This paper aims to present an historical review on the evolution of Balanced Scorecard's use in Portuguese largest companies, since its appearance until the present day, and also to perform an analysis of the current situation regarding the use of this management tool in Portuguese territory. The question to be studied is – how has the use of the BSC performed and evolved in Portugal, in the last 20 years, and how the application of the tool contributes to changes in management. Initially it has been conducted research on studies carried out in Portugal about the application of the BSC, having been identified three major studies performed within the territory: the first starting the end of 1999, the second carried from 2004 onwards, the last study was conducted throughout 2009. To complete the information provided by these studies it was conducted another research on the current conditions of the use of the BSC as well as of relevant level of application depth, and its relations to organizational change and evolution on management practices. This was pursued by identification of both academic works on the subject and main technical books printed in Portugal on the theme. Thus we were able, as a result of the present study, to present a clear picture about the use of BSC in Portugal since its listing and disclosure until the present day.

The role assumed by non-financial accounting measures in the context of new management concepts such as total quality management, world class manufacturing, customer satisfaction, “the ‘Japanization’ of management” (Vaivio, 1999, p. 410), and techniques like activity based costing systems, constituted an important aspect of management change in the last decades (Vaivio, 1999). Another innovative techniques were highlighted by Ax and Bjørnenak (2005), in the management accounting field, like activity based costing, activity based management, target costing, strategic cost management or economic value added, and most changes in accounting are the direct or indirect consequences of the diffusion processes of these innovations.

Pursuing this trend of ideas, particularly in the two last decades of 20th century, it was verified the need to modify organizations’ performance indicators in order to solve the problem of organizational performance evaluation being focused only on financial measures (Kaplan & Norton, 1992, 1993, 1996a, 1996b, 1997).

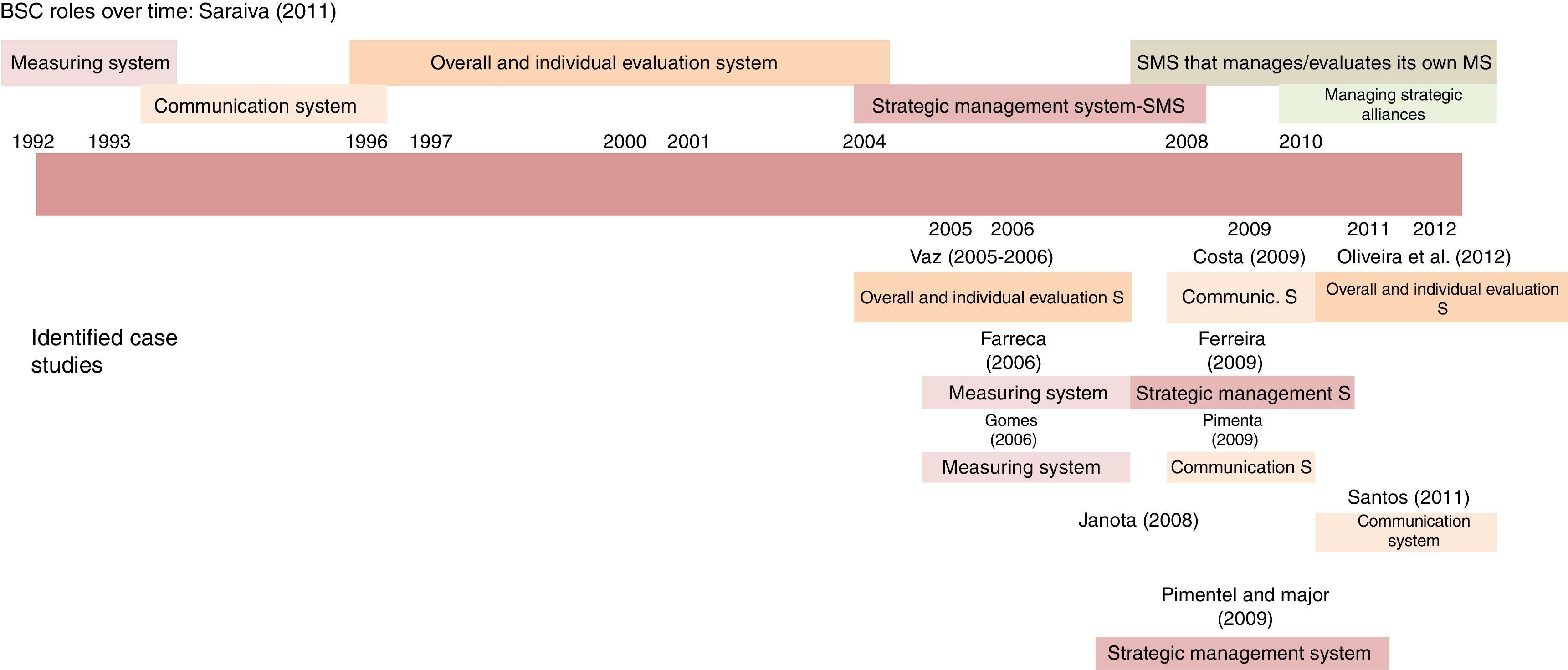

In this context, the concept of Balanced Scorecard (BSC) appeared, presented by Kaplan and Norton (1992), This notion has evolved through time as listed by Saraiva (2011), having assumed the roles of a:

- -

measuring system, consolidating a set of objectives, indicators and measures with a specific orientation, corresponding to the initial rise of the BSC;

- -

communication system: when it is used to disseminate the organization's strategic objectives;

- -

overall and individual evaluation system: each element has its defined goals, so that its activity can positively contribute to the creation of value, when the BSC begins to emerge as a tool for strategy implementation;

- -

strategic management system, used as an element to help and justify decision-making and organizational management support;

- -

strategic management system that manages/evaluates its own management system - integrating the components of intellectual capital of organizations in pursuit of strategy and initiating a path of apparent “turning outward”;

- -

system to manage strategic alliances, playing a major role in relations with the outside of the organization, using the BSC to manage strategic alliances.

From the beginning of its appearance until the present, it has been verified that this management tool brought very important changes both in organizational strategic management and in management accounting (Busco, Quattrone, & Riccaboni, 2007, Vaivio, 1999).

In order to understand the mechanisms of change, Innes and Mitchell (1990), categorized forces of change in management accounting into three different classes: facilitators, motivators and catalysts. In this paper we will try to identify the forces of change that occurred in Portugal, concerning changes induced both by the expansion of the concept of Balanced Scorecard and its actual use in the territory. It seems to us that those which can be identified as facilitators are the works presented in part two and three of the present paper; we can also assume that the fact that some of the biggest enterprises in the territory had been using the BSC, can also be regarded as a motivator by other organizations. In the present work, however, catalyst forces where not our aim.

