Pension funds, when they acquire common shares of companies in the capital markets, start to participate more actively in the decision-making of boards of directors and, through their representatives, in the monitoring of managers. The aim of this study is to determine whether pension funds are good monitors. This is done by identifying the influence of the control structure of pension funds over the financial performance and the market value of Brazilian public companies. Using dynamical models of linear and non-linear regressions estimated by GMM-Sys in an unbalanced panel from 1995 to 2015, it is shown that pension funds do not play a good monitoring role, as the control structure of these funds is negatively related to the financial performance of a company or, in other words, the higher the stake, the worse the performance of the company. A possible reason for this is that pension funds invest in the capital markets for portfolio diversification, are not concerned with specific decision-making in companies and have few monitoring skills, thus generating conflicts that go against the objective of maximizing the value of the company. Also, the study identifies the fact that investors give a higher value to the shares of firms in which domestic public funds have investments, even without proof that such funds improve the profitability of companies.

Os fundos de pensão, ao adquirirem ações ordinárias de empresas no mercado de capitais, começam a participar mais ativamente nas tomadas de decisão dos conselhos de administração e no monitoramento dos gestores através de seus representantes. Devido a essa questão, o presente estudo buscou verificar se os fundos de pensão são bons monitores através da identificação da influência da estrutura de controle destes no desempenho financeiro e no valor de mercado das empresas de capital aberto brasileiras. Utilizando modelos dinâmicos de regressões lineares e não lineares múltiplas, estimadas pelo GMM-Sys, em um painel não balanceado de 1995 a 2015, foi evidenciado que os fundos de pensão não desempenham um bom papel de monitoramento, já que a estrutura de controle destes fundos possui uma relação inversa com o resultado financeiro tanto interno quanto de mercado, ou seja, quanto maior a participação acionária, menor é o desempenho das empresas. Esse resultado foi encontrado, possivelmente, pois os fundos de pensão investem no mercado de capitais para diversificação de portfólio, não estando preocupados com tomadas de decisão específicas nas empresas, gerando, assim, falta de habilidades de monitoramento adequadas, provocando conflitos que vão contra o objetivo de maximização de valor das empresas. Também, foi identificado que os investidores valorizam as ações de firmas investidas por fundos públicos domésticos, mesmo sem comprovação que tais fundos melhoram a rentabilidade das empresas.

When institutional investors acquire shares in companies in the capital markets, they begin to participate more actively in the decision-making of the boards of directors, through their representatives. Institutional investors, such as mutual funds, investment clubs, external funds, insurance companies and pension funds, are legal entities that invest in the stock market (McCahery, Sautner, & Starks, 2016). Corporate governance turns out to be an important way for these investors to achieve the return they desire, and many institutions are willing to engage in shareholder activism, so much so that Aggarwal, Saffi, and Sturgess (2015) have identified that the proxy voting process promoted by these institutional investors is an important channel for governance.

Pension funds are large institutional investors in the capital markets. The greater the shareholding participation of these funds, the more they are concerned about monitoring the managers of the companies in which they hold shares (Punsuvo, Barros, & Kayo, 2007). Pension funds have a significant market share in the overall portfolio (Blake, Rossi, Timmermann, Tonks, & Wermers, 2013). Specifically, the importance of pension funds in Brazil in recent times has been largely because of their accumulated large resources, which total around R$ 250 billion. This significant amount has aroused a great deal of interest in several decision-making arenas, especially those dealing with public policy, the financial markets and the capital markets (Gomes & Cresto, 2010; Varga & Wengert, 2011).

Actively managed funds control a large share of company's equity and play a crucial role in determining share prices (Chen, Hong, Jiang, & Kubik, 2013). Lazzarini (2007) reaffirms this importance, arguing that, in spite of the great ownership restructuring that has occurred in recent decades and has facilitated privatizations and the inflow of foreign capital, in Brazil this situation have further reinforced the position of local owners, especially the State and federal pension funds in the capital markets. Harris, Jenkinson, and Kaplan (2014) argue that there has also been a large increase in the number and size of private equity funds.

The fact that pension funds acquire the common shares of publicly traded companies enables them to participate more actively, through their representatives, in the activities of the board of directors, because they have an interest in the development of the company and in increasing the value of their shares. As the directors are the most significant and active monitors used by companies to avoid any problems with the expropriation of minority shareholders, pension funds, once they have board representatives, also end up playing this role (Hartzell & Starks, 2003).

Effective monitoring by large stakeholder groups, represented by administrative advisors, is an important mechanism of corporate governance in publicly traded companies (Dasgupta & Piacentino, 2015). However, the importance of pension funds has grown over time, and their influence in monitoring corporate behaviour is still poorly understood in Brazil. The following question persists: ⬓What is the influence of the control structure of pension funds on the financial performance and market value of publicly traded Brazilian companies?⬽

On the basis of these assumptions, the objective of this study is to identify whether pension funds are good monitors, and to do this by analysing the influence of their control structure on the financial performance and market value of publicly traded Brazilian companies. First, the other components of the article are presented, starting with a review of the concepts related to control structure and pension funds. This is followed by the methodological aspects and the results achieved, and finally, the conclusions and the contributions of the study are identified.

Control structure of pension funds: concepts and hypothesesThe construction of the corporate governance system in a company requires the various contractual relations existing in the entity to be balanced against the relationship between the owner and the manager; a failure to observe these tensions can have an impact on the development and implementation of the mechanisms of control (Christopher, 2010). Pension funds, by acquiring part of the control of the company, become part of these relationships, which may have an impact on the performance of the company. In this context, this section is subdivided into two parts: (i) corporate governance, ownership structure and control structure; and (ii) pension funds as a monitoring mechanism.

Corporate governance, ownership structure and control structureDiscussions about ownership structure began with the work of Berle and Means (1932), who showed that the distribution of capital is one of the main mechanisms of governance. For Punsuvo, Barros, and Kayo (2007), corporate governance is a way of reducing the conflicts of interest generated by the separation of ownership and control, and, for Jensen and Meckling (1976), it is a set of internal and external mechanisms of incentive and control that aim to minimize the costs arising from the agency problem. For Shleifer and Vishny (1986), corporate governance is a way of ensuring return on investment, reducing the inefficiency of resource allocation, and encouraging investors to increase their stakes in the company, through transparency in audited financial reporting and through the collegiate functioning of control and accountability (Brennan & Soloman, 2008).

The legal regime in a country is important if one is to understand the conflicts of interests existing in its companies. To clarify this question, La Porta, Lopez-De-Silanes, Shleifer, and Vishny (1998) classified four different types of laws regarding the legal protection of shareholders that significantly influence the ownership and control structure. Countries with a common law regime (such as the United States and the United Kingdom) have more protection for minority shareholders, leading to fewer expropriations, while countries with French-style (such as Brazil, Belgium and France), German-style (such as Japan, Germany and Austria) and Scandinavian-style (such as Denmark, Finland and Switzerland) civil law have less protection for shareholders, facilitating the expropriation of minority shareholders. As a result, these latter countries end up having smaller and less developed capital markets (La Porta, Lopez-De-Silanes, Shleifer, & Vishny, 1997).

