The organizational structure of multinational enterprises (MNEs) is mainly made up of subsidiaries located in emerging and advanced countries. Consequently, they usually compete against the same rivals simultaneously in both emerging and advanced contexts. Multimarket contact (MMC) theory analyzes the competitive dynamics that arise in these situations. However, researchers have paid more attention to the consequences of multimarket contact in developed countries than to its effect in emerging countries. To explore the impact of the macroenvironment on the relationship between MMC and performance, we examine how coinciding with multimarket rivals in emerging economies alters the effect of MMC on firm performance. Our research, which is developed with a sample from the mobile telecommunications industry, shows that the presence of MNEs in emerging countries hinders the development of mutual forbearance practices and, therefore, reduces the positive effect of MMC on firm performance.

In recent decades, countries from Asia, Latin America, Africa and the Middle East have undergone a process in which government policies have favored economic liberalization and the adoption of free-market systems (Hoskisson et al., 2000). These countries are known as emerging market economies and, despite the efforts of governments to move toward a market-based economic system, they are characterized by governmental discretion, political instability and poor property rights protection (Meyer et al., 2009). In spite of these institutional voids, emerging economies can be an opportunity for foreign investors because of the growth in demand for many industries in these economies (Hoskisson et al., 2000). As a consequence, multinational enterprises (MNEs) often base their organizational structure not only in countries with a higher institutional stability, that is advanced economies, but also in emerging economies.

Because of the large number of countries in which MNEs are present, it is likely that they will compete with the same rivals in different markets at the same time. Thus, besides the complexity of managing different subsidiaries, MNEs also have to manage the consequences of competing against the same rivals in both emerging and advanced markets. Multimarket contact theory analyzes the competitive dynamics that arise in these kinds of situations, that is, when firms meet each other simultaneously in different markets (Karnani and Wernerfelt, 1985). Due to the current globalization of competition, multimarket contact (MMC) has become a frequent determinant of rivalry between firms (Greve, 2008; Yu and Canella, 2013) and, therefore, MMC theory has gained momentum among strategic management scholars (Greve, 2008; Guedri and McGuire, 2011; Upson et al., 2012). Nevertheless there is still no general agreement about the consequences of coinciding in multiple markets on interfirm rivalry. On the one hand, some scholars have defended a linear relationship between MMC and rivalry (Gimeno and Woo, 1996; Gimeno and Woo, 1999; Greve, 2008). According to these scholars, increases in MMC would always result in a low rivalry between firms. On the other hand, other researchers have suggested that the relationship between MMC and the intensity of rivalry may be represented as an inverted U-shape (Baum and Korn, 1999; Fuentelsaz and Gómez, 2006; Haveman and Nonnemaker, 2000). These researchers argue that, when MMC is low, rivalry between firms tends to be high. However, when MMC is high, MMC rivals tend to tolerate each other and, as a consequence, the rivalry between them lowers.

Apart from studying the relationship between MMC and interfirm rivalry, research has also paid a lot of attention to the contingencies that moderate the mutual forbearance hypothesis (Yu and Canella, 2013). For instance, Gimeno (1999) examines how the strategic importance of markets affects the reduction of rivalry between firms in MMC environments. Haveman and Nonnemaker (2000) explore the effect of mutual forbearance in markets dominated by a few large firms. Fuentelsaz and Gómez (2006) analyze the impact of strategic similarity among rivals on MMC dynamics and Vonortas (2000) studies the consequences of market and technological uncertainty on mutual forbearance agreements. As these examples show prior research has mainly focused on how industry and firm characteristics moderate the effect of MMC on firm performance. However, with few exceptions (see Yu et al., 2013), the impact of the characteristics of the macroenvironment on the relationship between MMC and performance has been underexplored. To our knowledge, there is no previous study that analyzes whether the relationship between MMC and performance is the same for subsidiaries in emerging economies, prior MMC studies having tended to focus on advanced economies.

Recent literature has highlighted how the features of emerging markets can change the findings of traditional managerial theories that have mainly been developed in advanced economies (Hoskisson et al., 2000). While some authors suggest that it is necessary to develop new theories to explain the behavior of firms in emerging economies, others understand that traditional theories are still applicable but need to be extended if we are to better understand the behavior and outcomes of firms in this context (Cuervo-Cazurra, 2012). This article seeks to analyze the extent to which market overlap in emerging countries conditions previous theory about the effect of MMC on firm performance.

This research argues that MMC has a U-shaped effect on firm performance and we examines the influence of MMC on firm performance, taking into account the degree of market overlap of MNEs in emerging countries, that is the number of emerging countries where MNEs encounter their multimarket rivals in relation to the total number of markets in which they compete against multimarket rivals. We propose that MMC is more effective in reducing interfirm rivalry when multimarket rivals meet in advanced markets rather than in emerging markets. Our underlying logic is that the observation of rivals’ behaviors and internal coordination among subsidiaries may be more difficult in emerging economies due to information asymmetries, uncertainty and higher requirements of local adaptation. As a consequence, mutual forbearance dynamics could arise more naturally in advanced markets than in emerging markets. We test our hypotheses in the mobile communications industry from 2000 to 2012 by considering MMC between the whole population of MNEs that coincide in emerging and non-emerging markets around the world.

The contribution of this study is twofold. First, we provide evidence of the effect of MMC on firm performance in an international context. Whereas prior research mainly focused on examining how industry and firm characteristics determine the effect of MMC on rivalry, we pay attention to the moderating influence of the macroeconomic context on MMC dynamics. Second, we extend MMC literature by suggesting that MMC is more effective in decreasing rivalry and creating above-average returns when it mainly takes place in advanced markets rather than in emerging markets. A better understanding of how the context influences the effect of MMC on firm performance can enrich MMC theory and clear up some concerns about MMC dynamics.

The rest of the paper is organized as follows. In the second section, we review the literature about MMC and the main characteristics of emerging countries. This will help us to better understand the hypotheses of the third section. The fourth section addresses the variables and the methodology, and the results are presented in the fifth section. The last section is devoted to the main conclusions and future research lines.

Literature reviewMultimarket contact competitionMMC theory describes the competitive dynamics among firms that compete against each other across several markets (Karnani and Wernerfelt, 1985). In the first stage, MMC increases the chance of direct competition. However, MMC theory defends the mutual forbearance hypothesis – i.e. the reduction of rivalry between multimarket firms due to the MMC between them – and sustains that multimarket rivals tend to refrain from aggressive competitive behaviors in their common markets (Greve, 2008; Parker and Röller, 1997; Spagnolo, 1999; Bernheim and Whinston, 1990). Multimarket competition implies that firms are able to respond to an attack in the market where it takes place, in the most important markets for the attacking firm or even in all the markets where both firms compete. As a consequence, multimarket firms tend to balance the chance of achieving an advantage in one market with the risk of receiving retaliatory responses in several markets or in the most important ones. The high risk of retaliatory responses, which could negatively affect firm performance, reduces the motivation of multimarket rivals to initiate aggressive competitive moves (Gimeno, 1999).