The paper is structured as follows: antecedents and methodology are presented in Section 1; Section 2 displays an analysis of books presented in the technical literature market in Portugal on the theme of BSC; in Section 3 is completed an extensive analysis on academic works carried out in Portugal under the theme of BSC; Section 4 present an evolution of the use of the BSC in Portugal in large companies, deepening the issues related to the implementation of the BSC and its evolution; finally in Section 5, limitations and paths for future investigation are displayed.

2Antecedents and methodologyIn the present paper we made a review on the way BSC has evolved in Portugal and has influenced changes in management, following the previous roles indicated above.

We followed the works of:

- -

Malmi (2001), in the sense that this study also aims to evaluate the role assumed by BSC in Finish companies, “(…) in particular, whether BSCs are used as an improved performance measurement system or as a strategic management system” (Malmi, 2001, p. 208);

- -

Ax and Bjørnenak (2005), on the idea that the diffusion processes of the innovative tools is a way to produce change; the authors also referred the dynamic evolution of the concept; finally we highlight that they consider diffusion as the process whereby an innovation is communicated through certain channels.

Other authors indicated as themes of change in organizations, interpretations on “How and Why”, “What and Who” and “Where and When” (Busco et al., 2007, p. 127) change occurred. As we were searching to establish how the BSC concept evolved and what were the main consequences of its use in Portugal, in an historical perspective, this idea seemed to us like a good way to support the evolution of those facilitators and motivators forces, so we choose to follow the themes suggested by Busco et al. (2007).

In this way, throughout the present work, and in order to justify the perceived developments we analyzed both technical works and empirical studies conducted, as well as other material information based on facts associated with the growing availability of the notion verified in Portugal since the BSC appearance, i.e. during the last 20 years.

The themes “How and Why” and “When”, seems to us partly answered, from the evidence displayed in Sections 2 and 3 of this paper, including information on the concept of BSC conveyed to businesses and public in general, through books published in Portuguese language by national authors. We believe that this kind of disclosure was vital to the awareness of the tool, either by the public in general or by companies of any kind. On the other hand, “What and Who” and “Where and When” will be discussed in Sections 3 and 4, mainly from the perspective of those who developed work of an academic nature on the subject, an activity that has been instrumental, in our opinion, to the identification and dissemination of the use of BSC in Portugal. At this point we have to recall “How” and “When” in order to better justify the inclusion of Section 4 of the paper. In this last section these two questions are responded, and in doing so, we expect to complete an answer to the research question.

As for the research question – how has the use of the BSC performed and evolved in Portugal? – by following the verified evolution – that has shown its’ application as more usual in large companies (Schatz, 2000; Walsh, 2000) – so we have analyzed the evolution on these kinds of companies by pursuing the studies of Quesado (2010), Quesado and Rodrigues (2009), and Rodrigues and Sousa (2002).

This kind of research question is also pointed by Hoque (2014), in a review work in which he identifies investigation gaps in the area of Balanced Scorecard. In its own words: “(…) in-depth field studies in a specific country on various issues of the balanced scorecard outlined above might be enlightening.” (Hoque, 2014, p. 46). In this aspect we intend to contribute to knowledge evolution on the issue of BSC performance and evolution, and the contribution to changes in management in Portuguese entities.

The methodology used in the present paper consisted mostly of literature review and the critical analysis conducted on the evolution of BSC use over the years, concerning the identification of:

- -

technical books printed in Portugal: this kind of practice was also used by other authors such as Ax and Bjørnenak (2005), who identified, among other factors, the best-selling books on the theme of BSC in Sweden, in order to identify the ways of disclosing the concept.

- -

papers, academic texts and works: This research has been carried out during the period analysis, essentially in databases held by Portuguese universities and other institutions of higher education, and also the Repositório Científico de Acesso Aberto Português (RCAAP) database. It was also important to establish contact, in some cases, directly with the authors of some of the papers, since some works were difficult to obtain. We choose these kind of publications because in Portugal there are no professional publications in the field of management accounting (as issued in Ax & Bjørnenak, 2005, that conducted an analysis on the content of this kind of publications), but on the other hand, the theme of management accounting seems to be popular in final works of graduate courses in Portugal;

- -

scientific papers: most of them available on open access resources, and also in top level scientific journals in the study field. In order to identify papers with restricted access we have conducted researches in academic google, and then, in some cases, we contacted directly the authors.

At this initial point we will begin by listing identified works edited in Portugal on the subject of the Balanced Scorecard. This information source might be, from our point of view, a significant cause in change facilitation concerning to the implementation of the BSC. To implement the tool, it is necessary to understand it, and the technical literature has been a way of diffusing knowledge in the management area. Other facilitators were diffusion through school curriculum (at the level of post graduation courses and degree-conferring courses, either within the basic formation, or at the level of specialization), or training within the organizations (also seen as having undertaken an important role).

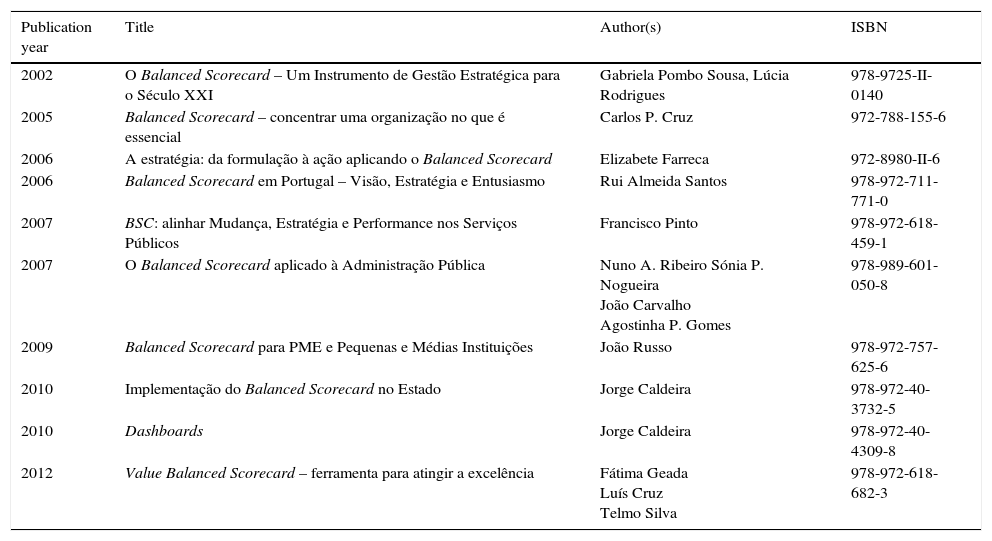

Thus, the main works of a technical nature, published in Portugal on the BSC, pursuing a chronological criterion, are listed in Table 1.