When there is strong legal protection for minority shareholders, the main problems stem from agency conflict, making companies with concentrated structures more efficient because the need for monitoring is reduced (Jensen & Meckling, 1976). However, in countries where there is weak legal protection, the nature of the conflict changes to the possibility of the expropriation of minority shareholders by majority shareholders (Shleifer & Vishny, 1997). Silveira (2004) argued that, in the Brazilian context, the second type of conflict is more pronounced, and that shareholders who hold most of the control tend to use their capital and power to favour their own interests against what the minority shareholders expect. This issue is evident in the work of Sonza and Kloekner (2014), which indicated that a high concentration of property may undermine the performance of Brazilian companies because of this expropriation.

La Porta et al. (1997, 1998) have argued that, in the absence of adequate protection for minorities, investors seek to protect their investments by exercising direct control through large blocks of stock. Following this idea, Becht and Mayer (2001) reported that more than 50% of European companies have a single shareholder block that commands the majority of shares. In contrast, in the United Kingdom and the United States fewer than 3% of companies have these blocks. Concentrated ownership is, therefore, a response to the protection of inefficient investors.

Pension funds as a monitoring mechanismThe monitoring of companies is done by several external agents, such as advisers, auditors, large shareholders, creditors, investment banks, rating agencies and institutional investors (Tirole, 2006). The directors, in principle, monitor the management of the company on behalf of the shareholders. Their duties are to define or approve the company's major decisions and corporate strategy: asset disposals, investments and acquisitions, public offerings made by acquirers, changes in executive compensation, supervision of risk management and auditing, among others (Tirole, 2006).

Tirole (2006) gives an understanding of the monitoring function by dividing it into active monitoring (interfering in management in order to increase shareholder value) and speculative monitoring (which is retrospective and is not aimed at increasing company value). In the case of speculative monitoring, Chen, Harford, and Lin (2015) have identified that financial analysts play an important role in governance in overseeing executives⬢ behaviour. The market rates an expected increase in conflicts after the loss of analysts⬢ coverage. For active monitoring, Cornelli, Kominek, and Ljungqvist (2013) have verified that the board of directors are active monitoring agents, generating an improvement in the performance of the firm.

As pension funds take control of companies, they begin to participate more actively in the decisions of the board of directors, through their representatives. As directors have, as one of their main functions, the supervision of activities, pension funds can also act as monitors. This activity is aimed at resolving existing conflicts, including the expropriation of minority shareholders, a very common problem in Brazilian companies, whose main characteristic is the concentration of control as a result of the legal regime in the country (Hartzell & Starks, 2003).

Emphasizing this issue related to expropriation, Iliev, Lins, Miller, and Roth (2015), by analysing the votes of institutional investors (including pension funds) in director elections in 42 countries, have identified that, in places with weak legal protection and poor disclosure of corporate information, these investors show a propensity to vote against the directors, suggesting a greater exercise of corporate governance through voting. This fact suggests that the participation of these investors in the board may be an important mechanism for governance in Brazil.

Another aspect of corporate governance related to pension funds is identified by Bird and Karolyi (2016), who found that the greater the transparency of corporate information, the greater the investment by these institutions. Aggarwal, Erel, and Starks (2015) have suggested that funds and their representatives take into account the opinion of beneficiaries and shareholders in their decisions, and that proxy votes serve as a public channel for influencing corporate behaviour. In this context, Prado, Saffi, and Sturgess (2016) indicated that an increase in the control exercised by pension funds limits the arbitrage in the capital markets.

Pension plan assets in Brazil grew significantly after their regulation through Law no. 6,435 of 1977, which was repealed only in 2001 by Complementary Law no. 109 regulating the performance of pension funds. Three years later, in 2004, Law no. 11,053, dated 29 December 2004, was introduced. This came into effect in January 2005, making pension funds tax-free for stock acquisitions (Article 5), even though the remaining shareholders would continue to be taxed at 15% (Article 3). Recently, Complementary Law no. 109 of 2001 was amended by Complementary Law 388 of 2015, which aimed to improve the governance arrangements of private pension entities linked to the Union, the States, the Federal District and the Municipalities, the foundations, joint-stock companies and other public entities.

From the statistics of the Organization for Economic Cooperation and Development (OECD, 2016), it can be seen that pension fund assets increased by 910.49% between 1995 and 2016, from R$ 74.8 million to R$ 756 million. Pension funds can be considered to be the main institutional investors of the country, playing an important role in the accumulation of long-term domestic savings. The relationship between pension fund net worth and Gross Domestic Product (GDP) increased from 3.3% in 1990 to 12.7% in 2016. For ABRAPP ⬜ Brazilian Association of Closed Pension Entities (2016), this relationship shows the importance of the pension system, but the proportion can still be considered relatively small when Brazil is compared to other countries (Netherlands 161.1%, Iceland 146.3%, Switzerland 125.6%, Australia 113.1%, United Kingdom 96.0% and USA 84.6%).

For this reason, there is a growing discussion about the role that pension funds can play in the Brazilian economy. It can contribute, in Rabelo's (1998) view, in three fundamental areas: (i) the financing of national economic development; (ii) the expansion of domestic capital markets; and (iii) the democratization of corporate capital (dissipation of ownership and control). On the other hand, the growth of funds has the potential to transform these structures and fundamentally affect the depth of domestic capital markets.

Because they are highly significant, pension funds are the focus of institutional monitoring studies, and many scholars have indicated that there is a positive relationship between ownership concentration and corporate performance. Along these lines, Aggarwal, Erel, Ferreira, and Matos (2011) verified, in an analysis covering 23 countries, that an increase in institutional property influenced the improvement of governance. Crane, Michenaud, and Weston (2016) corroborate this, stating that firms in which institutional investors have greater control pay more dividends, generating greater shareholder benefit. Del Guercio and Hawkins (1999) also found that pension funds are successful in controlling and driving changes that take the target companies into account. However, Edmans (2009) cautioned that the effectiveness of activism depends on the threat of selling stocks and leaving the company, which is greater for investors with larger fractions of ownership.

In the same vein, Ferreira and Matos (2008), in a study of the role of institutional investors (including pension funds) in 27 countries, identified that the monitoring and activism of these investors is very effective, improving the performance of firms. Companies that were owned by larger foreign and independent institutions had greater market valuation, better operating performance and lower capital expenditures. According to these authors, these companies had more active monitoring, both direct monitoring (direct intervention by institutions) and indirect monitoring (the effect of institutions in the market's assessment). Based on these assumptions, the following hypothesis is formulated:H1 The greater the concentration of control of pension funds, the greater the financial performance and the market value of Brazilian companies.

However, the activism of pension funds does not always bring good results for the company, mainly for the following reasons, which were pointed out by Becht, Franks, Mayer, and Rossi (2009): (i) pension funds, which generally own small fractions of companies and have less voting power than other investors, do not provide enough resources for activism by shareholders, generating inadequate monitoring; (ii) the largest US institutional investors have conflicts of interest, mainly because pension funds are commonly sources of disputes between trade unions and companies; and (iii) the US regulatory system limits shareholder control rules, and there are great legal obstacles for nominating and electing directors, especially for smaller shareholders.

The issue of the expropriation of minority shareholders may be exacerbated by the increased participation of these funds in the ownership of companies. Along these lines, Giannetti and Laeven (2009) found that when a public pension fund acquires a stake in a company in the capital markets, the value of a marginal vote increases, and controlling shareholders further strengthen their control blocks. Using this increased strength, these shareholders try to exploit their position or persuade pension funds to follow their decisions in order to increase their voting power, creating a negative bias for the company.