The debate about the effect of MMC on rivalry is still open in the MMC literature. Some authors suggest that the relationship between MMC and rivalry is linear (Fu, 2003; Gimeno and Woo, 1996; Gimeno and Woo, 1999; Greve, 2008; Upson et al., 2012). Accordingly, rivalry between multimarket rivals should always decrease as the number of MMCs rises. However, other scholars have qualified this contention by arguing that the relationship between MMC and rivalry may show an inverted U-shape (Baum and Korn, 1999; Fuentelsaz and Gómez, 2006; Haveman and Nonnemaker, 2000). These authors sustain that a certain level of MMC is necessary for multimarket rivals to become aware of their interdependences and begin to mutually forbear. Before reaching this point, rivalry between multimarket firms is intense because the risk of retaliatory responses is not yet an important threat, the recognition of competitive interdependences has not taken place and firms might have incentives to show their competitive abilities.

Prior literature has noted that two basic conditions must come together in order to achieve the mutual forbearance: full observability and effective internal coordination between subsidiaries (Yu and Canella, 2013). First, deterrence among multimarket rivals requires that defections from equilibrium can be detected and punished. As a consequence, MMC research tends to assume that mutual forbearance takes place in a fully observable context (Greve, 2008; Thomas and Willig, 2006; De Bonis and Ferrando, 2000). Second, the implementation of a mutual forbearance strategy needs an efficient internal coordination among subunits (Golden and Ma, 2003; Jayachandran et al., 1999; Ma, 1998). The possibility of observing rivals’ actions, as well as the ease of coordination between a MNE's subsidiaries, might be lower in emerging economies due to information asymmetries, uncertainty and the requirements of local adaptation.

Emerging and advanced economiesAn emerging market economy satisfies two criteria, “a rapid pace of economic development and government policies favoring economic liberalization” (Hoskisson et al., 2000: 249). Despite the rapid demand growth in emerging economies and their efforts toward market openness, these economies still have some institutional voids that lead to different “rules of the game” (North, 1990) than those of advanced economies.

Hitt et al. (2000: 451) highlights the difficulties of MNEs to operate in emerging countries because “the economic and sometimes social instability in emerging markets produces ambiguity and uncertainty regarding the rules of exchange”. Since financial markets are incipient, there is a high volatility and risk in making investments. Moreover, Hoskisson et al. (2000) argue that emerging economies are characterized by underdeveloped legal infrastructures, insufficient property rights protection and political discretion that result in opportunistic behavior of market agents, information asymmetries and market uncertainty. These characteristics increase information and enforcement transaction costs of developing business and make network contacts and personal relations more important to reduce the uncertainty derived from the institutional infrastructure (Johanson and Vahlne, 2009). Thus, emerging economies are a more complex arena in which to develop business than advanced economies. The latter are characterized by lower uncertainty because of the strong development of legal, judicial and executive systems that increase the available information in a market and improve the predictability of the actions of market agents, such as suppliers, consumers and competitors (Meyer et al., 2009).

HypothesesMMC and firm performanceInitial evidence of an inverted U-shape in the relationship between MMC and competitive behavior has been found for market entry rates (Baum and Korn, 1999; Fuentelsaz and Gómez, 2006; Haveman and Nonnemaker, 2000; Stephan et al., 2003), exit rates (Baum and Korn, 1999) and growth rates (Haveman and Nonnemaker, 2000). According to these authors, when MMC is low firms have incentives to establish a foothold in the markets of their rivals to signal their capacity to defend themselves from competitive moves (Karnani and Wernerfelt, 1985). These initial actions may provoke similar responses from competitors, increasing the level of rivalry (Baum and Korn, 1999). As the number of contacts increases, MMC rivals become aware of the harmful consequences that a process of competitive escalation in multiple markets would have on their performances. Once the level of MMC where firms are aware of their interdependences is reached, rivalry is reduced and firms begin to mutually forbear in their common markets (Spagnolo, 1999).

With very few exceptions (see, for example, Fuentelsaz et al., 2012), the inverted U-shaped relationship between MMC and rivalry has been found when measuring rivalry through firms’ actions such as markets entries or exits. We argue that the curvilinear relationship may also be applied to analyze the relationship between MMC and firm performance. When firms coincide in more than one market, their dependence on similar resources increases (Hannan and Freeman, 1993). Competition for productive factors and consumers has a negative effect on firm performance (Porter, 1985; Scherer and Ross, 1990). Nevertheless, as multimarket rivals become aware of their interdependences, they begin to develop mutual forbearance practices and avoid competitive escalation. The lack of competition allows multimarket rivals to obtain a higher performance. As a consequence, the effect of MMC on firm performance should be U-shaped. Accordingly, our first hypothesis proposes:H1 MMC between MNEs has a U-shaped effect on firm performance.

We have said mutual forbearance requires two boundary conditions to improve firm performance, namely, full observability and internal coordination among the MNE's subunits. Regarding the first condition MMC models tend to assume that violations of mutual forbearance agreements can always be detected and punished (Greve, 2008; Thomas and Willig, 2006; De Bonis and Ferrando, 2000). However, controlling the compliance of collusive agreements may be complicated in emerging countries. Information asymmetries, which tend to be magnified in these contexts (Tong et al., 2008; Meyer et al., 2009), may encourage the breach of mutual forbearance agreements by reducing the chance of detecting violations and, therefore, of being punished. In addition, in emerging economies, political instabilities and shocks frequently increase environmental uncertainty (Hoskisson et al., 2000), which makes deviation from collusive agreements even more difficult to detect. Thus, information asymmetries and uncertainty in emerging countries may hinder the observation and interpretation of the actions of multimarket rivals. In this scenario, MNEs may have incentives for opportunistic behaviors and for deviating from mutual forbearance agreements.