Works of a technical nature published in Portugal under the theme of the BSC.

| Publication year | Title | Author(s) | ISBN |

|---|---|---|---|

| 2002 | O Balanced Scorecard – Um Instrumento de Gestão Estratégica para o Século XXI | Gabriela Pombo Sousa, Lúcia Rodrigues | 978-9725-II-0140 |

| 2005 | Balanced Scorecard – concentrar uma organização no que é essencial | Carlos P. Cruz | 972-788-155-6 |

| 2006 | A estratégia: da formulação à ação aplicando o Balanced Scorecard | Elizabete Farreca | 972-8980-II-6 |

| 2006 | Balanced Scorecard em Portugal – Visão, Estratégia e Entusiasmo | Rui Almeida Santos | 978-972-711-771-0 |

| 2007 | BSC: alinhar Mudança, Estratégia e Performance nos Serviços Públicos | Francisco Pinto | 978-972-618-459-1 |

| 2007 | O Balanced Scorecard aplicado à Administração Pública | Nuno A. Ribeiro Sónia P. Nogueira João Carvalho Agostinha P. Gomes | 978-989-601-050-8 |

| 2009 | Balanced Scorecard para PME e Pequenas e Médias Instituições | João Russo | 978-972-757-625-6 |

| 2010 | Implementação do Balanced Scorecard no Estado | Jorge Caldeira | 978-972-40-3732-5 |

| 2010 | Dashboards | Jorge Caldeira | 978-972-40-4309-8 |

| 2012 | Value Balanced Scorecard – ferramenta para atingir a excelência | Fátima Geada Luís Cruz Telmo Silva | 978-972-618-682-3 |

Starting with a comprehensive review of the works mentioned above, it might be stated that those that have arisen in the first period, have, mainly, descriptive contents, although, those edited in 2006, have references to instances of the tool's application. One of them, which matches a case study, Farreca (2006), appears as a result of an academic study. In the second case, Santos (2006), is primarily a work of description of the tool and its potential, introducing, however, a few cases of implementation of the BSC in different companies. As for the books edited in 2007, they both present the description and the BSC framework, particularly on its adaptation to non-profit organizations in the public administration sector – yet we highlight these publications based on the fact that BSC, by that time, was already drawing attention on the sector. However, the second book also presents some insights about the use of BSC on some case studies in the public administration. As for 2009, a work emerged of a more practical nature and with features of “handbook for” the BSC methodology implementation, particularly in Russo (2009), where in addition to listing various possibilities of Balanced Scorecards – adapting the concept to the use in SMEs on different industries – it also emerges the description of some Scorecards identified in some actual applications in Portuguese companies. Concerning the works of Caldeira (2010a, 2010b), both listed here, one of them features several cases of implementation/formulation of the BSC in several public governmental organizations. The other work from the same author presents a number of technical solutions for construction and deployment of BSC, its indicators and visual shapes on the reporting theme. The last work identified, produced by Geada, Cruz, and Silva (2012), assumes the clear role of “handbook” in order to implement and use the BSC in the first part, relating the use with some aspects of management quality processes, and in a second part concerning to the presentation of several case studies performed in Portugal.

The evolution trend verified in terms of the identified works’ contents, suggests that published works of a technical nature in Portugal have a late onset if compared to the timing of appearance of BSC: only 10 years after the presentation of the concept by Kaplan and Norton (1992), was the first work of this kind published in Portugal. However, after an initial phase, the publication of works on the subject has arisen on a regular basis. It seems there is an increasing interest about the theme, not only from businesses but also from the public usually interested in technical literature in the management area.

Interestingly, the first published work in the country appears to follow the path of academic works carried out by Sousa and Rodrigues in the late 1990s of the 20th century and early years of the 21st century, resulting in the first work referred to in Table 1. Also the books in the third, fifth, sixth and seventh positions on the same table aroused as a result of academic work carried out previously by the authors. In this sense, it can be reasonably argued that the academy represented an extremely important role in the dissemination of the BSC's concept, as it was within the academic world that the first studies on the subject arose.

In other instances, yet related to the previous ones, it was found that it was through training in higher education, at postgraduate courses, initially, that some company directors contacted the concept of BSC (Farreca, 2006; Ferreira & Major, 2012), and afterwards, in courses of the first cycle in the management area. In this sense, Quesado (2010), points out as a factor of increased probability of implementation and use of BSC, the fact that managers held a college education and an academic degree. Also in terms of other learning courses in higher education, in the areas of management and economics, appeared a substantial number of works and studies on the subject, as it will be explained in the following section.

These facts appear to be in accordance with Ax and Bjørnenak (2005) paper, in the sense they also considered as an important way to communicate and spread the concept of BSC to potential adopters in Sweden. In fact, in the Portuguese case, printed technical books have been presented by Portuguese authors – and also in Sweden.

Regarding the spreading of the concept it shall also be considered the introduction of the BSC in subsidiary companies of multinational corporations operating in Portugal, as reported by Janota (2008) and Janota and Major (2012). However, after the study conducted by Quesado (2010), we may conclude that those were not a very relevant way of disclosure in Portugal.

4Academic works carried out in Portugal under the theme of BSCIn terms of works of scientific and academic features, there are several studies that can be categorized into two broad groups, according to the thematic of the applicability and of the application of BSC as such. We will address ourselves first of all to studies that approach the applicability of the concept, which is about the possibility of application of BSC to several fields of activity including proposals for concrete implementation and deployment, moving in a second stage to identify studies devoted to the analysis of cases performed in Portuguese organizations. In a later phase we will also review and analyze the works of a general scope, regarding the use of BSC, carried out in the country.

4.1Works on the subject of BSC applicabilityThe issue of applicability, often comes embedded in a context of apparent utilization, but after a deeper analysis it proves not being actual utilization in any of the stages outlined by Saraiva (2011), but rather displayed as proposals for implementation or application of the concept to a specific reality. In this sense we consider the studies held by Almeida (2011), Cavaco (2007), Gomes (2006), Janota (2008), Mendes (2012), Mendes, Santos, Perna, and Teixeira (2012), Morgado (2008), Neto (2011), Quesado and Letras (2015), Ribeiro (2005), and Santos (2009, 2011).