Since pension funds do not have great skills in strategic decision-making on the board, they tend to hire specialized consultancy firms, but their effective role is quite controversial. Malenko and Shen (2016) have identified that the influence of these consultancy firms on the vote decisions of these funds on the board meetings is quite high, both for companies that have a concentrated control structure and those that have a dispersed structure. In analysing whether funds are active voters, Iliev and Lowry (2015) identified that they are more prone to follow the recommendations of a specialized consultancy company when they vote in a board meeting. The few funds that are most engaged in the voting process and do not use consultancy services have a more significant return on this activity, generating greater shareholder value.

According to Smith (1996), only a minority of studies have found evidence that institutional owners (including pension funds) increase shareholder value through company monitoring. Wahal (1996) and Gillan and Starks (2000) reported that institutional owners are largely ineffective as monitors. Carleton, Nelson, and Weisbach (1998) and Woidtke (2002) have stated that there is a deterioration in company performance because such firms do not have adequate monitoring skills, leading to conflicts that go against a firm's goal of maximizing value. In this same vein, Harris et al. (2014) concluded that the performance of companies is negatively related to share ownership by pension funds. From the issues raised here, the following alternative hypothesis is formulated:H1A The greater the concentration of control of pension funds, the lower the financial performance and market value of Brazilian companies.

In order to verify the influence of the control structure of pension funds on the financial performance and market value of publicly traded Brazilian companies, a quantitative and exploratory⬜descriptive study is applied, with secondary data related to the control structure, balance sheet and income statement extracted from ECONOMATICA data base. The data referring to the different levels of governance are collected from the website and through direct contact with the Memory Center of the São Paulo Securities, Commodities and Futures Exchange (BM&FBovespa, 2016), and cover publicly traded Brazilian companies for which some common shares belong to pension funds (since these are stocks that give voting rights, which may influence the decisions and performance of the company). The data are collected on an annual basis, between 1995 and 2015 (21 years), and relate to 252 companies, giving 5002 observations.

In the analysis of the data, dynamic models of multiple linear and non-linear regressions estimated by GMM-Sys are applied for an unbalanced panel. In the application of panel data, a given sample of individuals is considered over time, allowing for multiple observations for each individual in the sample. For Bond (2002), a dynamic model (where the dependent variable lagged in a period is also considered as an explanatory variable in the model) should be considered to avoid possible distortions in the analysis, if the regressions present serial correlations of the first order, as is the case in this study.

The Generalized Moment Method (GMM) offers a more efficient structure for obtaining asymptotic estimators than other methods. In this case, there are two types of estimators that can be used: GMM-Dif (in differences), developed by Arellano and Bond (1991), and GMM-Sys (systemic), developed by Blundell and Bond (1998). The difference lies in the moment conditions of each estimator, which depends on the number of instruments available in the analysis. GMM-Sys is chosen for this study because this model accepts a set of available instruments and allows more precise estimates, although the assumptions about the initial conditions are more restrictive.

The regressions are estimated with linear and non-linear variables. In this second case, a possible quadratic relationship (where the main independent variable is squared) between the percentage of control exerted by the fund and the performance or market value of the company is considered. Using the ideas of Almeida, Campello, and Galvão (2010), the same explanatory variables, but now lagged, are used as instruments. Finally, Bond (2002) states that investigating the properties of the time series is highly recommended when GMM estimators are used for dynamic panel models. In this case, the efficiency gains allowed by the homoscedasticity condition are reduced, and one can dispense with the condition, because more robust assumptions are made (Mátyás, 1999).

The tests applied in the study are as follows: (i) Arellano and Bond (1991): to identify whether there is serial correlation in the residuals; (ii) Correlation: to identify the existence of multicollinearity; (iii) Chi-square (¿2): to verify whether there is an association between the variables; and (iv) Hansen (1982): to verify whether there is over-identification of the instruments. Because the presence of outliers in the variables is identified, they are winsorized at 1%. The data are corrected according to the IGP-DI, based on the year 2015, and the software used to run the regressions is STATA-SE. Formula (1), as follows, is applied in the study:

where D represents the performance, α is the intercept, γ and δ are the coefficients, Zit refers to the control structure of pension funds, Wit are control variables, EFind represents the industrial fixed effects, EFtemp represents the temporal fixed effects, ¿it represents the error term, i indicates the company and t indicates the time period. The dependent variables in the model are divided into two categories. The first includes internal profitability indicators: (a) ROA (return on assets); and (b) ROE (return on equity). The studies of Boubakri and Cosset (1998) and Gupta (2005) indicate that these profitability indices capture the financial situation of the company. The second category includes market indicators: (a) Tobin's Q; and (b) market-to-book (MB). The data referring to the final accounting period were considered for the analysis. The descriptions and the formulas for the variables are presented in Table 1.

Description of variables.

| Dependent variables | |||

|---|---|---|---|

| Internal variables | Formula | Market variables | Formula |

| ROA ⬜ return on assets | ROA=operating incometotal assets | Tobin's Qa | Q=(MVE+PS+D)total assets |

| ROE ⬜ return on equity | ROE=net profitequity | MB ⬜ market-to-booka | MB=(MVE+PS+D)equity |

| Independent and Control Variables | |||

|---|---|---|---|

| Variable | Formula/description | Authors | Signal |

| FP ⬜ pension funds | Total percentage of common shares belonging to pension funds that each hold above 5%. | Del Guercio and Hawkins (1999), Aggarwal et al. (2011), Edmans (2009) | + |

| Giannetti and Laeven (2009), Gillan and Starks (2000), Harris et al. (2014) | ↙ | ||

| AP ⬜ principal shareholder TPA ⬜ three largest shareholders; CPA ⬜ five largest shareholders | - Percentage of common shares owned by the company's largest shareholder. - Total percentage of common shares of the company's three largest shareholders. - Total percentage of common shares of the company's five largest shareholders. | Jensen and Meckling (1976) | + |

| Silveira (2004), Sonza and Kloekner (2014), La Porta et al. (1997, 1998) | ↙ | ||

| Tang ⬜ tangibility of the assetsb | Tang=CH+0.715ÔR+0.547ÔI+0.535ÔPPETA | Pöyry and Maury (2010), Almeida and Campello (2007) | ↙ |

| Size: AT ⬜ total assets; PL ⬜ equity; EBITDA. | - Logarithm of the company's total assets; - Logarithm of the company's equity; - Logarithm of profits before interest, taxes, depreciation and amortization. | Pedersen and Thomsen (1997) | + |

| Klapper and Love (2004) | ↙ | ||

| AL ⬜ leverage | AL=Current liabilities+Non-current liabilitiesEquity | Jensen and Warner (1988), Boubakri and Cosset (1998), Brick et al. (2006) | ↙ |

| Law05 ⬜ Law 11,053 of December 29, 2004. | Dummy: 1 ⬜ Period of validity of the law (2005⬜2015); 0 ⬜ Years prior to 2005. | Colombo and Caldeira (2016) | + |

| FE ⬜ foreign pension funds | Dummy: 1 ⬜ If the pension funds that have control structure are foreign; 0 ⬜ OWc | Giannetti et al. (2015) | + |

| FU ⬜ state-owned pension funds | Dummy: 1 ⬜ If the pension funds that have control structure are state-owned; 0 ⬜ OWc | Becht et al. (2009) | ↙ |

| IGC ⬜ Corporate Governance Index | Dummy: 1 ⬜ If the company participates in the Corporate Governance Index; 0 ⬜ OWc | Almeida, Santos, et al. (2010) | + |

| Ferreira (2012), Macedo and Corrar (2012) | ↙ | ||

MVE, stock price of the firm multiplied by the number of outstanding common shares; PS, settlement value of the outstanding preferred shares; D, total debt (current liabilities minus current assets plus inventories and long-term debt) (calculation suggested by Chung and Pruitt (1994)).