Mutual forbearance also requires the internal coordination and integration of all the subsidiaries (Golden and Ma, 2003; Ma, 1998). For instance, if a particular subsidiary initiates a competitive move in an attempt to improve its position in the country where it operates, this move could provoke retaliation from a multimarket rival and losses for the MNE in other countries where it is competing. For the threat of retaliation to be credible MNEs must have an efficient internal coordination to enable rapid answers in a certain market against the attacks that have been suffered in other markets. Hence, in absence of intra-firm coordination, MMC might evolve into a market-by-market competition process, in which mutual forbearance does not occur (Jayachandran et al., 1999). International business literature has shown that MNEs often find it difficult to coordinate across markets because subsidiaries feel pressure to be locally responsive rather than globally integrated (Prahalad and Doz, 1987; Yu et al., 2009). The need to be locally responsive is even more intense in emerging countries because the success of MNEs in these economies depends, to a great extent, on their integration into local networks and their adaptation to local governments (Guillén and Garcia-Canal, 2009; Hoskisson et al., 2000). In fact, MNEs usually enter emerging economies through alliances with local partners. In that way, they expect to achieve a greater integration with the local networks and the institutional environment (Johanson and Vahlne, 2009). Local partners facilitate access to emerging economies, but, at the same time, they make the global coordination of subsidiaries and the implementation of common guides from headquarters difficult. As a consequence of local adaptation and agreements with local partners, MMC dynamics and mutual forbearance may not be operational when MNEs mainly compete against their multimarket rivals in emerging economies.

According to prior arguments, mutual forbearance among MNEs is more complex when they mainly coincide in emerging markets. The lack of observability and the difficulties of coordinating subunits in these markets hinder the recognition of competitive interdependences and, therefore, prevent the establishment of collusive agreements among multimarket rivals. Therefore we expect that the greater the percentage of market overlap between MNEs in emerging economies, the greater the difficulties to develop mutual forbearance practices and, thus, the weaker the positive effect of MMC on firm performance.2 The second hypothesis of our theoretical model states that:H2 The greater the percentage of MMC in emerging countries, the lower the positive effect of MMC on firm performance.

The mobile telecommunications industry is a suitable setting for the purposes of this paper for several reasons. First, in the 90s, this industry underwent a process of openness in which operators started to enter new markets (Gerpott and Jakopin, 2005). This increase in market entries led to a rise in the number of points of competition between firms. A time frame from 2000 to 2012 allows us to study the full impact of MMC on firms’ results, moving from a situation where MMC was nonexistent to a situation with a moderate level of MMC.

Mobile groups3 are present all over the world, in both developed and emerging countries. The European Union (EU) countries are examples of countries with strong institutions that support economic exchanges under a common industry regulation. Under the legal directives of the EU institutions, the mobile telecommunications industry has achieved a high penetration rate in these countries because of a common technological standard, GSM, in the first stages of mobile communications. This favored the creation of strong European mobile multinationals, such as Telefonica and Vodafone, that started operating in the EU markets and that are present in emerging countries as well.

In the vast majority of emerging countries, GSM was imposed by the national authorities not regionally as in the EU during the 1990s (Fuentelsaz et al., 2005). The adoption of the GSM standard allowed interconnectedness with other regions, favoring the development of communications. Despite the late introduction of mobile telecommunications in emerging countries, their large growth in recent years has slowed down the penetration of fixed telephony (Barros and Cadima, 2000) and has allowed the entry of foreign MNEs and the creation of new MNEs with their origin in an emerging economy.

SampleThe mobile telecommunication industry is suitable for the purpose of this paper and we use the information provided by GSMA Intelligence.4 This information includes quarterly data for 51 international mobile groups and 132 countries within a timeframe that covers 2000–2012. The countries are divided into emerging countries and non-emerging countries. To classify the 132 countries of our sample into emerging and non-emerging, we have followed the standard of the International Monetary Fund (IMF), which leads us to consider 16 of the countries as emerging5 and the other 116 as non-emerging.

VariablesDependent variableOur objective in this paper is to analyze whether the effect of MMC on performance could be altered when that MMC takes place in an emerging country. Therefore, our dependent variable is the performance of international mobile groups. Following previous studies (Jakopin and Klein, 2012; Sung, 2014; Fuentelsaz et al., 2012), we use the EBITDA margin – earnings before interest, taxes, depreciation and amortization expressed as a percentage of total Revenue – as a measure for the international mobile groups’ performance. Therefore our dependent variable – the EBITDA margini – is a ratio where the numerator is the total EBITDA of the group (EBITDAi) and the denominator is the total Revenue of the group (Revenuei).

Independent variables

In order to test our first hypothesis, we need to calculate the Multimarket Contact (MMC) that each group has with the rest of the groups of the sample. We consider that there is one multimarket contact between two international groups when they compete in two markets at the same time. For example, Vodafone and Telefonica were incumbents in Germany at the beginning of our timeframe. When Vodafone entered Spain in 2001,6 where Telefonica had launched its services some years before, it established the first MMC between these two groups.

To construct our measure of MMC, we begin with a simple measure of MMC – that is the total number of markets where the focal international group encounters the rest of the groups. In order to be included in this first measure of MMC, we require that each pair of groups meets in at least two markets since only then is there multimarket contact between them. If the focal group only competes with a certain rival in one market, this pair of groups is not included in the simple measure of MMC of the focal group.

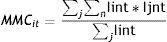

Once we have the simple measure of MMC between the focal group and its multimarket rivals, we need to weight it since each group competes with a different number of multimarket rivals (Gimeno and Jeong, 2001). For instance, it is very different if group i encounters its 3 multimarket rivals in 6 markets than if it has the same volume of MMC but only with one multimarket rival. In the first case, group i has fewer MMCs than in the second. So we weight the simple measure of MMC by the number of multimarket rivals that the focal group has.

Therefore, our measure of MMC for each group and time – MMCit– is calculated as follows:

where j and n refer to a certain multimarket rival and country, respectively, Iint is a dummy variable that takes value 1 if group i is present in market n and 0 otherwise, and Ijnt is a dummy variable that takes value 1 if group j is present in market n, and 0 otherwise. Therefore, the numerator of our MMC variable calculates the number of markets where the focal group i encounters each other group, j, included in our sample. As mentioned before, only those pairs of groups that meet in at least two markets are included in the numerator. The denominator of our MMC variable measures the number of multimarket contact rivals of the focal firm i.

To illustrate this variable, we give an example. If we take Vodafone as the focal group, we first need to count the number of markets where it competes with the rest of the groups. Taking into account the premise of competing in at least two markets at the same time, at the end of 2012, Vodafone competes in 2 markets with Bharti, 4 with Deutsche Telekom, 5 with Orange, 4 with Hutchison, 2 with KPN, 2 with MTN, 3 with OTE, 5 with Telefonica and 2 with Turkcell. Thus, Vodafone has a total of 29 market overlaps with the rest of the groups that is the numerator of the ratio.7 Since it has 9 multimarket rivals at that time, the denominator of our variable, we divide the total number of market overlaps by 9. Therefore, in the last period of 2012 Vodafone has 3.222 MMCs with the rest of the international groups that are included in our sample.