From the referred studies, three of them point to the implementation of BSC in school groups organizations or schools, as in Morgado (2008), Ribeiro (2005), and Santos (2009); other work addresses the possibility of application in other organizations of Public Administration, as in Gomes (2006), application to the Portuguese police system, Cavaco (2007), implementing at an hospital, and Mendes et al. (2012), the possible BSC's utilization on assessing performance in the high school system. A case study also arose in an organization on cultural industry, on Santos (2011). Janota (2008), Janota and Major (2012), presented a case study coming from the private sector, which analyzes the use of the BSC in a subsidiary of a pharmaceutical company. This work has features of a case study, corresponding at some points to an instance of effective use of the BSC. However, the way in which the work is designed and displayed makes it correspond to a mainly expositive study from the standpoint of the elements which constituted the tool. It does not leave, nonetheless, to constitute one case in which the BSC has been applied, thereby whether an integrant part on this section and either on following point: works carried out on the effective application of the BSC. This work is one of the first, among those identified by us, conducted in the private sector in profit oriented organizations.

It seems that the academic world started by proposing BSC implementation mainly in the non-profit sector at first. However, later, in recent years, many proposals for the traditional private sector arose.

Neto (2011) presents a case study which consisted of a proposal of implementation of the tool in a business unit of a group of enterprises, in the private sector, namely a producer of agricultural machinery. Another study, Almeida (2011), conducted as an overall study, yet applied only to small and medium enterprises (SMEs), indicated the issue of intentions on the tool's use by these kind of organizations and its applicability in such enterprises.

Some studies proposed the tool's implementation in Health-Clubs, such as in Mendes (2012). Other studies considered the use of the BSC, and proposed it in industrial organizations: Gonçalves (2012) proposed it in Colep, Fonseca (2011) in an Bosch business unit, Areal (2010) in a civil construction company, Patrão (2011) in Ciclo Fapril, S.A. and Forte (2012) in Fapricela, S.A.

Simultaneously, the use of the tool in non-profit organizations has also continued to evolve in the most recent years and in different areas: hospitals (Maia, 2011; Quesado, Guzmán, & Rodrigues, 2012; Silva, 2012), public administration (Duarte, 2012; Gomes, Mendes, & Carvalho, 2010, Mateus, 2010; Santos, 2012), social support (Borges, 2010), research, development and innovation (Cunha, 2010; Ribeiro, 2010).

The implementation of the tool is also considered in the Bank sector, on a paper conducted by Quesado and Letras (2015).

4.2Works committed to specific applications of the BSCIn this subsection of the present work, we choose to divide the studies about applications of BSC in Portugal in two separate groups: on the one hand case studies that analyze the BSC applications in specific organizations, and on the other hand, studies carried out globally and having as their target a particular group of organizations, designated in this work as broad scope studies.

4.2.1Case studies on the subjectAs mentioned above, at this point we will identify and analyze works which are application studies of the BSC, particularly the ones carried out as case studies, within the country under consideration. Thus, we can give as examples of case studies the works from Capelo and Dias (2009), Costa (2009), Farreca (2006), Ferreira (2009), Ferreira and Major (2012), Gomes (2006), Gomes et al. (2010), Janota (2008), Oliveira, Rodrigues, and Eiriz (2012), Pimenta (2009), Pimentel and Major (2009), Santos (2011), and Vaz (2005–2006).

With regard to the involved industry sectors, the identified cases emerged from BSC implementation in different kinds of organizations, such as sizeable private companies, as in Farreca (2006), Ferreira (2009), Ferreira and Major (2012) and Pimentel and Major (2009), and in SMEs, in Oliveira et al. (2012), as well as in public sector organizations with a strong tradition in the management control field in Pimenta (2009). This last study assumes some features of applicability work. There is also application in schools, such as in Costa (2009) and Vaz (2005–2006). The remaining case studies concerns the application in the Portuguese police system, Gomes (2006) and Gomes et al. (2010), and in a national theater, Santos (2011). These last works end up having features not of utilization but of applicability.

A different kind of study was presented by Capelo and Dias (2009), consisting on an experimental case study involving one university and a major company in the fuel distribution sector.

The four in depth studies, which relate to the utilization of the concept, are those corresponding to the use of the BSC in private companies or groups, oriented toward financial results, evidencing the use of the BSC as a measuring system (Saraiva, 2011), in the work lead by Farreca (2006), and as a strategic management system (Saraiva, 2011) in the study carried out by (2009), and also as a strategic management system, used as an element to help and justify decision-making and to support organizational management in the study presented by Pimentel and Major (2009). In the case of the study conducted by Ferreira and Major (2012), evidences point to the use of the BSC as a strategic management system that manages/evaluates its own management system, once its use aims to align and assess the strategic process resulting from a merging process and was used mainly as a way of supporting the decisions of top management rather than in an operational way. The fact that such studies were more extensive might be related to a higher level of engagement and interest in the implementation of the tool by organizations with these features, because these sort of organizations are those which are more oriented toward using this kind of tool (Quesado, 2010; Rodrigues & Sousa, 2001; Schatz, 2000; Walsh, 2000).

In the study conducted in a small and medium company (Oliveira et al., 2012), we concluded that BSC was being used as an overall and individual evaluation system.

In studies conducted in schools, still embracing the classification made by Saraiva (2011), it is apparent that the work carried out by Vaz (2005–2006) falls within the category of overall and individual evaluation system, and in the case of the study conducted by Costa (2009) as a communication system.

Lastly, in the study presented by Gomes (2006), the BSC is shown in its initial phase, as a measuring system, even though the aim of the study was on the held on checking the stage of overall and individual evaluation system; as for the works of Pimenta (2009) and Santos (2011), both can be considered in the implementation phase of the BSC as a communication system.

In Fig. 1 we represent the assumed role evolution of BSC highlighted by Saraiva (2011), and we compare it, over time, with the identified case studies, classified in accordance with that evolution.