CH, cash holdings; R, receivables; I, inventories; PPE, property, plant and equipment; TA, total assets (calculation suggested by Almeida and Campello (2007)).

The main independent variable, which is related to the control structure of pension funds, is formulated as the number of shares belonging to such funds divided by the total number of shares. As only owners of more than 5% of the shares actively participate in the decisions of the board, companies for which pension funds control less than 5% of the shares are excluded from the sample. The assumptions of this variable were explained in ⬓Pension funds as a monitoring mechanism⬽ section with the construction of the hypotheses. Regarding the control variables, the following measures are inserted into the equation; the formulas and compositions of these variables are presented in Table 1:

- (i)

Ownership structure of the main shareholder and the largest three and largest five shareholders. These variables may have an ambiguous effect. According to Jensen and Meckling (1976), the effect of ownership structure on performance is positive because the greater the concentration of ownership, the smaller the possibility of the company having agency problems. In other hand, La Porta, Lopez-De-Silanes, and Shleifer (1999) and Sonza and Kloekner (2014) have stated that when countries have weak legal protection in relation to minority shareholders, as in the case of Brazil, the more concentrated the ownership structure, the greater the possibility of expropriation of minority shareholders, impairing the company performance.

- (ii)

Size (total assets, EBITDA and equity). Pedersen and Thomsen (1997) showed that the larger the company size (as measured by total assets and EBITDA), the more disseminated its control structure, making its efficiency greater too. Klapper and Love (2004) have, by contrast, identified that size can have adverse effects on corporate performance in terms of governance, since both large and small firms have incentives to seek satisfactory results, to avoid agency problems (large companies) or to pursue growth opportunities (small companies).

- (iii)

Leverage. Generally, more profitable companies are less indebted. In this respect, Jensen and Warner (1988) and Boubakri and Cosset (1998) suggest that, for firms seeking a better financial result, there is a tendency to decrease their leverage, because borrowing costs burden the company, generating inefficiencies. Brick, Palia, and Wang (2006) also found a negative relationship between leverage and performance, suggesting that if firms are over-leveraged, there is a propensity to increase their bankruptcy costs, harming future prospects.

- (iv)

Tangibility. This variable is expected to be negatively related to efficiency because, according to Pöyry and Maury (2010), tangibility represents resources that are costly to the company, generating a decrease in its results. Along these same lines, Almeida and Campello (2007) stated that the more fixed assets a firm has, the greater the guarantees it must give to obtain financing, generating more indebtedness. This issue may adversely affect the financial performance of a company, since, as was mentioned in the previous item, leverage and results are inversely related.

- (v)

Law05. This is a dummy referring to Law no. 11,053, dated December 29, 2004, which began to take effect in January 2005. This law meant, according to Colombo and Caldeira (2016), that pension funds became exempt from taxes for the acquisition of shares, although the remaining shareholders continued to be taxed at 15%. This legal change created a natural experiment in the Brazilian capital markets, generating a significant causal effect for pension fund investments in publicly traded companies, which, as a consequence, positively affects the results of these firms.

- (vi)

Participation of foreign funds. Generally, the presence of funds from other countries generates an increase in value for companies. In this context, Giannetti, Liao, and Yu (2015) contribute to the literature related to the effects of board skills on company results, describing directors with international experience conveying the knowledge acquired from this experience, and generating efficiency gains by improving monitoring in the emerging markets, suggesting the idea that the participation of foreign funds can be beneficial to Brazilian companies.

- (vii)

Participation of state-owned funds. Differences in the compensation structures for private and state-owned pension funds imply potential differences in the incentives to monitor companies that are partly owned by these investors (Karpoff, Lee, & Vendrzyk, 1999). This is mainly due to the fact that public funds are influenced by politicians, who are elected by people who do not necessarily have the same interests as the beneficiaries of the funds, indicating that the participation of public funds can jeopardize the performance of a company (Becht et al., 2009).

- (viii)

Participation in the governance index. The impact in the capital markets of the companies⬢ participation at differentiated levels of governance is dubious. Almeida, Santos, Ferreira, and Torres (2010) affirm that participation in this index brings substantial benefits to companies, especially in terms of transparency, positively affecting their financial returns. Ferreira (2012) and Macedo and Corrar (2012) did not identify superior results for companies with good corporate governance practices, casting doubt on the importance of this index in increasing company performance.

- (ix)

Temporal and industrial fixed effects. To identify the industrial fixed effects, dummies are used for each sectorial classification of ECONOMATICA. Pedersen and Thomsen (1997) stated that firms in the same industry tend to have similar ownership structures, and Morck, Shleifer, and Vishny (1990) have shown that it is necessary to identify efficiency according to the field of activity, indicating that the quality of the business may be directly related to the industrial environment in which it operates. Dummies for each year of analysis are also added to identify whether specific events during this period have significant influences on the study, and as a control to prevent these events from distorting the results.

As reflected in the literature review and the construction of the hypotheses, private pension entities began to be more common in the Brazilian market during the period of study, mainly because of the increased resources accumulated by them, their acquisition of assets and their participation in the decisions of companies through the acquisition of common shares. This has raised the question of the effectiveness of their intervention in financial results. To study this issue, the descriptive statistics and correlations, as well as the linear and non-linear analyses of the relationship between the control structure of the pension funds and the company performance, are presented.

Descriptive statistics and correlationAs laid out in the methodology, before starting the analysis the variables are tested for correlation and the data are checked for consistency using the descriptive statistics. As expected, a strong correlation (above 0.7) is identified between the variables AP (principal shareholder), TPA (three largest shareholders) and CPA (five largest shareholders), between return on assets (ROA) and return on equity (ROE), between EBITDA (earnings before interest, taxes, depreciation and amortization) and PL (equity) and between the Tobin's Q and MB (market-to-book). To avoid multicollinearity problems, none of these variables with high correlations is used in the same regression. Afterwards, the descriptive statistics are analysed.

