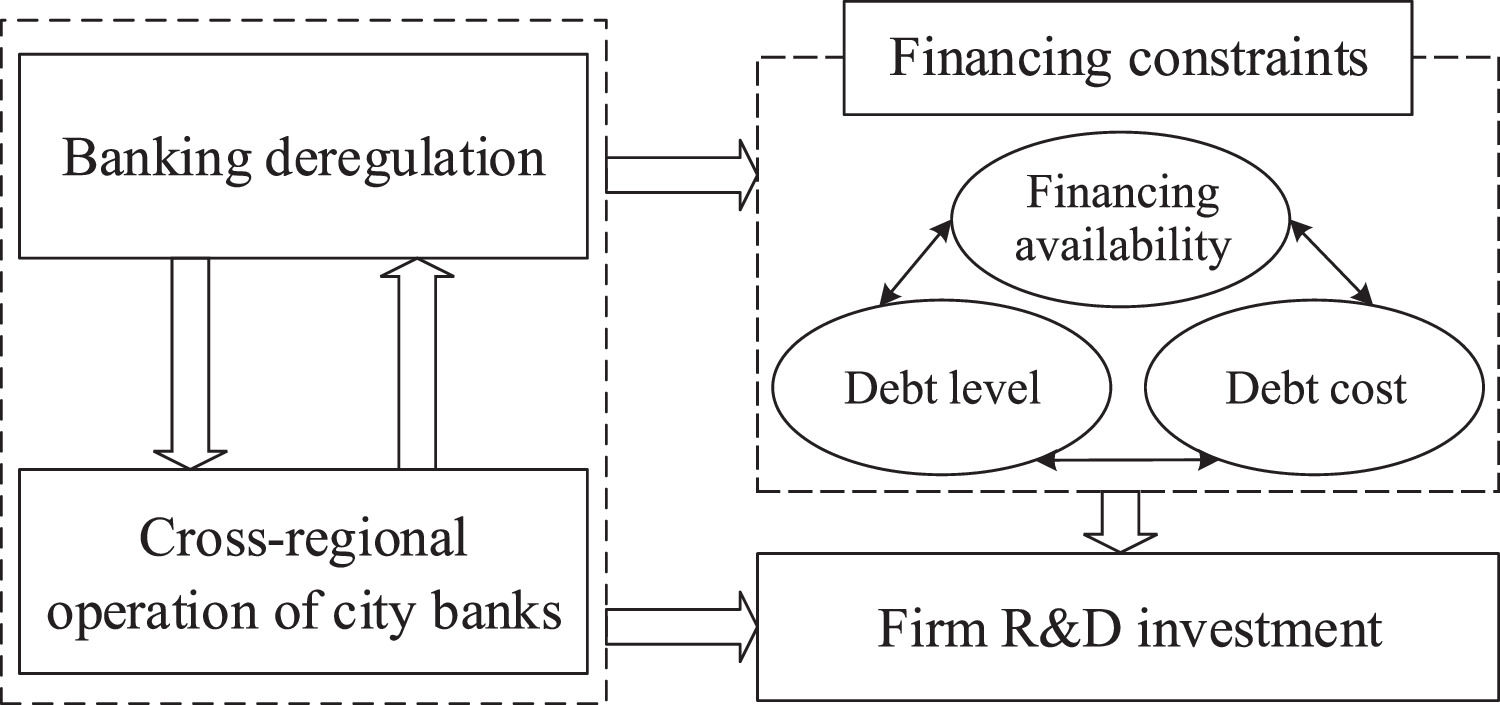

The cross-regional operation of city banks caused by banking deregulation affects firms’ financing constraints and R&D investment in two aspects. First, city banks are an important source of funds for firms and are closely connected with local governments, which are the largest shareholders of many city banks (Cheng et al., 2021). The main goal of setting up bank branches across regions is to absorb deposits and issue loans (Thorsten et al., 2010). The deregulation of banks intensifies the competition in the banking market where they are located, forming a new channel to reduce financing constraints and increase R&D investment (Rice & Strahan, 2010). Second, banking deregulation reduces ownership and relationship discrimination; thus, small firms obtain more funds from financial institutions than before. By opening branches across regions, city banks conduct due diligence on firms, alleviate information asymmetry and then reduce credit risk and non-performing loans. Geographic deregulation of banks affects their capital management tools and leads to a higher target capital ratio (Berger et al., 2023). Management compensation is a way through which banking deregulation increases firms’ risk incentives and innovation (Bens et al., 2022). If banking deregulation could improve financing availability and reduce debt costs, the cross-regional operation of city banks would promote R&D investment by reducing firm financing constraints, as shown in Fig. 1. Based on this, the following hypotheses are formulated.

Hypothesis 1: Banking deregulation increases firm R&D investment.

Hypothesis 2: Banking deregulation increases firm R&D investment by reducing financing constraints.

The lending relationship between banks and firms may be sensitive to firm characteristics, market structure, business environment and public policy (Berger & Udell, 2002; Hsieh et al., 2019). Information asymmetry, low financial transparency and a lack of collateral result in financing constraints (Bollaert et al., 2021). By setting up branches across regions, city banks gain a wider development space, increase the sources of deposits and loans and reduce debt costs and loan risks (Deng & Elyasiani, 2008). Hence, the effects of increased banking deregulation on R&D investment may be heterogeneous due to the diversification of firm characteristics.

The ownership competition view holds that it is more difficult for private firms to obtain loans than for state-owned enterprises (Cull & Xu, 2003). There is bank discrimination in the financing market; state-owned enterprises can obtain stable loans, whereas private firms find it difficult to obtain an equal market position. Private firms have obvious characteristics of financial repression, fewer financing channels and a lack of relationships with banks. As a result of interventions by state-owned banks and governments, lending by banks prefers state-owned enterprises to private firms (Cheng et al., 2021). Bank concentration is positively related to long-term debt and maturity structure for state-owned enterprises, whereas lower government intervention is a benefit for private firms to obtain long-term loans (Liu et al., 2018). Therefore, it is easier for state-owned enterprises to obtain financing from the financial market than private firms. Since banking deregulation allows small banks to set up branches across regions, similar to state-owned banks, the impact of banking deregulation on firms is more prominent in areas with a higher proportion of state-owned banks (Chen et al., 2023). Bank competition reduces the unfair treatment faced by private firms and lowers the threshold for them to obtain funds (Liu & Li, 2020), which provides an opportunity for firms to increase R&D investment.