Our second hypothesis proposes that the higher the percentage of MMC in emerging countries (%MMCEC), the lower the positive effect of MMC on firm performance. Therefore, our measure of MMC in emerging countries is expressed as a percentage of total MMC.

Total MMCi is calculated in the same way as the MMC variable used to test our first hypothesis, that is, by adding up the total number of markets where group i encounters its multimarket rivals j. MMC in emerging countriesi is the total number of emerging markets where group i competes with each of its multimarket rivals j. As in the construction of our MMC variable, we require group i to meet a certain rival group in more than one emerging market in order to include the pair of groups in the measure of market overlap in emerging countries of group i.

Control variablesWe control for some group and market characteristics. Regarding the group characteristics, we control for the size of the group since a bigger group may achieve better results more easily. We measure the size of the group by its Total Connections.8 Furthermore, since our dependent variable of performance does not distinguish between the markets of the focal group i but is common for every market where i is present, we include a variable of the Number of markets where the focal group is present. The argument rests on the idea that a group that is present in 10 countries has more markets that allow it to generate results than a group that is only present in 3. Therefore, one could expect the performance variable of the first group to be bigger than the total performance variable of the second.

In relation to market characteristics, we control for market concentration – measured through the Herfindahl Index – since it has been said that more concentrated markets lead to better results due to the lack of competition (Gómez and Maícas, 2011; Sung, 2014). Since our dependent variable does not distinguish the amount generated by each market that makes up the total performance variable of the group but is common for every market where the focal group is present, we multiply the importance that market has for the focal group by the Herfindahl Index of the focal market – Herfindahl market. The measure of market importance for each group has been calculated as the percentage of the Total Revenue of the group that comes from that market. The bigger the percentage of the total revenue of the focal group that comes from a certain market, the more the importance of that market for the focal group.

We also control for the market penetration of mobile telecommunications since a higher penetration could lead to better results due to higher demand. Following the definition of GSMA, market penetration is calculated as total connections at the end of the period, expressed as a percentage share of the total market population. As in the previous variable, we multiply the penetration rate of mobile telecommunications in the market by the importance of that market for the focal group – Penetration market.

We include the population of the market in our regression since a market with a larger population could lead to better results due to the bigger demand in the market. In the same way as before, we multiply the importance of the market for the focal group by the population of that market – Population market.

For the last of our market characteristics, we include GDP per capita because countries with greater wealth may spend more on mobile telecommunications (Gruber and Verboven, 2001) and, therefore, the results of the group in these countries could be higher. As in the previous variable, we multiply GDP per capita in the market by its importance for the focal group – GDP pc market. Finally, we include yearly and quarterly dummy variables in order to control for year and seasonal effects.

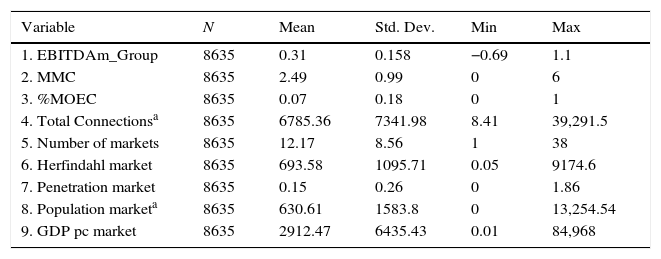

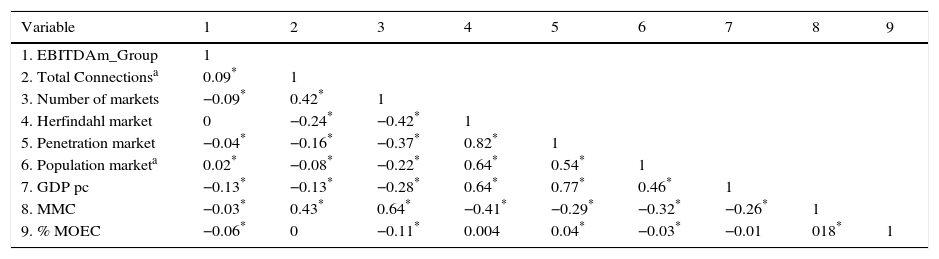

Data analysisTables 1 and 2 summarize the descriptive statistics and correlations, respectively, for the variables included in our analysis. As can be seen, the values of our dependent variable mainly range from −1 to 1 and our MMC variable from 0 to 6. Therefore, international groups that have the biggest number of MMC with their multimarket rivals, CableandWireless and America Movil, only compete with them in six countries at the same time.

Descriptive statistics.

| Variable | N | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| 1. EBITDAm_Group | 8635 | 0.31 | 0.158 | −0.69 | 1.1 |

| 2. MMC | 8635 | 2.49 | 0.99 | 0 | 6 |

| 3. %MOEC | 8635 | 0.07 | 0.18 | 0 | 1 |

| 4. Total Connectionsa | 8635 | 6785.36 | 7341.98 | 8.41 | 39,291.5 |

| 5. Number of markets | 8635 | 12.17 | 8.56 | 1 | 38 |

| 6. Herfindahl market | 8635 | 693.58 | 1095.71 | 0.05 | 9174.6 |

| 7. Penetration market | 8635 | 0.15 | 0.26 | 0 | 1.86 |

| 8. Population marketa | 8635 | 630.61 | 1583.8 | 0 | 13,254.54 |

| 9. GDP pc market | 8635 | 2912.47 | 6435.43 | 0.01 | 84,968 |

Correlations.

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 1. EBITDAm_Group | 1 | ||||||||

| 2. Total Connectionsa | 0.09* | 1 | |||||||

| 3. Number of markets | −0.09* | 0.42* | 1 | ||||||

| 4. Herfindahl market | 0 | −0.24* | −0.42* | 1 | |||||

| 5. Penetration market | −0.04* | −0.16* | −0.37* | 0.82* | 1 | ||||

| 6. Population marketa | 0.02* | −0.08* | −0.22* | 0.64* | 0.54* | 1 | |||

| 7. GDP pc | −0.13* | −0.13* | −0.28* | 0.64* | 0.77* | 0.46* | 1 | ||

| 8. MMC | −0.03* | 0.43* | 0.64* | −0.41* | −0.29* | −0.32* | −0.26* | 1 | |

| 9. % MOEC | −0.06* | 0 | −0.11* | 0.004 | 0.04* | −0.03* | −0.01 | 018* | 1 |

Regarding the correlations, MMC is negatively correlated with the dependent variable, indicating that firms that simultaneously compete with their rivals in different markets achieve worse results than those that only compete with them in one market. Moreover, the negative correlation between %MOEC and the EBITDA margin indicates that, when multimarket contact takes place in emerging countries, the negative effect of MMC on performance is even worse.