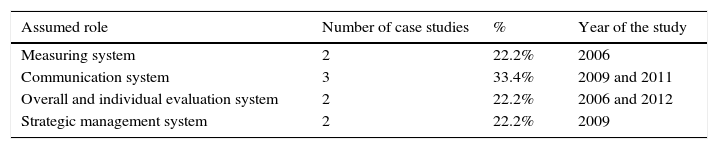

The results of this analysis appears to be that only the four initial roles assumed by BSC were being deployed: in a few cases (two), BSC was being used as a measuring system, which corresponds to the most simple way to use BSC and also to the most ineffective (Braam & Nijssen, 2004; Capelo & Dias, 2009; Madsen & Stenheim, 2014), three companies were using it as a communication system, two as an overall and individual evaluation system, and two as a strategic management system. If we consider the total number of case studies it will be found a very equitable distribution assumed by roles – as we can see in Table 2.

Case studies in which BSC was implemented and distribution by roles.

| Assumed role | Number of case studies | % | Year of the study |

|---|---|---|---|

| Measuring system | 2 | 22.2% | 2006 |

| Communication system | 3 | 33.4% | 2009 and 2011 |

| Overall and individual evaluation system | 2 | 22.2% | 2006 and 2012 |

| Strategic management system | 2 | 22.2% | 2009 |

We can conclude that only the most initial roles assumed by BSC were used in Portuguese cases studied and that case studies on the tool arose in Portugal from 2006 onwards – this may be a consequence of the (lack on) deepening degree on the awareness of the tool developments and evolutions.

4.2.2Broad scope studies on the subjectAt this point we found two kinds of studies: the ones we called generalist broad scope studies, those whose object was the whole country; and other ones we found more appropriate to classify as regional broad scope studies. The first ones were conducted at a national level, considering all companies with certain features, and the second ones were conducted within some regions of Portugal, considering, only in those regions, the companies with the desired features.

4.2.2.1Regional broad scope studiesOne study of this kind has been identified, conducted by Curado and Manica (2010), addressing the BSC use in Madeira's largest firms. This study was based upon the ranking of the largest national companies among the published ranks (top 500 and top 1000 firms) from the three highest standard Portuguese daily and weekly newspapers, and consequently studied the largest companies in Madeira, namely by questioning 163 of them. The response rate was 19%, and the study shows that only a minority of firms use the BSC: about 10%. However, from among the firms that have been using another tool, namely the Tableaux de Bord, the majority of the companies, about 23% of the total number, nearly 57% of those were planning on adopting the BSC in the near future.

The study found that companies adopting the BSC declare that its use gives them a global view of the firm, allows strategic learning and improvement and also allows them to align personal and departmental goals to strategy. The benefits in using the BSC, identified by companies, consists mainly in facing the BSC as a useful tool for enhancing financial performance, internal communication and strategic learning. As for the connections between a rewarding system and the BSC, none of the companies adopts a BSC-based reward system.

Considering the evidence brought by this study, it appears that BSC is being used in this region, yet with a low level use of the tool. It must be highlighted that the regions’ size and geographical contingencies can be a barrier to the disclosure of new concepts and management tools, and also that the fact that the region is located in one of Europe's peripheral territories can be considered as such a barrier.

However, by the general features of BSC application in the region we may conclude that BSC is being used as a measuring system, consolidating a set of objectives, indicators and measures with a specific orientation; is also being used as a communication system, since it is used to disseminate information within the companies; and also is being used as a strategic management system, used as an element to help and justify decision-making and organizational management support.

4.2.2.2Generalist broad scope studiesFrom among the studies conducted in Portugal and identified for the intended purpose, we highlight three of them, which match with three different stages of knowledge and utilization of the BSC in Portugal. The first two, considered in chronological order, comply with studies carried out in large organizations, notably in the largest Portuguese companies, which appeal to the classification carried out by certain Portuguese publications taken as a reference in the economic area: in particular the weekly newspaper Expresso, the annual ranking of 1000 largest Portuguese Companies, and Exame Magazine, the annual ranking on the 500 largest Portuguese companies.

The third study corresponds to a more recent phase and is based on a database established for research purposes, which contains only organizations identified as BSC users.

Than we have also identified other two papers – the most recent, in chronological order, displayed in the next table – which we understood as a consequence of the third study highlighted in this section.

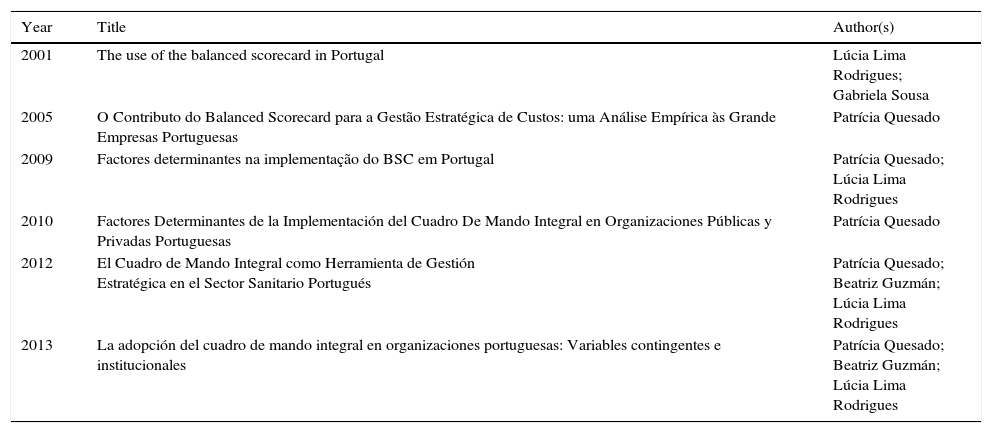

Studies that we have based the final analysis in this paper on are those presented in Table 3, in particular, the first three ones:

Works upon global scope on the implementation of the BSC in Portugal.

| Year | Title | Author(s) |

|---|---|---|

| 2001 | The use of the balanced scorecard in Portugal | Lúcia Lima Rodrigues; Gabriela Sousa |

| 2005 | O Contributo do Balanced Scorecard para a Gestão Estratégica de Custos: uma Análise Empírica às Grande Empresas Portuguesas | Patrícia Quesado |

| 2009 | Factores determinantes na implementação do BSC em Portugal | Patrícia Quesado; Lúcia Lima Rodrigues |

| 2010 | Factores Determinantes de la Implementación del Cuadro De Mando Integral en Organizaciones Públicas y Privadas Portuguesas | Patrícia Quesado |

| 2012 | El Cuadro de Mando Integral como Herramienta de Gestión Estratégica en el Sector Sanitario Portugués | Patrícia Quesado; Beatriz Guzmán; Lúcia Lima Rodrigues |

| 2013 | La adopción del cuadro de mando integral en organizaciones portuguesas: Variables contingentes e institucionales | Patrícia Quesado; Beatriz Guzmán; Lúcia Lima Rodrigues |

The works of global scope referred to, by their relevance to the analyzed subject, will be displayed and interpreted in the following section.