The size competition view holds that the monopoly of large banks destroys the balance of loan allocation, which makes the credit funds of financial institutions lean towards large firms. Large banks are more willing to establish long-term cooperative relations with large and transparent firms and provide financing support for these firms, which make the financing constraints of large firms lower than those of small firms. Financial openness is conducive to the growth of firms with low information asymmetry, such as large and listed firms (Park et al., 2020). In contrast, small firms have few approaches to access to financial markets than large firms (Mudd, 2013); however, increased banking deregulation improves their position and thus promotes their access to bank loans (Avramidis et al., 2022). Investment by banks in relationship lending is vital for small firms to obtain bank loans (Fungacova et al., 2017). In a homogeneous market dominated by small banks, bank competition helps firms with low transparency obtain funds, whereas in a heterogeneous market controlled by large banks, bank competition prevents firms with less information from obtaining funds (Heddergott & Laitenberger, 2017).

There are a number of studies on the relationship between banking deregulation and the financing of small firms. Small- and medium-sized financial institutions’ expansion increases bank competition, which promotes the investment and growth of small firms (Hasan et al., 2017). These firms have the characteristics of asymmetric information and less collateral, which makes banks reluctant to take risks to provide loans for them. Banking deregulation is conducive to obtaining funds, reducing the unfair treatment of private and small firms and improving firm performance. Although banking development cannot fully meet the funds’ needs of small firms with comparative advantages, city and joint-stock banks reduce the financing constraints of these firms (Chong et al., 2013).

The timing of a firm's entry into the market is related to its financing channel and ability (Cowling et al., 2017; Bai et al., 2018), which may lead to differences in their R&D activities. New firms have less collateral, incomplete information disclosure and high risk, which makes them unfavourable to financial institutions and reduces their possibility of obtaining loans. In contrast, old firms have more advantages, such as asset size and market opportunities, resulting in fewer financing constraints than new firms. Hence, a high level of banking monopoly may promote firm growth, and banking deregulation is conducive to new firms.

The changes in banking deregulation may impact firms with financing constraints. The hypothesis to be tested is as follows:

Hypothesis 3: The effects of banking deregulation on the R&D investment of different types of firms are heterogeneous.

Following the previous studies (Chava et al., 2013; Cornaggia et al., 2015), new models are constructed to investigate the effect of banking deregulation on firm R&D investment.

where i, t, k and j represent the firm, year, industry and region, respectively. The dependent variable, R&D_ratio, is the R&D investment at the firm level. The independent variables, Bank_dum and Bank_num, are explanatory variables and represent the cross-regional operation of city banks at the prefecture-level city. The coefficient β captures the change in firm R&D investment. A positive value of β suggests a relatively higher R&D investment level after banking deregulation. Control represents a series of firm-level variables.

As a result of reverse causality and the omitted variables, one of the challenges faced by this study is to identify the causal relationship between banking deregulation and R&D activities. First, R&D investment is likely to be endogenous to firm and market characteristics, including banking development. Thus, a correlation between banking development and firms may make it difficult to explain the causal effects of banking deregulation on R&D investment. Moreover, banking deregulation is measured at the prefecture-level city, and R&D investment is measured at the firm level; thus, firm R&D investment cannot affect the decisions of banks at the regional level. Second, there may be omitted variables in the models that affect the estimated results, and error terms may include the unobserved regional and industry characteristics that are related to R&D investment and banking deregulation. Ordinary least squares regression makes it difficult to produce correct statistical inferences with omitted variables. The panel dataset allows the elimination of time-invariant, unobservable effects. Therefore, ωi, ηt, μk and φj are the firm, time, industry and region fixed effects. εi,t,k,j is a random error term.

Variable measuresThere are three methods to measure firm R&D investment. R&D_ratio is the firm R&D investment intensity. R&D_dum is a dummy variable that represents firm R&D investment. In addition, Ln_R&D is the firm R&D investment size. R&D_dum and Ln_R&D are used for robustness tests.

Banking deregulation enhances bank competition; this study adopts four methods to capture the branching deregulation of city banks. The dummy variable, Bank_dum, is assigned to 1 if there is a city bank from other prefecture-level cities that set up a branch locally and 0 otherwise. The continuous variable, Bank_num, is the natural logarithm of the number of branches set up by city banks from other cities. The dummy variable, State_dum, is assigned to 1 if there is a city bank from other provinces that sets up a branch locally and 0 otherwise. The continuous variable, State_num, is the natural logarithm of the number of branches set up by city banks from other provinces. State_dum and State_num are used for robustness tests.

Following the previous literature (Giebel & Kraft, 2019; Bouteska et al., 2023), the control variables include firm asset size Asset. The difference in resource endowment among firms may affect their ability to provide funds for R&D projects. The current asset ratio, Current, is an indicator to measure the cash flow of firms. When the Current is higher, it implies that firms have more free cash flow and operate better. The capital intensity, Capital, is measured by the natural logarithm of the ratio of fixed assets to employee numbers. Capital intensity reflects the fixed assets shared by an employee. The debt level, Leverage, affects cash flow and financing constraints and has an impact on R&D investment. Return on assets, Profit, controls the influence of internal financing capacity on firms. The higher the return on assets is, the stronger the profitability is, increasing investment. Subsidy controls governments’ support. Firms that conform to policy orientation can receive subsidies, which play a positive role in reducing financing constraints and increasing R&D investment. The concentration of industry, HHI, uses the Herfindahl index of the five firms with the highest sales revenue to measure market power, which controls the impact of industry concentration on R&D investment. Table 1 presents the variable descriptions.

Variable definitions.

The data on city bank branches comes from the financial licence information of NAFR, which includes the addresses, establishments, and cancellation times of more than 220,000 bank branches. The information of bank branches would be deleted from the sample after being closed; however, their information before being closed is included in the sample. This study calculates the changes in banking deregulation based on the geographical location of city bank branches. Firm data come from the Annual Survey of Industrial Enterprise. This study uses previous literature for reference to screen samples; deletes samples with fewer than eight employees and eliminates samples with at least one of R&D investment, industrial output value, total assets, owner's equity, liabilities, fixed assets and operating income less than zero or missing. The extreme values other than 1%–99% of continuous variables at the firm level are truncated, and 1,012,321 annual observations from 2004 to 2010 are obtained. The two datasets are matched using prefecture-level location information.

Table 2 reports the summary statistics of the variables. Column (6) shows the mean differences in characteristics between firms with and without R&D investment. The Spearman correlation coefficients between variables are less than 0.509, indicating that multicollinearity is not a concern.

Summary statistics.