MethodWe perform a number of tests to select the specification of our model. First, the Breusch-Pagan Lagrange Multiplier test rejects the null hypothesis that the variance of the firm-level component of the error term is zero (χ2=27,672.46; p<0.01). Therefore, there is firm-level unobserved heterogeneity in our sample. Using panel data techniques is recommended in this scenario. Firm-level unobserved heterogeneity can be modeled as a random effect or as a fixed effect. We use the Hausman test to select the appropriate specification in this case. The test generates a negative result (χ2=−47.96), which must be interpreted as strong evidence that the null hypothesis cannot be rejected and, therefore, firm-level unobserved heterogeneity must be modeled as a random effect. Consequently, we estimate a random effects model controlling for firm and year effects.

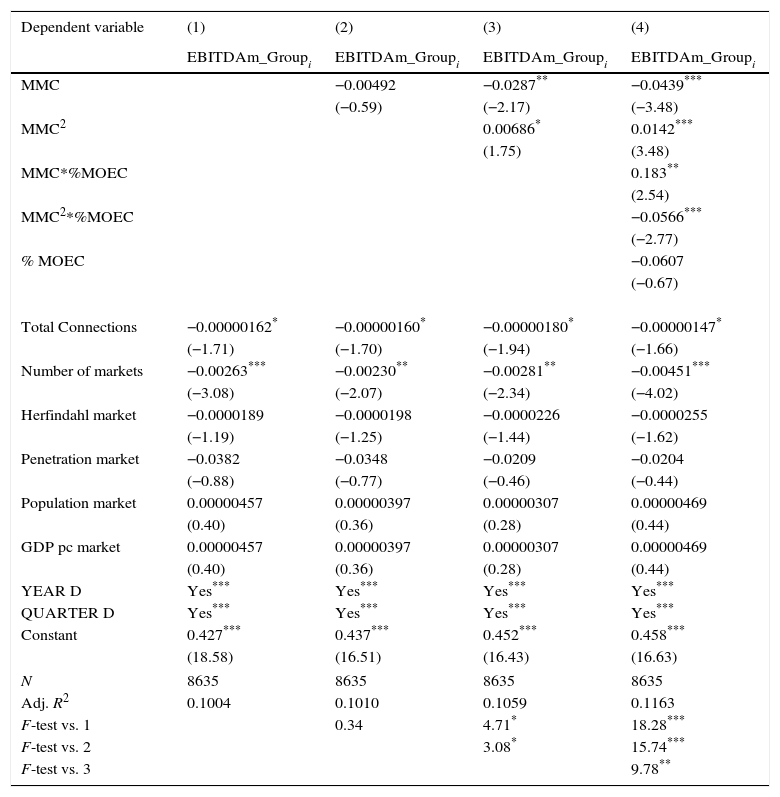

ResultsTable 3 shows the results of our estimations. Column 1 shows the baseline model that only considers the control variables. The model is globally significant, which confirms the importance of our control variables. Hypothesis 1 states that MMC has a U-shaped effect on firm performance. Column 2 includes the variable MMC and column 3 adds its squared effect. The parameter of the direct effect of MMC in column 2 is not significant; however, in column 3, the parameter of the direct effect of MMC is negative (β=−0.0287; p<0.05) and the parameter of the squared effect is positive (β=0.00686; p<0.10). This suggests the predicted U-shaped effect but, for this curvilinear effect to be meaningful in our estimations, the inflection point has to belong to the range of values of MMC observed in our sample. The inflection point corresponds to the value 2.092 of the variable, which falls within the range of our sample.

The influence of MMC on performance and the moderation effect of %MOEC on that relationship.

| Dependent variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| EBITDAm_Groupi | EBITDAm_Groupi | EBITDAm_Groupi | EBITDAm_Groupi | |

| MMC | −0.00492 | −0.0287** | −0.0439*** | |

| (−0.59) | (−2.17) | (−3.48) | ||

| MMC2 | 0.00686* | 0.0142*** | ||

| (1.75) | (3.48) | |||

| MMC*%MOEC | 0.183** | |||

| (2.54) | ||||

| MMC2*%MOEC | −0.0566*** | |||

| (−2.77) | ||||

| % MOEC | −0.0607 | |||

| (−0.67) | ||||

| Total Connections | −0.00000162* | −0.00000160* | −0.00000180* | −0.00000147* |

| (−1.71) | (−1.70) | (−1.94) | (−1.66) | |

| Number of markets | −0.00263*** | −0.00230** | −0.00281** | −0.00451*** |

| (−3.08) | (−2.07) | (−2.34) | (−4.02) | |

| Herfindahl market | −0.0000189 | −0.0000198 | −0.0000226 | −0.0000255 |

| (−1.19) | (−1.25) | (−1.44) | (−1.62) | |

| Penetration market | −0.0382 | −0.0348 | −0.0209 | −0.0204 |

| (−0.88) | (−0.77) | (−0.46) | (−0.44) | |

| Population market | 0.00000457 | 0.00000397 | 0.00000307 | 0.00000469 |

| (0.40) | (0.36) | (0.28) | (0.44) | |

| GDP pc market | 0.00000457 | 0.00000397 | 0.00000307 | 0.00000469 |

| (0.40) | (0.36) | (0.28) | (0.44) | |

| YEAR D | Yes*** | Yes*** | Yes*** | Yes*** |

| QUARTER D | Yes*** | Yes*** | Yes*** | Yes*** |

| Constant | 0.427*** | 0.437*** | 0.452*** | 0.458*** |

| (18.58) | (16.51) | (16.43) | (16.63) | |

| N | 8635 | 8635 | 8635 | 8635 |

| Adj. R2 | 0.1004 | 0.1010 | 0.1059 | 0.1163 |

| F-test vs. 1 | 0.34 | 4.71* | 18.28*** | |

| F-test vs. 2 | 3.08* | 15.74*** | ||

| F-test vs. 3 | 9.78** | |||

Standard errors in parentheses.