It should also be highlighted the great relevance assumed by these works, in particular the two initial ones, in the dissemination of the concept of BSC in Portugal. It will also be evidenced as material fact, that case studies presented earlier, most of them, have been preceded by these ones.

As a matter of fact the two last papers identified in Table 3 are not going to be analyzed in the next section, because one of them is an sectorial analysis, and the last one is an interpretation of a previous work. However, we highlight all of these studies, because all of them, aimed to characterize the use of the BSC at different time points in Portugal.

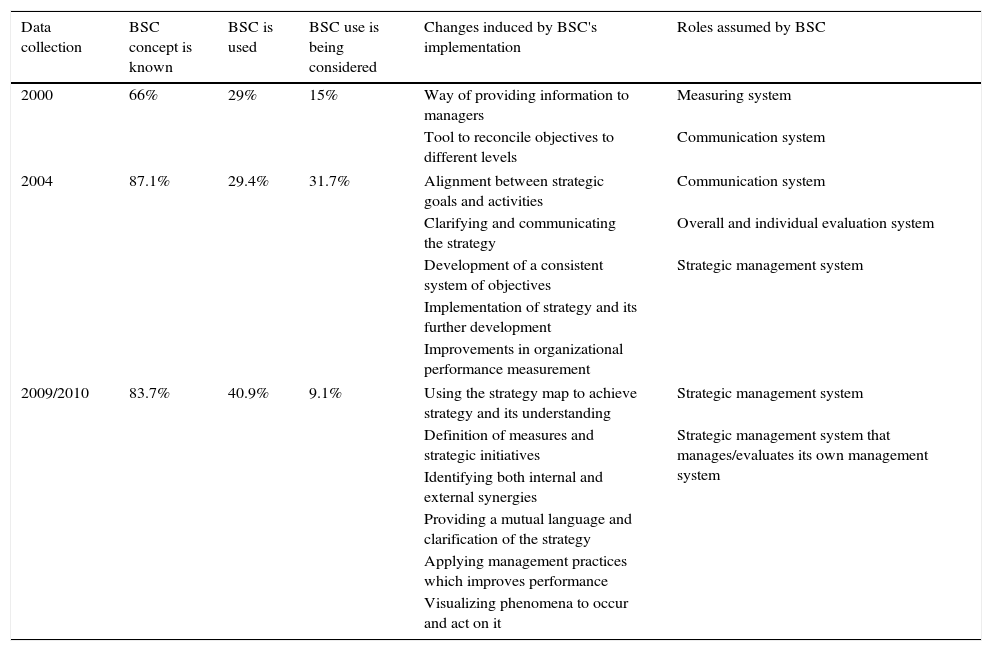

5Evolution of the use of the BSC in PortugalAt this point, and based on the studies from Quesado (2010), Quesado and Rodrigues (2009), and Rodrigues and Sousa (2002), an historical review on the evolution of the use of the BSC in Portugal will be carried out, between the year 2000, the time when data was gathered to complete the study from Rodrigues and Sousa (2001), and the years 2009/2010, when the data collection was carried out to perform the work of Quesado (2010). This overall range of time is still covered with information on the subject, presented by Quesado and Rodrigues (2009), based on figures for the year 2004, the year when was collected the data to support this work.

We highlight from these studies only some aspects, in order to find the common points between them all and in order to respond the investigation question – how has the use of the BSC performed and evolved in Portugal? – by trying to identify “Where and When”, “How” and “When” (Busco et al., 2007).

The objectives pursued by Rodrigues and Sousa (2001) were to find out to what extent BSC was being used by Portuguese companies, how they apply the concept, and if the introduction of BSC was associated with changes in management control methods. Finally, they intended to discover why Portuguese companies adopted BSC.

The study was conducted in large Portuguese companies and its main results indicate that about 14% of the companies were using the BSC, 7% were in a phase of introducing it, and 8% were considering doing so; 71% of the companies do not used it, nor had plans to do so. Considering the number of companies that were not using the BSC, the major reason was ignorance of the system, in 48% of them.

Concerning the date of adoption of the BSC, the earliest adoption happened in 1994, and all the others occurred by 1998 and 1999.

As for the use of the BSC, the majority of the companies that were using it, 63%, considered that BSC must be used to provide information to managers and to reconcile the objectives of the different levels of management, 13% considered that it must be used only to reconcile the objectives of the different levels and 25% have attributed other roles to the BSC, such as: a “system to evaluate performance” or “to organize systematically information necessary for the evolution of the company through KPI's”, Rodrigues and Sousa (2002, p. 77).

Two different ways of use were identified, one as an information system and the other as a tool to implement strategy: most companies (81%) have used it simultaneously in both ways. 13% used it as an information system and 6% used it as a tool to implement strategy.

As for perceived benefits obtained from the implementation of the BSC, companies have had, in general, a positive attitude toward the BSC, regarding it as a good management tool that brought benefits, but when inquired about changes induced by BSC, the answers were inexistent in most cases. Somehow, some of the responses had referred items such as: reinforcement of strategic reformulation and strategic alignment, getting a larger control of the implemented tasks and the existence of a major focus on key targets.

About the reasons to adopt BSC, the most pointed refer to BSC as being a mean of assessing strategy in terms of intended results; another reason, although being the less pointed, concerns the argument that BSC translates strategy into action; a considerable number of companies pointed out the two former explanations.

In general, the study suggests that at the time, BSC was not very diffused and used in Portugal, and the popularity of the concept was still reduced, however a “growing interest” was verified (Rodrigues & Sousa, 2002, p. 78). The BSC model usually introduced in these companies was that proposed by Kaplan and Norton, yet some companies did use some changes or variants on the base-model. Another characteristic verified in the surveyed companies was the use of either a little number or a large number of indicators. This was identified by the authors as risk of failure. It was also verified that in most companies the BSC results was of restricted access. For all these reasons it was considered that, despite most of the companies had faced the adoption of the BSC as a strategic management system, in fact they appear to be in the situation of using it as a measuring system and in some few cases as a communication system, the two roles initially played by BSC, according to the classification we have been using.