Notes: The summary statistics of variables Ln_R&D, Bank_num, State_num, Asset, Capital, Subsidy and Age are the original values. These variables take the natural logarithm in regression tests. Columns (1)–(3) are summary statistics of the full sample.

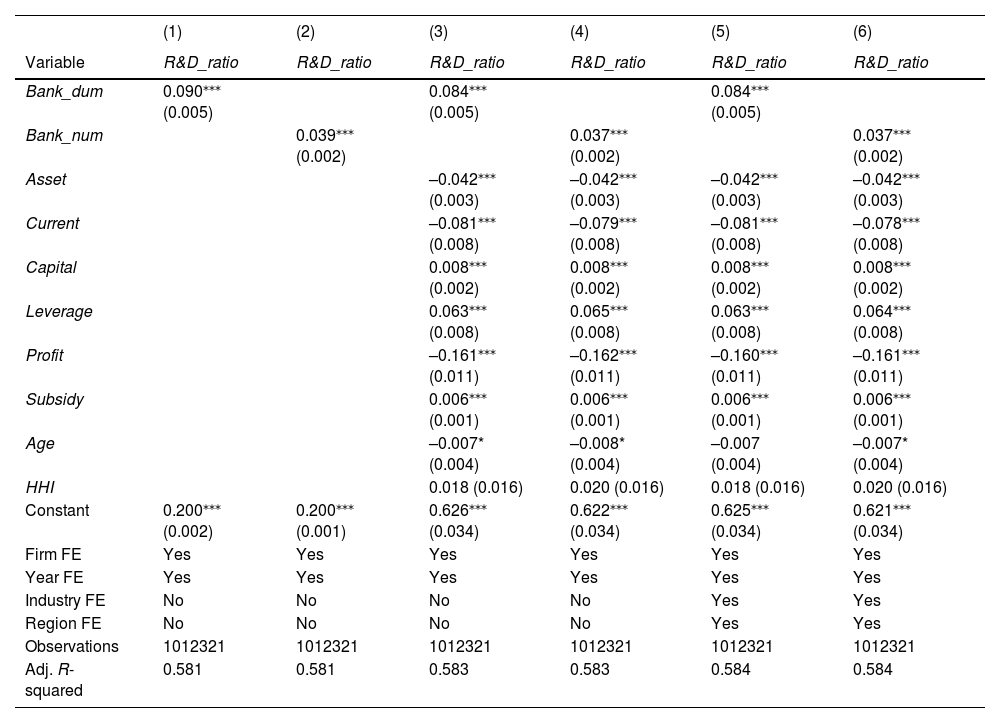

Table 3 shows the results. The control variables are not added to columns (1) and (2), and the coefficients of Bank_dum and Bank_num are significantly positive, revealing that the cross-regional operation of city banks is positively related to firm R&D investment. In columns (3)–(6), the coefficients of Bank_dum and Bank_num are significantly positive, indicating that the deregulation of city banks is positively correlated with R&D investment, which is consistent with the findings of columns (1) and (2). The result of column (5) suggests that the R&D investment of firms with cross-regional operation areas of city banks is 0.084% higher than that of firms without cross-regional city banks. Column (6) shows that for every 1% increase in the number of cross-regional branches set up by city banks, firm R&D investment increases by 0.037 percentage points. These results support Hypothesis 1, confirming the applicability of the market power hypothesis in China's financial services to the real economy. Moreover, the goodness of fit of the models is above 0.58.

Baseline regression results.

Notes: Standard errors are in parentheses. The explained variable is R&D_ratio. ⁎⁎⁎ p<0.01; ⁎⁎ p<0.05; * p<0.1.

Compared with large banks, city banks have flexible mechanisms and strong innovation ability, which meet the funding needs of R&D activities. The deregulation of city banks setting up branches across regions results in an increase in branches and competition. Therefore, the bargaining position of banks declines, whereas that of firms rises relatively. Financial institutions more easily support R&D activities than before. Banking deregulation improves the innovation ability and production efficiency of firms (Chen et al., 2023).

The results reveal that the influence of banking deregulation on R&D investment would be overestimated without considering the effect of firm characteristics. The coefficients of Asset are significantly negative, and there is a negative correlation between firm asset size and R&D investment. The greater the firm size is, the lower the R&D intensity is. Current reveals that the current asset ratio is negatively correlated with R&D investment. Capital indicates that capital intensity is positively related to R&D investment. Capital-intensive firms are more willing to invest in R&D projects to promote innovation and update production equipment. When capital intensity is higher, firms adopt more advanced equipment and technology; meanwhile, firms with low capital intensity rely on traditional production modes. Leverage has a positive correlation with R&D investment. Return on assets is negatively correlated with R&D investment. Age suggests a negative correlation between firm operating time and R&D investment. The longer the operating time is, the lower the R&D intensity is. These results show that capital intensity, liability and government subsidy cannot be ignored in increasing firm R&D investment, which confirms the rationality of the models.