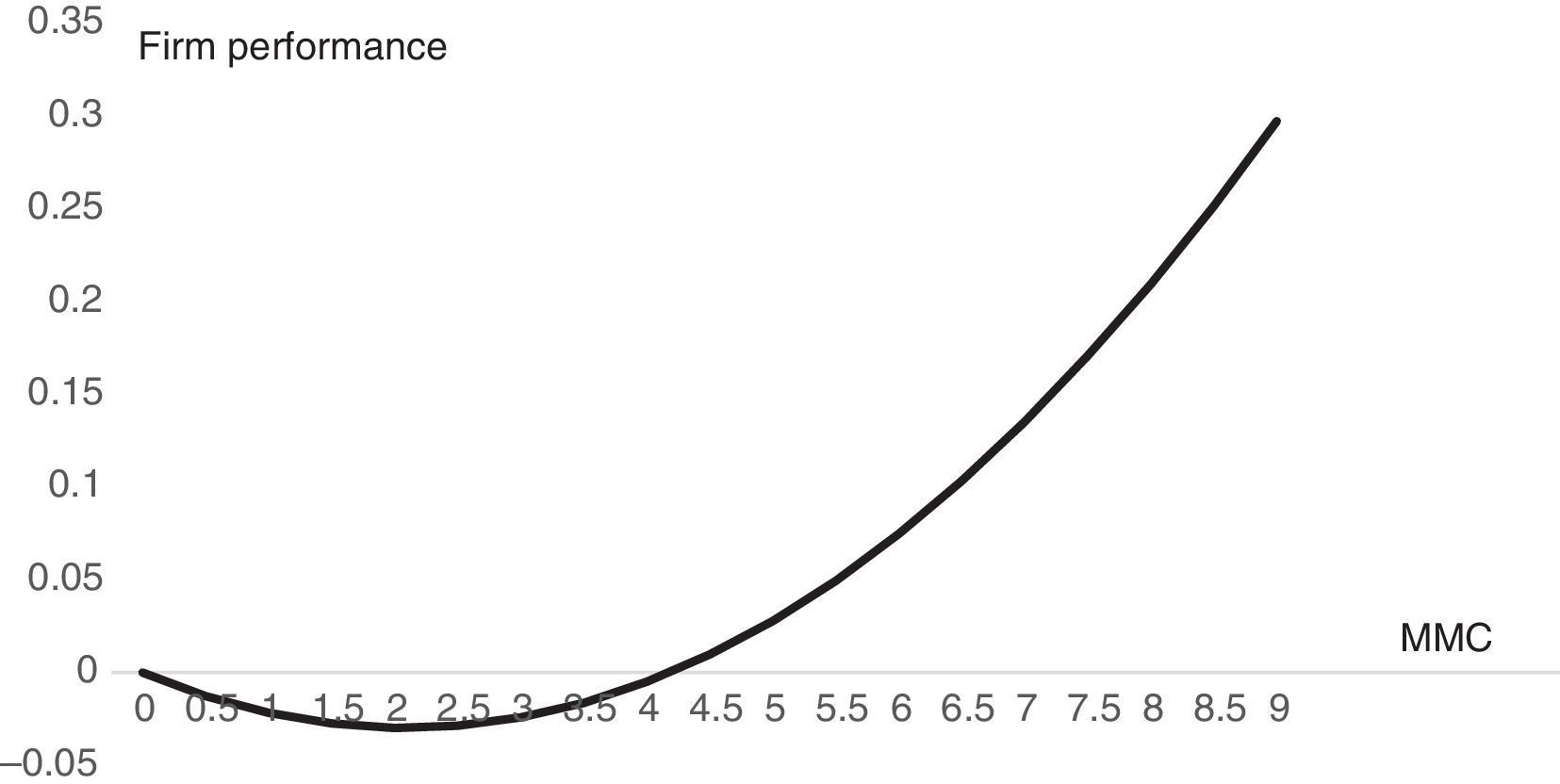

Therefore, Hypothesis 1 is supported by our estimations. To better illustrate our results, Graph 1 depicts the effect of multimarket contact within the range of values of our sample. As the graph shows, the influence of MMC on firm performance is negative up to a certain threshold and, then, it becomes positive as MMC increases. As a consequence, we can conclude that MNEs that compete through medium levels of MMC perform worse than MNEs whose degree of MMC is low or high.