The second study considered, in order to present the evolution on Portuguese experience in the use of the Balanced Scorecard, was conducted in 2004 and presented in 2005. It was conducted by Quesado (2005) and it aimed to assess the applicability of the BSC in large Portuguese companies belonging to the private sector, as well as to identify how businesses managed their costs and to find out whether the companies that were adopting or considering adopting the BSC were regarding it as a tool to manage costs strategically.

As main results, concerning the state of implementation of BSC, it was found that 44.7% of companies knew the BSC concept but have not come into contact with this system, 12.9% do not know the concept of BSC, 5.9% already had taken the first steps in order to implement the BSC and 18.8% already had implemented BSC, while 4.7% dropped out of the implementation and 12.9% were expecting to implement it in the future. Results showed that the level of BSC implementation was rather low: less than 30%. About the reasons which led companies to implement the BSC, the authors highlighted the fact that the BSC seemed to be able to create connections between the strategy and individual goals, to teams and to business units. Also, BSC enables communication of the strategy out to the operational level and leads to increases in terms of understanding the inducers of the strategic success. It also leads to an alignment of the performance of employees with the strategic goals, by allowing more efficient measurement of non-financial performance. Finally, considering changes induced by the use of the BSC, companies considered that the major benefits introduced were related to the improvement in alignment between strategic goals and activities, in 84.6% of the answers. Also, the fact that BSC has turned out to be effective in clarifying and communicating the strategy and making possible the development of a consistent system of objectives; these two aspects were both mentioned in 76.9% of the companies. It was found out that in 69.2% of the responses the BSC enabled the implementation of strategy and its further development, and in 65.4% it was stated that improvements in organizational performance measurement had taken place.

Taking these results, apparently a considerable number of companies were using BSC as a communication system and also as an overall and individual evaluation system (Saraiva, 2011), in the sense that the definition of goals, appears to clarify which activities can positively contribute to value creation. A considerable number of responses, more than 65%, seemed to consider the BSC, at least partially, as a strategic management system (Saraiva, 2011), used as an element to help and justify decision-making and as an organizational management support, according to the classification followed in this paper.

The most recent study conducted in Portugal concerning to the use of the BSC is the largest and mot in depth of those considered and instead of regarding only the large companies group, has been conducted also in different kinds of organizations: small and medium companies, local governments or municipalities, municipal and inter-municipal companies, as well as hospitals. This study, Quesado (2010), approaches almost all aspects of BSC in those organizations considered. However, we will take into account, in order to establish a comparison with the previously referred papers, the results concerning only the private companies group, and in this the information related to large companies.

Concerning to the knowledge on the concept of BSC, it was found that, in general, the companies are now familiar with the tool. This leads to the conclusion that, at the time, the BSC was a concept quite well known in Portugal, Quesado (2010, pp. 212–213). Between large organizations only 16.2% referred that they did not know the tool; the rest (about 83.7%) claim to have knowledge about it, noticeably 40.9% stated a good or a total level of knowledge on the BSC, Quesado (2010, p. 213).

Regarding the implementation of the BSC, the tool was used in 38.6% of the companies, it has been abandoned by 2.3% and 9.1% were hoping to implement it in the future; 50% of the large companies have stated that they had not had used it, nor intended doing so.

The BSC perspectives used in large Portuguese companies, are, in general, those proposed by Kaplan and Norton in the base model, in line with those identified previously by Rodrigues and Sousa (2002). However, about the perspectives used in the Scorecard, some companies did not use the learning and growth perspective, in some cases being substituted by a different perspective, yet with any relation with the idea of the intellectual capital. This aspect – the lack of use of the learning and growth perspective seems to be in direct confrontation with the adaptation of the BSC in countries like Sweden, where Ax and Bjørnenak (2005) noted a high linkage with the intellectual capital model, being one of the adaptations of the model of BSC in Sweden the employee perspective. This kind of adaptation of the BSC in Portugal should be deepened in the future – as it seems to be a distinctive factor between the use of the tool in Portugal.

Concerning to this point we have to consider the opinion of Madsen and Stenheim (2014, p. 82): “Conceptual issues are related to understanding and interpreting the concept, while technical issues may arise when developing a technical infrastructure to support the BSC. Social and political issues are also common, as the implementation of the BSC may trigger many types of behavioral responses (…)” – apparently some of the responsible for managing these companies do not value either do not understand the significance of learning and growth perspective.

As for the use of the BSC, the existence of causality relationships were one of the major concerns and it was found that companies have been considering the causality relations in their scorecards (about 72% in private organizations), and from these a significant number claimed to validate statistically those relations, 53.3%. Thereof, companies stated they were using the strategy map as an element that allows them to view, simply and quickly, those components necessary to achieve the strategy and its understanding by organization members, easing the definition of indicators and strategic initiatives. The major impacts of the use of strategic maps in the Portuguese organizations turned out to be the chance of clarifying and communicating the strategy (in 76.9% of the companies), and the fact that BSC enabled and facilitated alignment between objectives and performance measures (for 88.5% of it). Other referred impacts were: the possibility of identifying both internal and external synergies, providing a mutual language and clarification of the strategy, making the resources allocation decision easier, allows showing the concern of the organization on applying management practices which improved their performance and allows visualizing phenomena which will occur in the future in advance and operate on its causes before they happen. These aspects appear to be in accordance with the findings of Madsen and Stenheim (2014), that BSC improved managerial focus in countries like Sweden, Norway and Denmark.

Taking the study information into consideration, the author (Quesado, 2010), concludes that the use of strategy maps means that Portuguese organizations face the BSC as a system for implementing and evaluating the strategy, so the BSC is not taken by those organizations only as a tool of measurement or assessment of organizational performance.

According to these findings we can conclude that by this time, in general, in large Portuguese companies, the BSC plays the role of a strategic management system, used as an element to help and justify decision-making and organizational management support. It also appears that in other cases the BSC is assuming the role of a strategic management system that manages/evaluates its own management system, integrating the components of intellectual capital of organizations in pursuit of strategy.

According to the aspects we highlighted above as relevant to clarify the answers to the research question, we will now display a summary of the issue, through time, in Table 3.

According to the previous table, it is possible to conclude how the use of the tool has evolved in Portugal, and that even the concept has had a late introduction it has become popular to several organizations.

At this point we should clarify that, in order to complete a deeper analysis considering Table 3, it should be, one more time, relieved that the study accomplished between 2009 and 2010, has not had exactly the same set of companies of the two previous ones. However, companies with desired features were included in it and it was possible to infer the data related only to these companies.