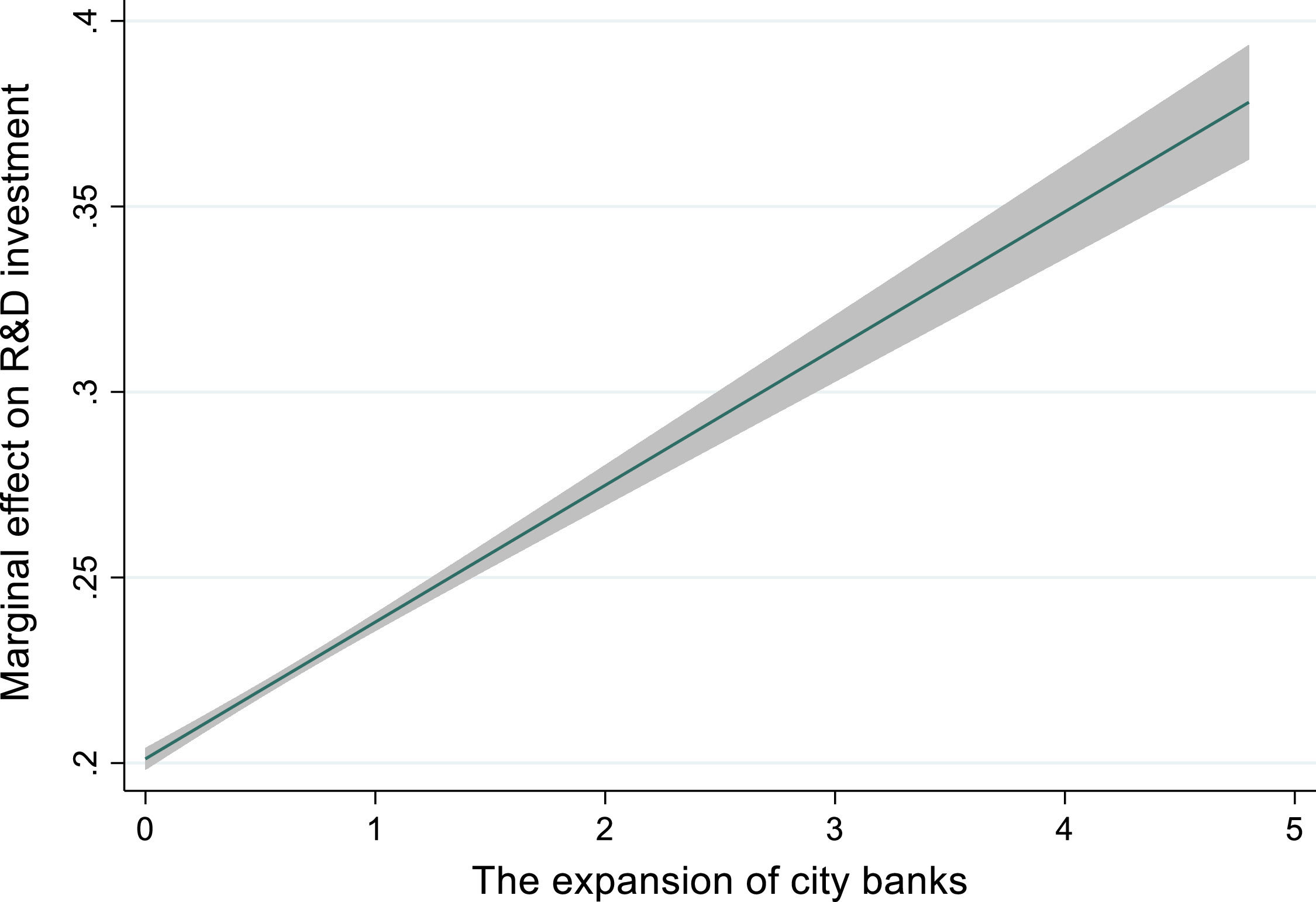

This study transforms the effect of the cross-regional operation of city banks on R&D investment into the marginal effect in column (6) and then plots it in Fig. 2. The figure shows that increased city bank branches increase R&D investment, revealing that deregulating city banks to set up branches across regions is an effective way to help firms increase their investment in R&D projects. The shaded area is the 90% confidence interval of the marginal effect of banking deregulation. When banking deregulation rose from the lowest level to the highest level, the R&D investment intensity of firms rose from 0.20% to 0.38% (Fig. 2).

Robustness tests

This subsection presents several methods to examine whether the above findings are robust to alternative measures of variables. Table 4 reports the results.

Robustness test results.

Notes: Standard errors are in parentheses. The explained variable of columns (1) and (2) is R&D_dum, the explained variable of columns (3) and (4) is Ln_R&D, and the explained variable of columns (5)–(9) is R&D_ratio. ⁎⁎⁎ p<0.01; ⁎⁎ p<0.05; * p<0.1.