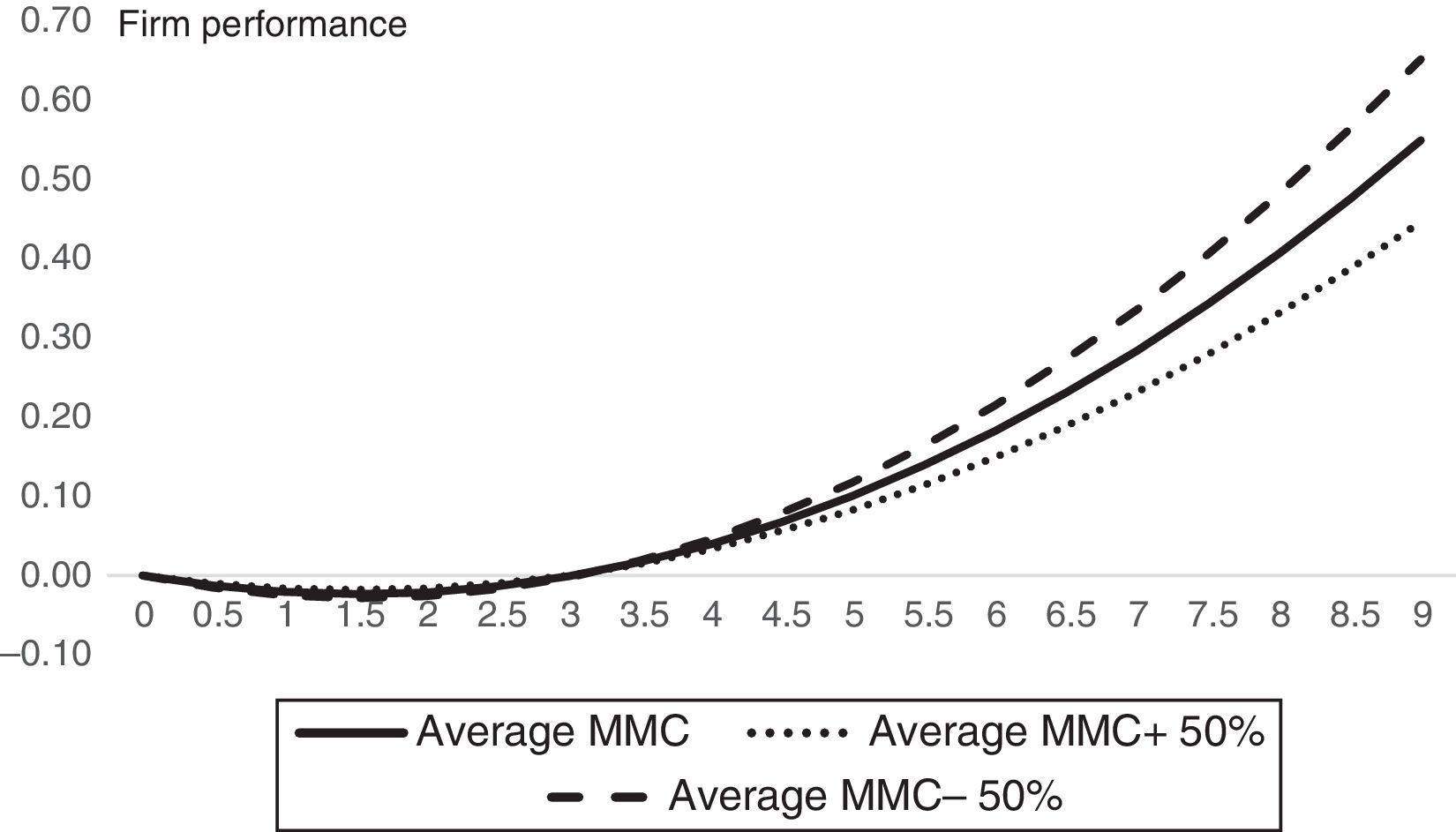

Hypothesis 2 states that the positive effect of MMC on firm performance is less intense when market overlap among MNEs takes place in emerging contexts. Column 4 includes the interaction term of MMC with the percentage of market overlap in emerging countries. The F-tests at the bottom of the table confirm that the full model – column 4 – is preferred to its simpler counterparts. The parameter of the interaction term between the percentage of market overlap in emerging countries and the direct effect of MMC is positive (β=0.183; p<0.05), while the parameter of the interaction term between the percentage of market overlap in emerging countries and the squared effect of MMC is negative (β=−0.0566; p<0.01). The combination of these two effects has an ambiguous interpretation. To understand it better, Graph 2 depicts the effect of MMC on firm performance for different values of the variable percentage of market overlap in emerging countries.

The solid line shows the effect of MMC on firm performance when MNEs have an average market overlap with their multimarket rivals in emerging countries. The dotted line shows the influence of MMC on firm performance when the percentage of market overlap in emerging countries is 50% above the average value of the variable and the dashed line represents this influence when the percentage of market overlap in emerging countries is 50% below the average value of the variable. As Graph 2 shows, the positive effect of MMC on firm performance decreases as the percentage of market overlap in emerging countries increases. These results support our second hypothesis, confirming that the presence of MNEs in emerging economies hinders the development of mutual forbearance agreements and, therefore, reduces the positive effect of MMC on firm performance.

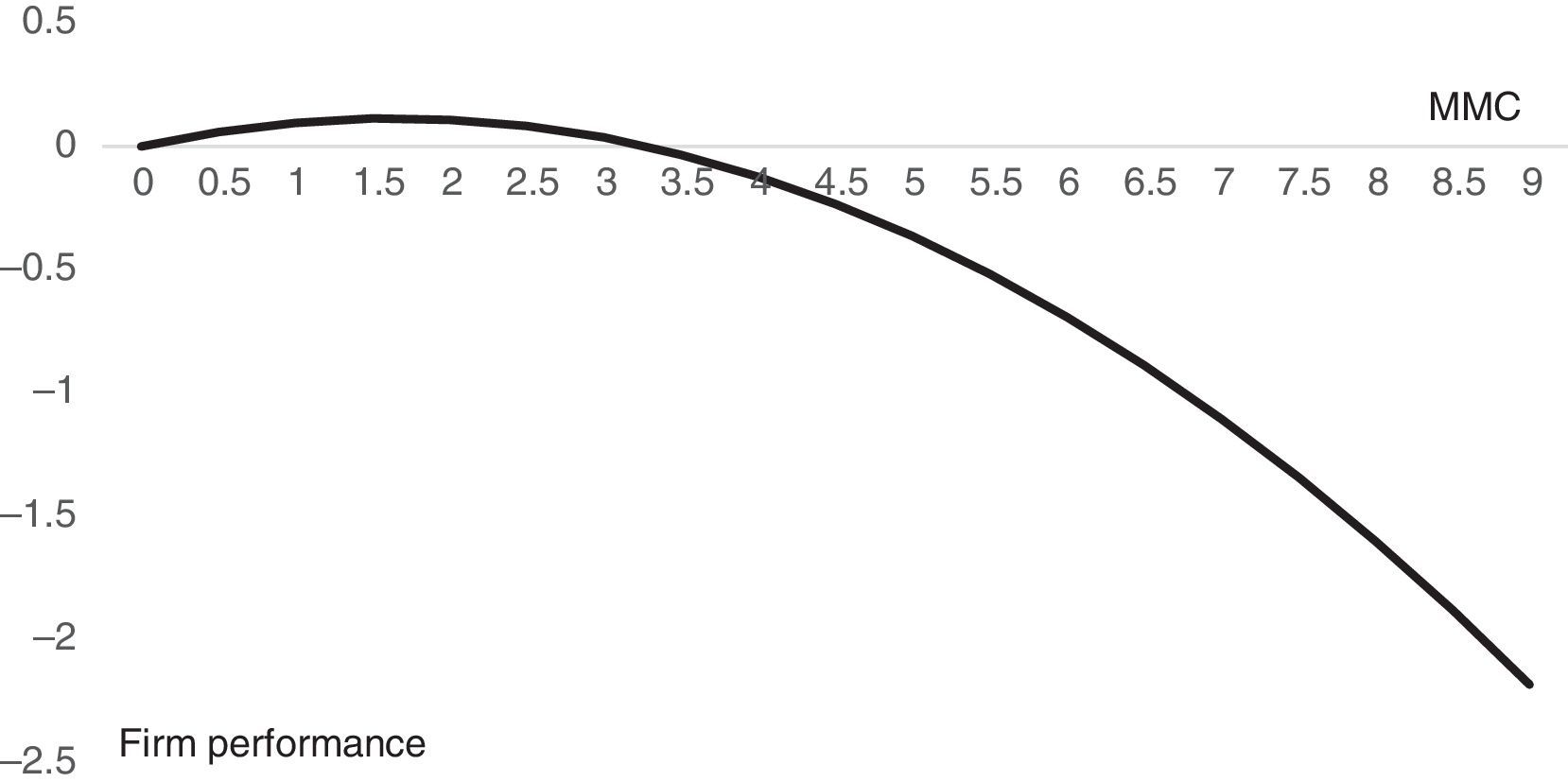

Finally, to understand our results better, we depict the effect of MMC on firm performance for situations in which MNEs only compete against their multimarket rivals in emerging countries. As Graph 3 shows, the effect of MMC on firm performance is mainly negative when MMC among MNEs only takes place in emerging countries. This could mean that mutual forbearance dynamics are not present when MNEs only compete with their multimarket rivals in emerging countries. The difficulties involved in observing and interpreting the behavior of rivals, as well as the problems of coordinating their subunits in emerging contexts, may prevent completely the development of collusive agreements. We devote further attention to this finding in the following section.