6Conclusion, limitations and paths for future investigationBased on the evidence presented, it may be concluded that despite the introduction of the BSC in Portugal has been delayed regarding the timing of the concept appearance, it has however, been developed quite significantly in terms of its implementation in large companies within the country. We identified (Table 4) that use has always been increasing, since the first documented implementation, which occurred in 1994.

Evolution of the use of the BSC in Portuguese large companies, upon studies and implementation phases considered.

| Data collection | BSC concept is known | BSC is used | BSC use is being considered | Changes induced by BSC's implementation | Roles assumed by BSC |

|---|---|---|---|---|---|

| 2000 | 66% | 29% | 15% | Way of providing information to managers | Measuring system |

| Tool to reconcile objectives to different levels | Communication system | ||||

| 2004 | 87.1% | 29.4% | 31.7% | Alignment between strategic goals and activities | Communication system |

| Clarifying and communicating the strategy | Overall and individual evaluation system | ||||

| Development of a consistent system of objectives | Strategic management system | ||||

| Implementation of strategy and its further development | |||||

| Improvements in organizational performance measurement | |||||

| 2009/2010 | 83.7% | 40.9% | 9.1% | Using the strategy map to achieve strategy and its understanding | Strategic management system |

| Definition of measures and strategic initiatives | Strategic management system that manages/evaluates its own management system | ||||

| Identifying both internal and external synergies | |||||

| Providing a mutual language and clarification of the strategy | |||||

| Applying management practices which improves performance | |||||

| Visualizing phenomena to occur and act on it | |||||

Having analyzed all the period since the appearance of the concept, we conclude that besides having a growing implementation level, it also has evolved from the first to the final stages identified as BSC's implementation roles according to the evolution of the use made of it, with exception to the final role mentioned. This last aspect is not surprising, since the final phase has emerged and was disclosed in an article presented by Kaplan and Norton by the time data collection was being gathered (Kaplan & Norton, 2010).

In these review we have tried to classify the evolution of the BSC use in Portugal, since the first studies conducted on the issue until the most recent, by the identification of the themes “How and Why”, “What and Who” and “Where and When” (Busco et al., 2007). To the theme How and Why we have tried to respond in the second and third sections of this paper by identifying how people have got information and knowledge about the concept – we found that, mainly, the concept has been introduced in Portugal by the academics – and this also responds to Why: academics tried to analyze and understand a concept that was new and was having some impact in the academic world, and also in the management practices all over the world. These leads us to Who – in the beginning of the spreading process, academics were the main actors of change, but after the concept was spreaded, business world started to adopt and use it (What an Who) – these was mainly responded on section three of the paper. The Where and When theme is mainly displayed in the fourth section of the paper: the concept has been analyzed mainly in large companies because it has been essentially used in those, as far as the When theme is was important the finding that by the time of the first study a very small number of companies used to know the concept. As a result of this scenario, the first books on the theme in Portugal were written by academics and researchers, contributing by these to the spread of the concept. In this sense we highlight the important part that the academic world has had in the disclosure and diffusion of the Balanced Scorecard concept in Portugal, as well as the important role that the tool itself has had, concerning aligning strategy with actions, as to develop the introduction of non-financial indicators.

It seems to us as predictable that, once other categories of companies verify the use of this by larger companies, that they will also consider the implementation of the tool, particularly if larger organizations disclose information regarding a favorable assessment, which appears to be validated by them, according to Quesado (2010). In the path with this idea, Malmi (2001, p. 218), states “the increasing popularity of BSCs at present may best be explained by imitative behavior (…)”, about adoption in Finish companies; also Ax and Bjørnenak (2005), referred these factor by linking the innovation to success stories from practice in Sweden.

Regarding the intentions about the implementation, in the large companies it is now found that after an initial fast growing period, when a large amount of companies were considering it, it is now being considered the future implementation by less than 10%.

However, after considering the two previous paragraphs, conditions appear to be fulfilled in allowing us to conclude that a substantial number of companies will still implement it in the future. According to Vicente, Major, Pinto, and Sardinha (2009), in an analysis on the management controllers’ functions and roles, in Portugal, it was found that the BSC is regarded as one of the important tools and techniques for effectively discharging the functions of management controllers. This tool has been assumed as playing a prominent role as a way of change in management: “… are still considered important, with over 50% rating, in the option of utmost importance, the following factors: new techniques and management methodologies (Activity-based Costing, The Balanced Scorecard, etc.)., new styles and management practices; development and accessibility of new technologies of information and communication, organizational restructuring initiatives and market-oriented business.” (Vicente et al., 2009, p. 71). All these arguments, along with the fact that some large companies are still considering the implementation of the BSC in the future, seem to indicate that evolution about the use and also about the abandonment of the tool can and should be studied in the future. In particular and concerning largest Portuguese companies, it would be interesting to conduct a study that completes the two large scope ones presented in this paper, focusing either on studied subjects and on issues like the use of the BSC as a system to manage strategic alliances and to assess the management system.

Other possibilities are the deepening on the subject related with the inexistence and/or adaptation of learning and growing perspective – this can be explored in an cultural aspect on the leadership, being the leadership a theme pointed by some authors as an opportunity to develop new paths of research in the future (Hoque, 2014; Kaplan, 2009).

Another important issue is the apparent gap between the use of the scorecard and the benefits obtained from it – in this field we can also recall Hoque: “Future studies could investigate whether and how causal relationships among balanced scorecard perspectives could be the outcome of facilitating strategic organizational and employee learning, and could assess the impact on organizational strategic outcomes” (Hoque, 2014, p. 48).

As to the limitations of this paper, being an analytical review, we can always not consider some relevant study or paper that we could not identify – we tried to overcome this issue by completing an exhaustive search of studies, books, scientific articles and other sources on the field. However, this procedure, can also be considered, itself, as another limitation, since we have considered several kinds of sources, and not only scientific articles. Yet this kind of practice as already been carried out by other authors.

Another limitation is that, having considered some different studies with diverse characteristics, we have had to choose and adapt some of the results of those studies in order to sustain our analysis, however this situation often occurs when working with secondary data.

PEst-OE/EGE/UI4056/2014 – financed by Fundação para a Ciência e Tecnologia (FCT).

http://repositorium.sdum.uminho.pt/bitstream/1822/332/1/luciarodrigues2.pdf, accessed in January 2012.

http://www.rcaap.pt/directory.jsp?locale=pt, accessed between November 2010 and August 2012.

www.publicationethics.org.