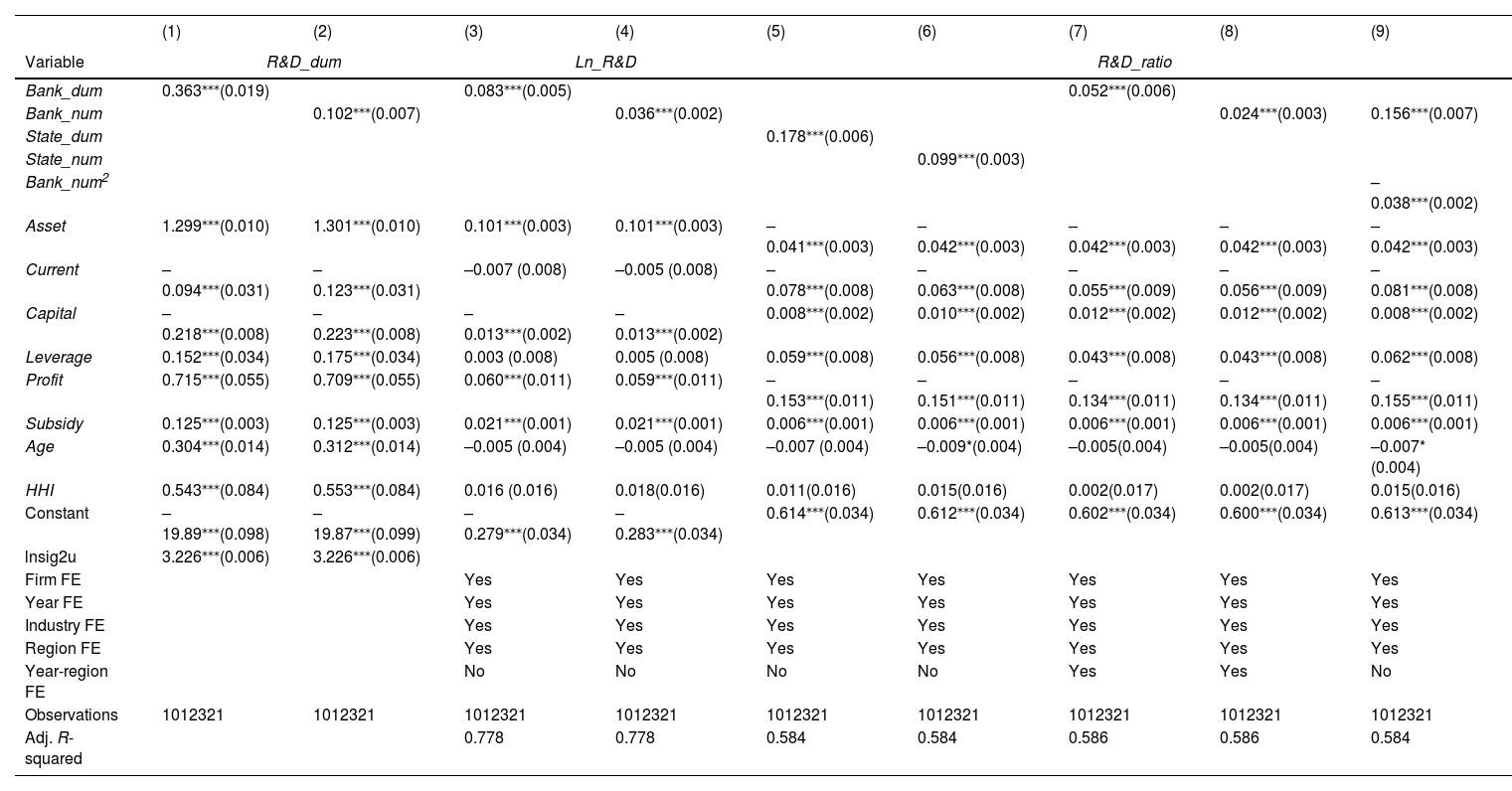

First, to avoid estimation bias caused by measurement errors of variables, this study adopts R&D_dum and Ln_R&D to measure firm R&D investment and assumes State_dum and State_num to measure banking deregulation by the inter-provincial operations of city banks. Columns (1) and (2) of Table 4 are logit model results, and the coefficients of Bank_dum and Bank_num are significantly positive, indicating that the cross-regional operations of city banks encourage firms to participate in R&D activities. In columns (3) and (4), the coefficients of Bank_dum and Bank_num are significantly positive, respectively, showing that banking deregulation increases R&D investment scale. The coefficients of State_dum and State_num are significantly positive in columns (5) and (6), respectively, suggesting that the inter-provincial expansion of city banks helps firms increase R&D investment. The inter-provincial operations of city banks can better reflect banking deregulation than cross-regional operations in the province. Compared with the results in Table 3, inter-provincial operations of city banks increase R&D investment more than cross-regional operations within a province.

Second, this study examines the omitted variables. The models may not include factors that change with regions and time and are not directly observed, which results in estimation bias. Therefore, the interaction terms of time and regional effects are added to the models, and the results are shown in columns (7) and (8). The coefficients of Bank_dum and Bank_num are significantly positive, indicating that the factors that change with the time and region do not change the evaluation of city banks’ deregulation to increase R&D investment.

Third, this study investigates the non-linear relationship between banking deregulation and R&D investment. The quadratic variable of Bank_num, Bank_num2, is included in column (9). The coefficient of Bank_num is significantly positive, and the coefficient of Bank_dum2 is significantly negative. On the left side of the inflection point, increasing the number of cross-regional branches set up by city banks (competition among banks intensifies) increases R&D investment. Meanwhile, on the right side of the inflection point, the increased number of city bank branches reduces R&D investment. Specifically, the inflection point is 2.053, and the branches of cross-regional city banks in most regions are on the left side of the inflection point, suggesting that the positive relationship between banking deregulation and R&D investment is stable. These results confirm the robustness of the findings.

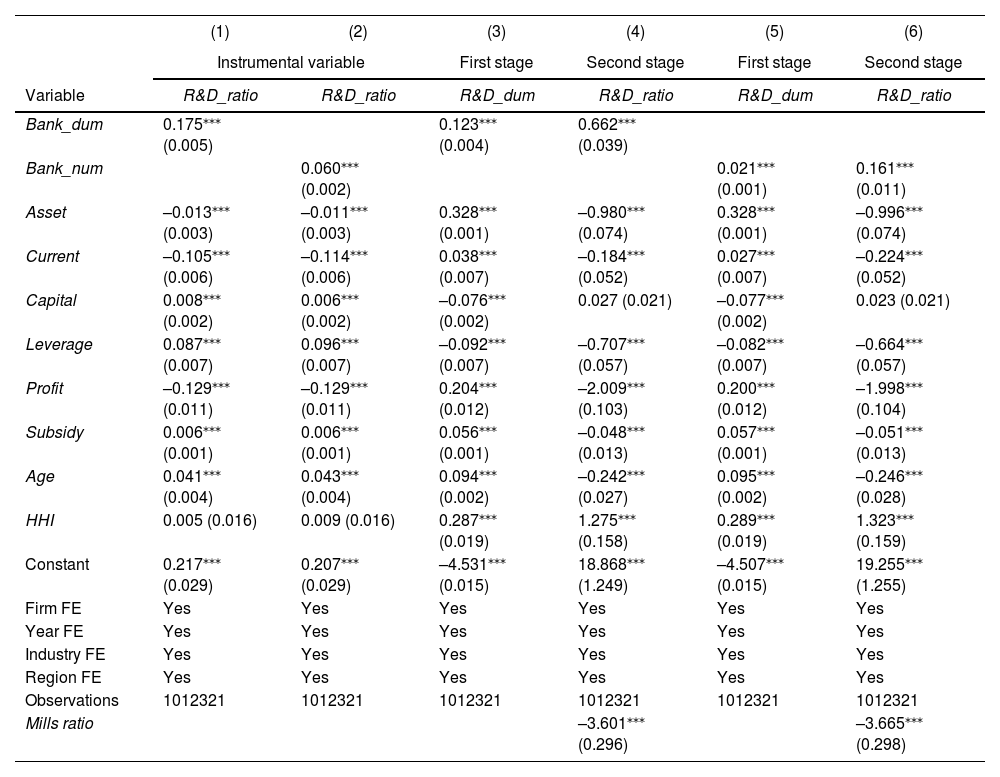

Endogeneity testsOne of the challenges in this study is identifying the causal relationship between banking deregulation and R&D investment. The cross-regional operation of city banks promotes R&D investment, and areas with more R&D activities tend to have higher economic levels, which attract city banks to set up branches. Thus, banking deregulation may be endogenous, and regional factors may affect the cross-regional operation of city banks. Reverse causality may be a factor if regional differences affect firm activities and banking development.

First, this study employs instrumental variables as an alternative identification of the effects of banking deregulation on R&D investment. This study divides the regions where the firms are located into three categories to construct instrumental variables. The first is municipalities. The second is sub-provincial cities, provincial capitals and cities with separate plans. The third is county-level regions within a prefecture-level city. This study takes the average level of banking deregulation in the same type of region (excluding the region where the firm itself is located) as an instrumental variable. The asymmetric information of R&D projects is obvious, and the transaction and information collection costs of cross-regional financing by city banks are high. Therefore, the impact of banking deregulation in other regions on local R&D activities is small. Cities at the same level and within the same region have similarities in social, economic and natural factors. When city banks set up branches, these banks are more willing to select areas with few branches and low competition. Hence, it is relevant for city banks at the same city level or within the same region to set up branches.

Columns (1) and (2) of Table 5 are the two-stage least squares results of the second-stage regressions. The F statistic is greater than 10, and the minimum eigenvalue statistic is greater than the critical value, indicating that the instrumental variables are suitable. The coefficients of Bank_dum and Bank_num are significantly positive, suggesting that setting up branches across regions of city banks is positively correlated with R&D investment after eliminating the endogenous problems. Banking deregulation is beneficial to increasing firm R&D investment, and the conclusion is valid.