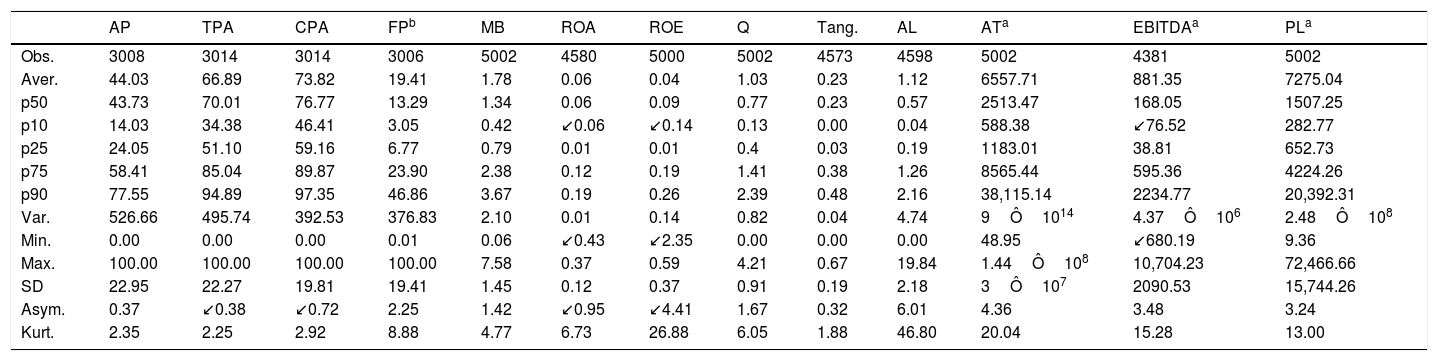

As shown in Table 2, after the application of the winsorization of 1%, the variables related to the ownership and control structures show very close averages and medians. On average, pension funds have 19.41% of the control of the companies in the analysis, with the main shareholder and the three and five largest shareholders having, respectively, around 44.03%, 66.89% and 73.82% of the shares of the companies, evidencing a very high stock concentration; this is a common feature in Brazilian companies, which are mostly owned by families.

Descriptive statistics.

| AP | TPA | CPA | FPb | MB | ROA | ROE | Q | Tang. | AL | ATa | EBITDAa | PLa | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Obs. | 3008 | 3014 | 3014 | 3006 | 5002 | 4580 | 5000 | 5002 | 4573 | 4598 | 5002 | 4381 | 5002 |

| Aver. | 44.03 | 66.89 | 73.82 | 19.41 | 1.78 | 0.06 | 0.04 | 1.03 | 0.23 | 1.12 | 6557.71 | 881.35 | 7275.04 |

| p50 | 43.73 | 70.01 | 76.77 | 13.29 | 1.34 | 0.06 | 0.09 | 0.77 | 0.23 | 0.57 | 2513.47 | 168.05 | 1507.25 |

| p10 | 14.03 | 34.38 | 46.41 | 3.05 | 0.42 | ↙0.06 | ↙0.14 | 0.13 | 0.00 | 0.04 | 588.38 | ↙76.52 | 282.77 |

| p25 | 24.05 | 51.10 | 59.16 | 6.77 | 0.79 | 0.01 | 0.01 | 0.4 | 0.03 | 0.19 | 1183.01 | 38.81 | 652.73 |

| p75 | 58.41 | 85.04 | 89.87 | 23.90 | 2.38 | 0.12 | 0.19 | 1.41 | 0.38 | 1.26 | 8565.44 | 595.36 | 4224.26 |

| p90 | 77.55 | 94.89 | 97.35 | 46.86 | 3.67 | 0.19 | 0.26 | 2.39 | 0.48 | 2.16 | 38,115.14 | 2234.77 | 20,392.31 |

| Var. | 526.66 | 495.74 | 392.53 | 376.83 | 2.10 | 0.01 | 0.14 | 0.82 | 0.04 | 4.74 | 9Ô1014 | 4.37Ô106 | 2.48Ô108 |

| Min. | 0.00 | 0.00 | 0.00 | 0.01 | 0.06 | ↙0.43 | ↙2.35 | 0.00 | 0.00 | 0.00 | 48.95 | ↙680.19 | 9.36 |

| Max. | 100.00 | 100.00 | 100.00 | 100.00 | 7.58 | 0.37 | 0.59 | 4.21 | 0.67 | 19.84 | 1.44Ô108 | 10,704.23 | 72,466.66 |

| SD | 22.95 | 22.27 | 19.81 | 19.41 | 1.45 | 0.12 | 0.37 | 0.91 | 0.19 | 2.18 | 3Ô107 | 2090.53 | 15,744.26 |

| Asym. | 0.37 | ↙0.38 | ↙0.72 | 2.25 | 1.42 | ↙0.95 | ↙4.41 | 1.67 | 0.32 | 6.01 | 4.36 | 3.48 | 3.24 |

| Kurt. | 2.35 | 2.25 | 2.92 | 8.88 | 4.77 | 6.73 | 26.88 | 6.05 | 1.88 | 46.80 | 20.04 | 15.28 | 13.00 |

Legend: AP, principal shareholder; TPA, three largest shareholders; CPA, five largest shareholders; FP, pension funds; MB, market-to-book; ROA, return on assets; ROE, return on equity; Q, Tobin's Q; Tang., tangibility; AL, leverage; AT, total assets; EBITDA, earnings before interest, taxes, depreciation and amortization; PL, equity; p, percentiles; SD, standard deviation.

The other control variables, with the exceptions of ROA and tangibility, show differences between their averages and medians, evidencing the need to use winsorization of 1%. Companies generally have a market value that exceeds their equity by 78% (MB), while their market value exceeds their total assets by, on average 3% (Tobin's Q). In terms of leverage, for each R$ 1.00 of equity, these companies are indebted in the short and long term by around R$ 1.12. ROA and ROE have similar averages, indicating that around 6% of total assets are converted into operating income and 4% of equity is converted into income. The companies have around 23% of tangible assets in relation to total assets.

Finally, with regard to size variables, the companies have, on average, EBITDA of around R$ 881.35 thousand, total assets of R$ 6.56 million and equity of R$ 7.27 million. These variables show differences between their averages and medians, evidencing the need for winsorization. They also present fairly high variances and standard deviations, necessitating the application of the Naperian logarithm. In the variables related to the control structure (with the exception of the principal shareholder variable) and those related to the internal performance (ROA and ROE), the asymmetric distribution is negative (the mean is lower than the median); in the other variables, the asymmetric distribution is positive. Looking at kurtosis, for the variables related to ownership structure (AP, TPA and CPA) and tangibility, the frequency curve is more open (platykurtic), while for the other variables, the frequency curve is more closed (leptokurtic).

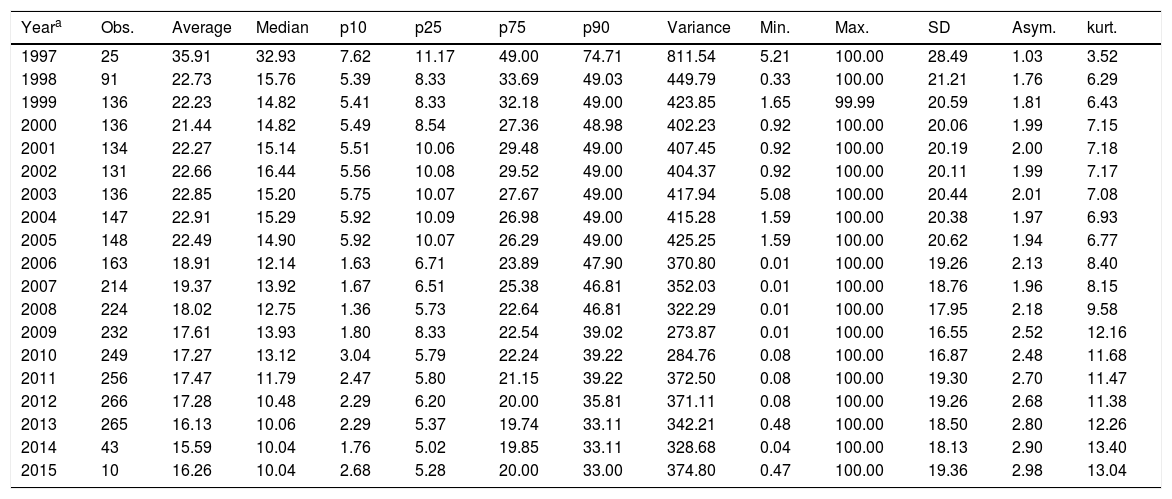

After the adjustments, the variables present consistent and expected patterns, with averages and medians near to each other. In order to gain a better understanding of the evolution of the control structure of pension funds over time, Table 3 is presented. As can be seen, the percentage of shares owned by pension funds has decreased considerably over the years, which is evidence that, although the assets of pension funds have increased and they are considered the most important institutional investors in the country, as discussed in ⬓Pension funds as a monitoring mechanism⬽ section, the participation of these funds in the control of companies has been decreasing over the period of study.