Discussion and conclusions

Nowadays, MNEs are present in many countries. As a consequence, they tend to compete against their rivals simultaneously in different markets. This research explores MMC dynamics among MNEs and shows that MMC has a U-shaped effect on firm performance. This finding contributes to the reaching of a consensus in MMC literature by confirming the curvilinear relationship between MMC and performance in an international context (Baum and Korn, 1999; Fuentelsaz and Gómez, 2006; Haveman and Nonnemaker, 2000). Our results show that, when MMC is low, rivalry between MNEs is intense. However, when MMC is high, MNEs prefer to tolerate each other and, thus, rivalry between them decreases, with a consequent improvement in firm results. Therefore, MNEs that compete through moderate levels of MMC perform worse than MNEs whose MMC is high or low.

In addition, we show that the positive effect of MMC on firm performance, that is the positive slope of the U-shaped effect, is less intense as the percentage of market overlap with multimarket rivals in emerging countries increases. This finding is consistent with our theoretical framework that suggests that collusive agreements among MNEs are difficult to establish in emerging contexts. Apparently, the two basic conditions of mutual forbearance among multimarket firms, namely, full observability and efficient internal coordination, are not present in emerging countries. With respect to full observability, it seems that information asymmetries and environmental uncertainty that characterize emerging economies (Tong et al., 2008; Meyer et al., 2009) make the behavior of multimarket rivals less observable and interpretable. Concerning the internal coordination of subunits, our results suggest that the need for local adaptation and agreements with local partners in emerging economies (Guillén and Garcia-Canal, 2009; Johanson and Vahlne, 2009; Hoskisson et al., 2000) hinders the coordination of subsidiaries and obstructs the implementation of common guides from headquarters.

By exploring MMC dynamics in emerging contexts, our contribution to previous literature is twofold. First, our findings help to advance MMC literature by analyzing the extent to which the macroeconomic environment moderates the mutual forbearance hypothesis (Yu and Canella, 2013). As mentioned, prior research has mainly focused on exploring how industry and firms characteristics moderate the effect of MMC on firm performance (Gimeno, 1999; Haveman and Nonnemaker, 2000; Fuentelsaz and Gómez, 2006). Second, since prior MMC studies have tended to focus on advanced economies, our research is one of the first to explore whether the relationship between MMC and performance is the same for subsidiaries in emerging countries. In this regard, we also shed light on the debate about how the macroeconomic features of emerging markets can change the findings of traditional managerial theories (Hoskisson et al., 2000). Our results show that mutual forbearance cannot be sustained in emerging countries, which reduces the applicability of MMC theory in this kind of contexts.

Our research has several limitations that may constitute avenues for future research. First, this research studies the moderating effect of the macroeconomic context in the relationship between MMC and performance. We explore the way in which market overlap in emerging countries, which are characterized by governmental discretion, political instability and poor property rights protection (Meyer et al., 2009), affects mutual forbearance practices and, therefore, the impact of MMC on performance. To further explore how the macroeconomic context conditions MMC dynamics among MNEs, future research should separately analyze the moderating effect of different institutional factors. For instance, future research could study how governmental discretion has an impact on mutual forbearance among multimarket rivals or the effect of property rights protection on MMC dynamics.

Second, using international mobile telecommunications data may affect our results in different ways. For example, we had to remove some significant emerging markets, such as Brazil, from our sample because they assign licenses with regional, not national, coverage. Therefore, although two international groups were present in one of the markets removed may not compete directly. Additionally, results may be affected by the international strategy that the firms follow. In the telecommunications industry, MNEs usually follow a multidomestic (country-by-country) strategy, which makes them more dependent on local resources and increases the pressures they face to gain legitimacy locally (Ghoshal and Westney, 1993; Rosenzweig and Singh, 1991). It can make mutual forbearance especially difficult, as we proposed in Hypothesis 2. It would be interesting to extend this study to other industries in which MNEs follow a global strategy to observe whether results change as a consequence of the international strategy followed by MNEs.

With respect to managerial implications, managers of MNEs have to deal with the complexity of supervising subsidiaries located in both developed and emerging countries. They are in charge of managing the consequences of competing against the same rivals simultaneously in different markets, that is, they have to handle MMC with other MNEs. Our findings are of utmost importance for managers in this regard. As Graph 3 shows, the effect of MMC on performance is mainly negative when market overlap with multimarket rivals only takes place in emerging countries. This shows that reaching collusive agreements in emerging countries is not possible and implies that MNEs that operate exclusively in these countries cannot take advantage of MMC dynamics. Therefore, managers interested in developing MMC strategies to benefit from mutual forbearance with rivals should direct the growth of their firms toward developed countries.

We acknowledge financial support from the Spanish Ministry of Economy and Competitiveness and FEDER (projects ECO2011-22947 and ECO2014-53904-R). We thank Xosé H. Vázquez, two anonymous referees, Jaime Gomez and Juan P. Maicas for their comments and suggestions.

These authors contributed equally to this paper.

Notice that our second hypothesis exclusively theorizes about the positive effect of MMC on firm performance. Consequently, our contention only affects the positive slope of the U-shaped effect proposed in Hypothesis 1.

International mobile groups are holdings with economic interests in at least two different mobile national operators (MNO). Therefore, international groups are entities that operate through their participation in MNOs capital.

Countries that are considered as emerging are: Argentina, Bulgaria, Chile, Colombia, Estonia, Hungary, Latvia, Lithuania, Malaysia, Pakistan, Peru, Poland, Romania, South Africa, Turkey and Ukraine. Other emerging countries such as Brazil, India and Russia are not included in our sample since the licenses in these countries are not given for all the country but only for some regions within it.

In this study, we consider that an international group is present in a market when it has a participation of at least 30% in the capital of any mobile operator that is present in that market. Our premise is that below this threshold the group may not have a sufficient influence over the operator to modify its competitive behavior and, therefore, reach the forbearance result.

Vodafone also competes with other groups, such as Digicel, Etisalat and Millicom but only in one market so those pairs of groups (Vodafone-X) are not included in the measure of its market overlap.

According to GSMA Intelligence, Total Connections are defined as total unique SIM cards (or phone numbers, where SIM cards are not used), including cellular M2M that have been registered on the mobile network at the end of the period.

articles