Endogeneity test results.

Notes: Standard errors are in parentheses. The explained variable of columns (1), (2), (4), and (6) is R&D_ratio, the explained variable of columns (3) and (5) is R&D_dum. ⁎⁎⁎ p<0.01; ⁎⁎ p<0.05; * p<0.1.

Second, this study solves the problem of sample self-selection. A firm's participation in R&D activities is a two-stage decision. The first stage is that the firm decides whether to participate in R&D activities. The second stage is that the firm determines the R&D investment scale. Sample statistics show that a large number of firms did not participate in innovation activities, and their R&D investment was zero. If the firms that did not participate in R&D activities were deleted or treated equally with those that participated in R&D activities, the estimation results may be biased. Heckman (1978) constructed a two-stage selection model to deal with truncated data and solve the problem of selection bias. In the model, the first stage is the selection model, which examines the determinants of R&D participation. The second stage is the linear regression model, which checks the determinants of the R&D investment scale.

Columns (3)–(6) of Table 5 present the results. The inverse Mills ratio is significant, and there is a problem of sample selection bias. It is reasonable to adopt a two-stage selection model. The coefficients of Bank_dum and Bank_num are significantly positive in columns (3) and (5), respectively, revealing that the cross-regional operation of city banks promotes firms to participate in R&D activities. The coefficients of Bank_dum and Bank_num are significantly positive in columns (4) and (6), respectively, showing that the deregulation of city banks to set up branches across regions increases the intensity of firm R&D investment.

Mechanism testsIf alleviating financing constraints is a way for banks to increase firm R&D investment, banking deregulation plays a more significant role in improving the innovation ability of firms with financing constraints. From the perspective of financing, this study examines how banking deregulation affects firm R&D investment by impacting financing constraints. The models are set as follows:

where Fini,t indicates the financing constraints faced by i firm in t year. This study uses three methods to measure financing constraints. Long is the natural logarithm of the increment in firm long-term loans. Leverage is a firm's debt ratio. Cost is the ratio of interest expenses to liabilities and represents financing costs. The coefficient γ captures the impacts of financing constraints on firm R&D investment. The models include interaction terms between banking deregulation and firm financing constraints. σ captures how banking deregulation shapes the effects of financing constraints on R&D investment. External finance-dependent firms may take advantage of banking deregulation to reduce financing constraints and increase R&D investment.

Table 6 shows that the coefficients of Bank_dum and Bank_num are significantly positive, indicating that the cross-regional operation of city banks improves firm R&D investment. The coefficients of Long and Leverage suggest that the increase in financing makes firms invest more in R&D projects. In columns (1)–(4), the coefficients of interaction terms are significantly positive, revealing that banking deregulation strengthens the positive effects of reducing financing constraints on R&D investment. The coefficients of Cost suggest that increased financing costs force firms to reduce R&D investment. As shown in columns (5) and (6), the coefficients of interaction terms are statistically and significantly negative, indicating that banking deregulation lowers the negative effect of debt costs on R&D investment. These results support Hypothesis 2.

Regression results for the impact mechanism.

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variable | R&D_ratio | R&D_ratio | R&D_ratio | R&D_ratio | R&D_ratio | R&D_ratio |

| Bank_dum | 0.085⁎⁎⁎ (0.005) | 0.082⁎⁎⁎ (0.005) | 0.084⁎⁎⁎ (0.005) | |||

| Bank_num | 0.039⁎⁎⁎ (0.002) | 0.037⁎⁎⁎ (0.002) | 0.037⁎⁎⁎ (0.002) | |||

| Long | 0.002⁎⁎ (0.001) | 0.003⁎⁎⁎ (0.001) | ||||

| Leverage | 0.050⁎⁎⁎ (0.008) | 0.064⁎⁎⁎ (0.007) | ||||

| Cost | –0.053* (0.029) | –0.072⁎⁎⁎ (0.026) | ||||

| Bank_dum × Long | 0.009⁎⁎⁎ (0.001) | |||||

| Bank_num × Long | 0.002⁎⁎⁎ (0.000) | |||||

| Bank_dum × Leverage | 0.040⁎⁎⁎ (0.012) | |||||

| Bank_num × Leverage | 0.009⁎⁎ (0.004) | |||||

| Bank_dum × Cost | –0.235⁎⁎⁎ (0.053) | |||||

| Bank_num × Cost | –0.057⁎⁎⁎ (0.019) | |||||

| Control variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 1012321 | 1012321 | 1012321 | 1012321 | 1012321 | 1012321 |

| Adj. R-squared | 0.708 | 0.708 | 0.682 | 0.682 | 0.682 | 0.682 |

Notes: Standard errors are in parentheses. The explained variable is R&D_ratio.

The aforementioned results confirm that banking deregulation helps firms obtain loans, reduces financing constraints and provides a better financing environment for R&D projects. These findings are consistent with the market power hypothesis, which argues that bank competition leads to higher financing accessibility for firms. Allowing banks to set up interstate branches helps firms obtain loans and promotes R&D activities in the US, especially those firms that rely on external financing and are close to bank branches (Amore et al., 2013). The European Union relaxes the threshold of banks’ transnational operation, enhances market competition, and encourages banks to implement non-price competition strategies, which increase the entry costs of competitors (Coccorese & Pellecchia, 2022).

Heterogeneity testsDifferent types of firms have various financing channels. This section examines whether firm location, ownership, size, industry and age result in heterogeneous effects on R&D activities.

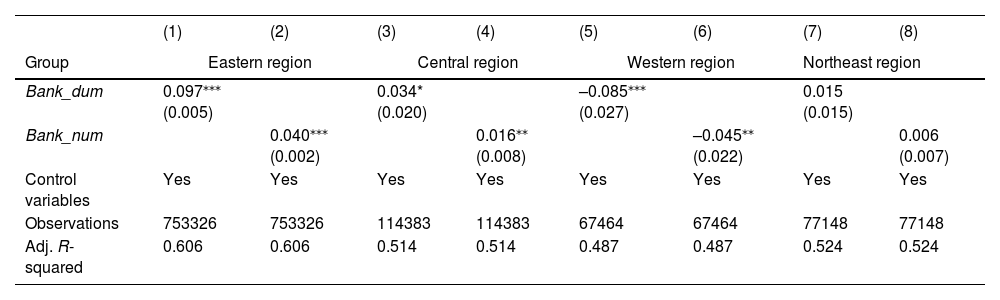

Effect of firm locationThere is a regional gap in financial development in developing countries. Compared with the central and western regions of China, city banks set up more branches in the eastern region, which may lead to regional differences in firm innovation. Areas with high economic levels have more R&D activities and stronger innovation abilities, whereas developing regions have fewer R&D activities. Does the unbalanced spatial distribution of city banks cause regional differences in R&D investment? This study divides the regions where firms are located into four categories and examines whether regional heterogeneity exists in the effects of banking deregulation on R&D investment. Table 7 shows the results.