Percentages of control by pension funds in companies over time.

| Yeara | Obs. | Average | Median | p10 | p25 | p75 | p90 | Variance | Min. | Max. | SD | Asym. | kurt. |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1997 | 25 | 35.91 | 32.93 | 7.62 | 11.17 | 49.00 | 74.71 | 811.54 | 5.21 | 100.00 | 28.49 | 1.03 | 3.52 |

| 1998 | 91 | 22.73 | 15.76 | 5.39 | 8.33 | 33.69 | 49.03 | 449.79 | 0.33 | 100.00 | 21.21 | 1.76 | 6.29 |

| 1999 | 136 | 22.23 | 14.82 | 5.41 | 8.33 | 32.18 | 49.00 | 423.85 | 1.65 | 99.99 | 20.59 | 1.81 | 6.43 |

| 2000 | 136 | 21.44 | 14.82 | 5.49 | 8.54 | 27.36 | 48.98 | 402.23 | 0.92 | 100.00 | 20.06 | 1.99 | 7.15 |

| 2001 | 134 | 22.27 | 15.14 | 5.51 | 10.06 | 29.48 | 49.00 | 407.45 | 0.92 | 100.00 | 20.19 | 2.00 | 7.18 |

| 2002 | 131 | 22.66 | 16.44 | 5.56 | 10.08 | 29.52 | 49.00 | 404.37 | 0.92 | 100.00 | 20.11 | 1.99 | 7.17 |

| 2003 | 136 | 22.85 | 15.20 | 5.75 | 10.07 | 27.67 | 49.00 | 417.94 | 5.08 | 100.00 | 20.44 | 2.01 | 7.08 |

| 2004 | 147 | 22.91 | 15.29 | 5.92 | 10.09 | 26.98 | 49.00 | 415.28 | 1.59 | 100.00 | 20.38 | 1.97 | 6.93 |

| 2005 | 148 | 22.49 | 14.90 | 5.92 | 10.07 | 26.29 | 49.00 | 425.25 | 1.59 | 100.00 | 20.62 | 1.94 | 6.77 |

| 2006 | 163 | 18.91 | 12.14 | 1.63 | 6.71 | 23.89 | 47.90 | 370.80 | 0.01 | 100.00 | 19.26 | 2.13 | 8.40 |

| 2007 | 214 | 19.37 | 13.92 | 1.67 | 6.51 | 25.38 | 46.81 | 352.03 | 0.01 | 100.00 | 18.76 | 1.96 | 8.15 |

| 2008 | 224 | 18.02 | 12.75 | 1.36 | 5.73 | 22.64 | 46.81 | 322.29 | 0.01 | 100.00 | 17.95 | 2.18 | 9.58 |

| 2009 | 232 | 17.61 | 13.93 | 1.80 | 8.33 | 22.54 | 39.02 | 273.87 | 0.01 | 100.00 | 16.55 | 2.52 | 12.16 |

| 2010 | 249 | 17.27 | 13.12 | 3.04 | 5.79 | 22.24 | 39.22 | 284.76 | 0.08 | 100.00 | 16.87 | 2.48 | 11.68 |

| 2011 | 256 | 17.47 | 11.79 | 2.47 | 5.80 | 21.15 | 39.22 | 372.50 | 0.08 | 100.00 | 19.30 | 2.70 | 11.47 |

| 2012 | 266 | 17.28 | 10.48 | 2.29 | 6.20 | 20.00 | 35.81 | 371.11 | 0.08 | 100.00 | 19.26 | 2.68 | 11.38 |

| 2013 | 265 | 16.13 | 10.06 | 2.29 | 5.37 | 19.74 | 33.11 | 342.21 | 0.48 | 100.00 | 18.50 | 2.80 | 12.26 |

| 2014 | 43 | 15.59 | 10.04 | 1.76 | 5.02 | 19.85 | 33.11 | 328.68 | 0.04 | 100.00 | 18.13 | 2.90 | 13.40 |

| 2015 | 10 | 16.26 | 10.04 | 2.68 | 5.28 | 20.00 | 33.00 | 374.80 | 0.47 | 100.00 | 19.36 | 2.98 | 13.04 |

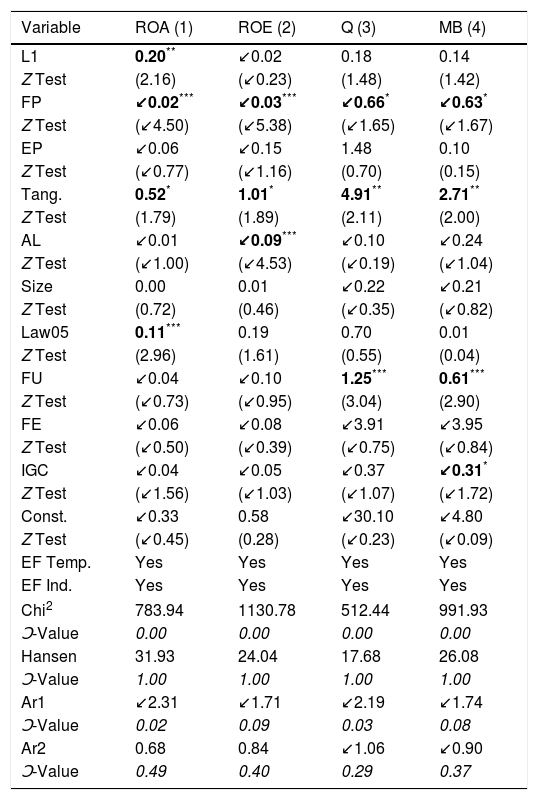

To examine the linear relationship between the control structure of the pension funds and company performance, the unbalanced panel data method is applied by GMM-Sys. As shown in Table 4, the Arellano and Bond (1991) test (Ar1 and Ar2) indicates that the model rejects the null hypothesis of no serial correlation in the first order residuals, and does not reject a second order serial correlation. Thus, the model presents serial correlation of first order, justifying the use of dynamic GMM-Sys. For the Hansen test (1982), the null hypothesis is not rejected, which is evidence that there are no specification problems in the instrumental variables. The instruments used are the lagged independent variables, as suggested by Almeida, Campello, et al. (2010). Finally, the Chi-square test (¿2) is applied, and the null hypothesis is rejected, indicating that there is an association within the group of variables.

Linear regression analysis on internal and market performance.

| Variable | ROA (1) | ROE (2) | Q (3) | MB (4) |

|---|---|---|---|---|

| L1 | 0.20** | ↙0.02 | 0.18 | 0.14 |

| Z Test | (2.16) | (↙0.23) | (1.48) | (1.42) |

| FP | ↙0.02*** | ↙0.03*** | ↙0.66* | ↙0.63* |

| Z Test | (↙4.50) | (↙5.38) | (↙1.65) | (↙1.67) |

| EP | ↙0.06 | ↙0.15 | 1.48 | 0.10 |

| Z Test | (↙0.77) | (↙1.16) | (0.70) | (0.15) |

| Tang. | 0.52* | 1.01* | 4.91** | 2.71** |

| Z Test | (1.79) | (1.89) | (2.11) | (2.00) |

| AL | ↙0.01 | ↙0.09*** | ↙0.10 | ↙0.24 |

| Z Test | (↙1.00) | (↙4.53) | (↙0.19) | (↙1.04) |

| Size | 0.00 | 0.01 | ↙0.22 | ↙0.21 |

| Z Test | (0.72) | (0.46) | (↙0.35) | (↙0.82) |

| Law05 | 0.11*** | 0.19 | 0.70 | 0.01 |

| Z Test | (2.96) | (1.61) | (0.55) | (0.04) |

| FU | ↙0.04 | ↙0.10 | 1.25*** | 0.61*** |

| Z Test | (↙0.73) | (↙0.95) | (3.04) | (2.90) |

| FE | ↙0.06 | ↙0.08 | ↙3.91 | ↙3.95 |

| Z Test | (↙0.50) | (↙0.39) | (↙0.75) | (↙0.84) |

| IGC | ↙0.04 | ↙0.05 | ↙0.37 | ↙0.31* |

| Z Test | (↙1.56) | (↙1.03) | (↙1.07) | (↙1.72) |

| Const. | ↙0.33 | 0.58 | ↙30.10 | ↙4.80 |

| Z Test | (↙0.45) | (0.28) | (↙0.23) | (↙0.09) |

| EF Temp. | Yes | Yes | Yes | Yes |

| EF Ind. | Yes | Yes | Yes | Yes |

| Chi2 | 783.94 | 1130.78 | 512.44 | 991.93 |

| Ͻ-Value | 0.00 | 0.00 | 0.00 | 0.00 |

| Hansen | 31.93 | 24.04 | 17.68 | 26.08 |

| Ͻ-Value | 1.00 | 1.00 | 1.00 | 1.00 |

| Ar1 | ↙2.31 | ↙1.71 | ↙2.19 | ↙1.74 |

| Ͻ-Value | 0.02 | 0.09 | 0.03 | 0.08 |

| Ar2 | 0.68 | 0.84 | ↙1.06 | ↙0.90 |

| Ͻ-Value | 0.49 | 0.40 | 0.29 | 0.37 |

Legend: ROA, return on assets; ROE, return on equity; Q, Tobin's Q; MB, market-to-book; L1, dynamic variable (lag of the dependent variable); FP, pension funds; EP, ownership structure of principal shareholder, three largest shareholders or five largest shareholders; Tang., tangibility; AL, leverage; Size, total assets, EBITDA or equity; FU, state-owned pension funds; FE, foreign pension funds; IGC, Corporate Governance Index; Const., constant; EF Temp., temporal fixed effects; EF Ind., industrial fixed effects; Chi2, Chi-square test; Hansen, Hansen test; Ar1 and Ar2, serial correlation of first and second order.

In general, the control structure of pension funds is negatively related to efficiency, both in the ROA and ROE and in the market performance (Tobin's Q and MB) regressions. In the results, a 1% increase in the control structure of pension funds causes a decrease in the return on assets of 0.02% and in the return on equity of 0.03%, both at a level of significance of 1%. In terms of market performance, the decrease in relation to Tobin's Q is 0.66% and in relation to MB is 0.63%, both at a significance level of 10%. This result corroborates those of Carleton et al. (1998) and Woidtke (2002), who infer that an increase in the control structure of pension funds generates a reduction in the performance of companies because the pension funds do not have adequate monitoring abilities, generating conflicts that go against the objective of the maximization of value.

In terms of control variables, a negative relationship is found between the profitability of the companies and the ownership structure of the main shareholder. The logic is reversed when the relationship with market performance is analysed, but in none of the analyses is this variable significant (regressions with three and five shareholders were tested, but the results were qualitatively similar). In all regressions, the tangibility of the assets shows a positive and significant relationship with efficiency, with a 1% increase in this variable generating an increase of 0.52% in the return on assets and 1.01% in the return on equity, at a level of significance of 10%, and increases of 4.91% and 2.71% in market return (Tobin's Q and MB), at a level of significance of 5%. This result contradicts the results of Pöyry and Maury (2010), who asserted that tangibility represents costly resources for the company, generating a decrease in its results.

When analysing leverage, it is perceived that a 1% increase in this variable decreases the return on equity by 0.09%, at a significance level of 1%. In other regressions, this relationship is not significant. This result corroborates the results of Boubakri and Cosset (1998), who identified a downward trend in leverage as efficiency increases, because an increase in indebtedness may hinder the efficient allocation of resources. With regard to Law no. 11,053/2004, which introduced reforms in the taxation of pension plans related to capital market investments, this is positively and significantly related to the ROA, indicating that its implementation generated an increase of 0.11% in the return on assets, at a level of significance of 1%, corroborating the results of Colombo and Caldeira (2016).

The variables related to size are not statistically significant. On the other hand, the presence of public pension funds positively affects the market value of companies, with a 1% increase in the participation of these funds generating an increase of 1.25% in Tobin's Q and 0.61% in MB, both at a significance level of 1%. Although this result does not match the results of Becht et al. (2009), it is important to consider that some of the most important pension funds in Brazil are public. The variable related to the company's participation in the Governance Index shows a negative and significant relationship with MB, with a 1% increase in participation in this index generating a decrease of 0.31% in the market value of the company, at a 10% level of significance, corroborating the results of Ferreira (2012) and Macedo and Corrar (2012). The participation of foreign funds is not significant in any analysis.

Finally, dummies are used for the industrial and temporal fixed effects in all the regressions, to take into account the sectorial particularities and conditions of each year covered in the analysis. The dynamic model is also presented, where the lagged dependent variable is used as an explanatory variable. In this case, only the dynamic variable of regression 1 is significant, which is evidence that an increase in performance in one year positively influences the return on assets in the next period.

In what follows, the results are presented with a non-linear relationship between the variables being considered.

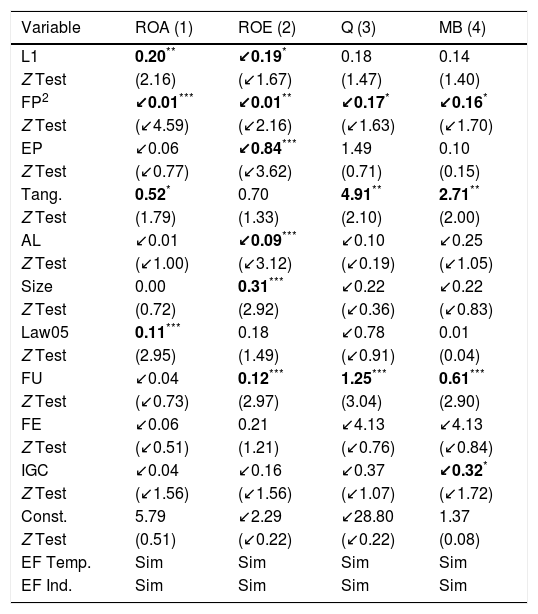

Non-linear analysis of the relationship between control structure of pension funds and performanceTo check the consistency of the results, the possible quadratic relationship (where the main independent variable is squared) between the control percentage of the funds and the financial performance or the market value of the companies is analysed. As can be seen in Table 5, the results are qualitatively similar to those found in the linear analysis, but they have a smaller magnitude: a 1% increase in the control structure decreases the return on assets and the return on equity by 0.01%, at significance levels of 1% and 5%, respectively, and the market performance by 0.17% and 0.16%, both at a significance level of 10%.