Regression results for firm location.

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Group | Eastern region | Central region | Western region | Northeast region | ||||

| Bank_dum | 0.097⁎⁎⁎ (0.005) | 0.034* (0.020) | –0.085⁎⁎⁎ (0.027) | 0.015 (0.015) | ||||

| Bank_num | 0.040⁎⁎⁎ (0.002) | 0.016⁎⁎ (0.008) | –0.045⁎⁎ (0.022) | 0.006 (0.007) | ||||

| Control variables | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 753326 | 753326 | 114383 | 114383 | 67464 | 67464 | 77148 | 77148 |

| Adj. R-squared | 0.606 | 0.606 | 0.514 | 0.514 | 0.487 | 0.487 | 0.524 | 0.524 |

Notes: Standard errors are in parentheses. The explained variable is R&D_ratio.

The coefficients of Bank_dum and Bank_num are significantly positive in columns (1)–(4), indicating that the cross-regional operation of city banks has a positive effect on R&D investment in the eastern and central regions. On the contrary, the coefficients of Bank_dum and Bank_num are significantly negative in columns (5) and (6), respectively, showing that banking deregulation reduces R&D investment in the western region. The results may be related to the siphoning effect of city banks from the eastern and central regions on funds in the western region. Columns (7) and (8) reveal that city banks’ expansion has no effect on R&D investment in the northeast region. Note that the poor business environment in the northeast may hinder R&D activities and economic growth.

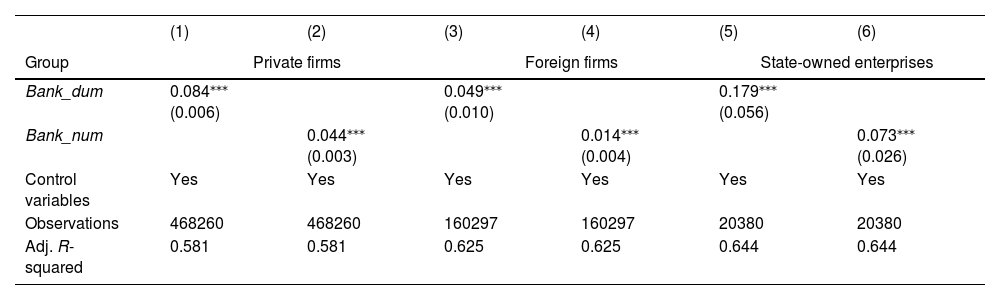

Effect of firm ownershipThere are differences in financial services provided by banks to firms with different ownership. Banks are more willing to provide funds to state-owned enterprises with more collateral and low risk (Le et al., 2019). It is difficult and costly for private firms to obtain loans (Borisova et al., 2015). This study divides firms into three categories according to their controlling shareholders and examines whether there is ownership heterogeneity in the impact of banking deregulation on firm R&D investment (Shailer & Wang, 2015). Table 8 reports the results.

Regression results for firm ownership.

Notes: Standard errors are in parentheses. The explained variable is R&D_ratio. ⁎⁎⁎ p<0.01; ⁎⁎ p<0.05; * p<0.1. The results of control variables are not reported.

The coefficients of Bank_dum and Bank_num are significantly positive, indicating that the deregulation of city banks is positively related to firm R&D investment. Specifically, the elasticity coefficients of state-owned, private and foreign firms decrease in turn, revealing that the positive effect of banking deregulation on R&D investment is heterogeneous in firm ownership. The deregulation of city banks has a stronger positive effect on state-owned enterprises than on private and foreign firms that have more information asymmetry and risk and are vulnerable to the impact and discrimination of the financial market. Statistics show that the R&D intensity of state-owned enterprises is the highest, followed by foreign firms, and that of private firms is the lowest. The aforementioned results provide evidence for explaining this phenomenon and formulating policies such as targeted incentives for firm innovation.

Effect of firm sizeThere are differences in financing channels among firms of different sizes. Small firms face more information asymmetry than large firms, which makes the financing difficulties and costs of small firms higher than those of large firms. Banking deregulation may strengthen the competitive advantage of large firms and provide sufficient funds for R&D activities. To investigate whether the effect of banking deregulation on R&D investment is heterogeneous in firm size, this study divides the observations into small, medium and large firms. This study defines firms with assets less than 40 million Yuan, between 40 and 400 million Yuan and over 400 million Yuan as small, medium and large firms, respectively. Table 9 shows the results.

Regression results for firm size.

Notes: Standard errors are in parentheses. The explained variable is R&D_ratio. ⁎⁎⁎ p<0.01; ⁎⁎ p<0.05; * p<0.1. The results of control variables are not reported.

The coefficients of Bank_dum and Bank_num are significantly positive, and these coefficients in large, medium and small firms decrease in turn. Therefore, the cross-regional operation of city banks increases firm R&D investment, and the positive effect is stronger in large firms with low information asymmetry and risk than in small and medium firms. Statistics reveal that the R&D intensity of large firms is the highest, followed by medium firms, and that of small firms is the lowest, and the gap is widening.

The results imply that the positive effect of banking deregulation on R&D investment is stronger for less opaque firms, which are less affected by information asymmetry and adverse selection, than more opaque firms. Small firm size leads to less hard information and asymmetric information, making banks underestimate the credit level of small firms. Moreover, large firms have advantages in diversified assets, scale economies, low risk and a perfect management systems (Borisova et al., 2015). Therefore, in areas where city banks set up more branches, large firms have fewer financing constraints and benefit more from banking deregulation than small and medium firms, thus investing more funds in R&D activities.

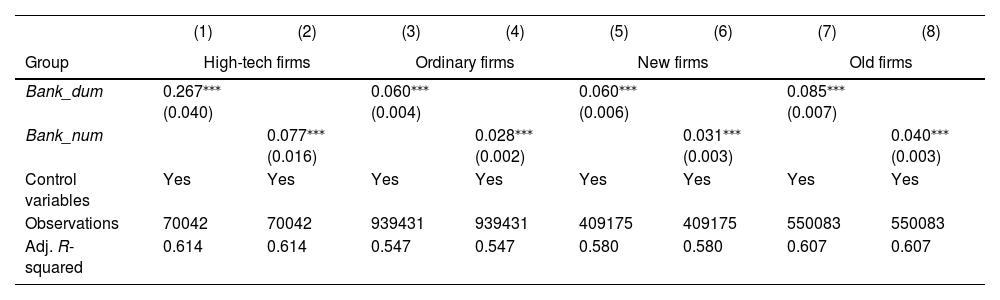

Effect of firm industryHigh-tech firms are the most active subjects of innovation activities; however, these firms face more financing constraints due to information asymmetry and high risk. Banking deregulation may have a greater impact on high-tech firms than on ordinary firms. To check whether industry heterogeneity exists in the effects of city banks’ deregulation on R&D investment, the observations are divided into high-tech and ordinary firms based on the classification of high-tech industries.

In columns (1)–(4) of Table 10, the coefficients of Bank_dum and Bank_num are significantly positive, indicating that the cross-regional operation of city banks increases the R&D investment of both high-tech and ordinary firms. The coefficients of high-tech firms are higher than those of ordinary firms, revealing that the positive effect of banking deregulation is stronger for high-tech firms than for ordinary firms. High-tech firms’ activities benefit more from city banks setting up branches across regions than ordinary firms. The decisions of high-tech firms to invest in innovation activities are sensitive to banking deregulation, which encourages these firms to obtain funds and increase R&D investment.

Regression results for firm industry and age.

Notes: Standard errors are in parentheses. The explained variable is R&D_ratio. ⁎⁎⁎ p<0.01; ⁎⁎ p<0.05; * p<0.1. The results of control variables are not reported.

There are two views on the relationship between firm age and R&D activities. The first view is that old firms have a mature route, and their internal motivation to participate in R&D activities is weak. The second view argues that the long operating life makes old firms have more knowledge and experience, and these firms are more inclined to participate in R&D activities. To test whether there is age heterogeneity in the effects of banking deregulation on R&D investment, this study divides the observations into two groups according to the median operating years of firms. Those with operating years of less than 7 years are defined as new firms, and those with operating years of 7 years or more are defined as old firms.

Columns (5)–(8) in Table 10 show that the coefficients of Bank_dum and Bank_num are significantly positive. Banking deregulation improves the R&D investment of both new and old firms. The coefficients of old firms are greater than those of new firms, revealing that the cross-regional operation of city banks promotes the R&D investment of old firms more than that of new firms. Although obtaining funds is an obstacle to old firm operations (Adegboye & Iweriebor, 2018), banking deregulation alleviates the financial constraints of these firms. Bank competition enhances commercial density by improving the credit acquisition of new firms; however, the effect weakens with increased stock market size due to the importance of information symmetry in relationship lending (Elitcha, 2021).

Conclusions and implicationsConclusionsFinancial systems are dominated by banks in many developing countries. It is the requirement of financial reforms to promote innovation-driven growth by exploring the effects of banking deregulation on firm R&D activities and its mechanisms. This study examines the relationship between banking deregulation and firm R&D investment using panel data from 1,012,321 manufacturing firms in China over the period 2004–2010. The results reveal that banking deregulation is positively associated with R&D investment, and improving financing availability is a channel through which banking deregulation promotes R&D activities. This study uses instrumental variables and the Heckman model to address reverse causality and selection bias. The robustness and endogeneity tests confirm these conclusions. The inter-provincial operation of city banks increases firm R&D investment. Moreover, the effects of banking deregulation are heterogeneous due to the differences in firm location, ownership, size, industry and age. Banking deregulation increases firm R&D investment in the eastern and central regions of China more than those in the northeast and western regions. The positive effect of banking deregulation on R&D investment is stronger for state-owned enterprises than for private and foreign firms, large firms than for small and medium firms, high-tech firms than for ordinary firms and old firms than for new firms.

Practical implicationsGiven the above findings, the implications of promoting banks to improve firm financing and innovation are as follows. First, the government should improve the legal system and policy transparency to provide an institutional guarantee for firms and banks to invest in R&D activities. The government provides a fair policy to eliminate the unfair treatment of small and private firms that belong to the long-tail group in the financial market. The government implements preferential tax policies to encourage firms to increase R&D investment. Financial regulators should improve the market access policy of banking, encourage banks to set up branches across regions and establish a warning mechanism and regulatory policies to reduce risks and financing constraints.

Second, banks should improve liquidity management and reduce the risk of non-performing loans after banking deregulation. Furthermore, they should avoid excessive concentration of customers in regions and industries and set up branches in underdeveloped areas. Banks use fintech to collect and process information, monitor capital flow, identify fund demanders, improve loan allocation and warn of risks. Moreover, it is a direction to optimise the banking structure so that small banks break the monopoly of large banks and enhance banking competition. Small banks apply fintech to compensate for the shortage of branches, which reduces the restrictions of time and geography on financial services, improves loan supply and provides funds for R&D projects.

Third, firms should improve their credit rating through the application of digital technology in information disclosure, governance and innovation projects. Due to the high risk and information asymmetry of R&D activities, firms strengthen contact with banks and utilise the financing convenience brought by banking deregulation and fintech. Small and private firms should promote digital transformation and the standardisation of financial statements to improve their operational efficiency and information transparency, which enhances digital supervision and the capital market's understanding of R&D projects and digital supervision.

Limitations and future researchAlthough this study investigates the effect of banking deregulation on R&D investment, it ignores the effect of applying fintech on firm innovation (He et al., 2023). Financial licence information provides the data of banks’ branches; however, their deposits, loans and fintech application data are not disclosed. This microdata can be collected from bank branches through questionnaires, exploring how fintech affects firm innovation and the effect of banking deregulation by affecting information asymmetry between banks and firms and financing constraints. Moreover, foreign banks have the motivation to enter developing countries, and allowing foreign banks to enter is another measure of banking deregulation (Zhang & Huang, 2022; Lyu et al., 2023). Although innovation is widely discussed in developing countries, the effect of fintech and foreign bank entry is mainly based on the observation of developed countries, and the relationship between them is misplaced. Future research should investigate the effect of fintech and foreign bank entry on firm innovation in developing countries.

Data Availability StatementData will be made available on request.

Ethics statementNot applicable.

The authors thank the editors and anonymous reviewers for their valuable comments and constructive suggestions. This work was supported by the Humanities and Social Science project of the Ministry of Education of China (Grant No. 20YJC790079), Southwest University Special Project of Studying and Explaining the Party Twenty Great Spirits (Grant No. SWU2209079) and Innovation Research 2035 Pilot Plan of Southwest University (Grant No. SWUPilotPlan025).