Non-linear regression analysis on domestic and market performance.

| Variable | ROA (1) | ROE (2) | Q (3) | MB (4) |

|---|---|---|---|---|

| L1 | 0.20** | ↙0.19* | 0.18 | 0.14 |

| Z Test | (2.16) | (↙1.67) | (1.47) | (1.40) |

| FP2 | ↙0.01*** | ↙0.01** | ↙0.17* | ↙0.16* |

| Z Test | (↙4.59) | (↙2.16) | (↙1.63) | (↙1.70) |

| EP | ↙0.06 | ↙0.84*** | 1.49 | 0.10 |

| Z Test | (↙0.77) | (↙3.62) | (0.71) | (0.15) |

| Tang. | 0.52* | 0.70 | 4.91** | 2.71** |

| Z Test | (1.79) | (1.33) | (2.10) | (2.00) |

| AL | ↙0.01 | ↙0.09*** | ↙0.10 | ↙0.25 |

| Z Test | (↙1.00) | (↙3.12) | (↙0.19) | (↙1.05) |

| Size | 0.00 | 0.31*** | ↙0.22 | ↙0.22 |

| Z Test | (0.72) | (2.92) | (↙0.36) | (↙0.83) |

| Law05 | 0.11*** | 0.18 | ↙0.78 | 0.01 |

| Z Test | (2.95) | (1.49) | (↙0.91) | (0.04) |

| FU | ↙0.04 | 0.12*** | 1.25*** | 0.61*** |

| Z Test | (↙0.73) | (2.97) | (3.04) | (2.90) |

| FE | ↙0.06 | 0.21 | ↙4.13 | ↙4.13 |

| Z Test | (↙0.51) | (1.21) | (↙0.76) | (↙0.84) |

| IGC | ↙0.04 | ↙0.16 | ↙0.37 | ↙0.32* |

| Z Test | (↙1.56) | (↙1.56) | (↙1.07) | (↙1.72) |

| Const. | 5.79 | ↙2.29 | ↙28.80 | 1.37 |

| Z Test | (0.51) | (↙0.22) | (↙0.22) | (0.08) |

| EF Temp. | Sim | Sim | Sim | Sim |

| EF Ind. | Sim | Sim | Sim | Sim |

Legend: ROA, return on assets; ROE, return on equity; Q, Tobin's Q; MB, market-to-book; L1, dynamic variable (lag of the dependent variable); FP2, pension funds squared; EP, ownership structure of principal shareholder, three largest shareholders or five largest shareholders; Tang., tangibility; AL, leverage; Size, total assets, EBITDA or equity; FU, state-owned pension funds; FE, foreign pension funds; IGC, Corporate Governance Index; Const., constant; EF Temp, temporal fixed effects; EF Ind., industrial fixed effects.

In terms of control variables, the ownership structure of the main shareholder has a negative influence on the profitability of companies, with a 1% increase in this variable generating a 0.84% decrease in return on equity. This result corroborates the results of the studies of La Porta et al. (1999) and Sonza and Kloekner (2014), who propose that this negative relationship found in Brazilian companies is due to the fact that, in countries with weak legal protection, a more concentrated structure can generate expropriation of minority shareholders, decreasing the efficiency of the company.

As in the previous analysis, tangibility is positively and significantly related to efficiency in regressions 1, 3 and 4, showing that a 1% increase in the company's fixed assets in relation to the total generates a 0.52% increase in ROA, at a significance level of 10%, and an increase of 4.91% and 2.71% in market performance (Tobin's Q and MB), at a significance level of 5%. Leverage is negative and significantly related to ROE, with a 1% increase in this variable generating a 0.09% decrease in return on equity, at a significance level of 1%, corroborating the study of Boubakri and Cosset (1998).

Size is positively related to performance, with a 1% increase in total assets generating a 0.31% increase in return on equity, at a significance level of 1%, corroborating the results of Pedersen and Thomsen (1997) that were discussed in the methodology section. With respect to the dummy representing Law no. 11,053/2004, this was positively and significantly related to the internal performance of the companies: the results indicate that the implementation of this law generated a 0.11% increase in return on assets, at a level of significance of 1%. This result was expected because, according to Colombo and Caldeira (2016), this law encouraged pension funds to invest more actively in the capital markets, generating a greater return to companies.

The results related to the participation of state-owned funds are similar to those found in the linear analysis, with a 1% increase in their participation generating an increase of 0.12% in ROE, 1.25% in Tobin's Q and 0.61% in market-to-book, at a significance level of 1%. By contrast, the influence of foreign funds is not significant in any analysis. Finally, the participation in the Corporate Governance Index is negatively related to performance in all regressions, being significant only in regression 4, as in the previous analysis. The dynamic variable is negative and significant at 5% in relation to ROA and positive and significant at 10% in relation to ROE. The industrial and temporal fixed effects in this analysis are also considered. The conclusions, contributions and limitations of the study are presented below.

Conclusions, contributions and limitations of the studyThe present article seeks to verify the influence of the control structure of pension funds on the performance of Brazilian public companies. The results show that these funds are not good monitors, since their control structure is negatively related to the internal and market performance of the companies. This leads to a rejection of hypothesis H1, but not the alternative hypothesis (H1A). These results corroborate those of Giannetti and Laeven (2009), Wahal (1996), Gillan and Starks (2000), Carleton et al. (1998), Woidtke (2002) and Harris et al. (2014). The conclusion is that when pension funds invest in the capital markets, they are not concerned with the specific decision-making of the companies, and thus there is a lack of adequate monitoring skills, provoking conflicts that go against the objective of maximizing the company's value.

When variables related to the ownership structure of the main shareholders are inserted, they are found to be negatively related to the profitability of the companies in the non-linear regressions, corroborating the findings of La Porta et al. (1999) and Sonza and Kloekner (2014). The size of the company is positively and significantly related to profitability in the non-linear regressions, showing that the larger the firm, more professional and efficient it is (Pedersen & Thomsen, 1997). Leverage, as expected and as suggested by the study of Boubakri and Cosset (1998), shows an inverse relationship with the return on equity in the two analyses, providing evidence that the higher the profitability, the less these companies seek indebtedness.

As expected, Law no. 11,053/2004 encouraged pension funds to invest more actively in the capital markets, generating a higher return for companies that had participation from these institutional investors (Colombo & Caldeira, 2016); this is shown in the linear and non-linear regressions referring to the return on assets. The study also demonstrates that the fact that companies participate in the Corporate Governance Index in the capital markets does not generate an increase in market performance; this was also shown by the findings of Ferreira (2012) and Macedo and Corrar (2012).

A few other issues have arisen in the course of the analysis. Asset tangibility is positive and significant in most of the results, showing that investment in tangible assets can be beneficial to company performance, contrary to the findings of Pöyry and Maury (2010). The fact that the state-owned pension funds invest in the companies generates a positive and significant return, mainly in market performance, contrary to the study of Becht et al. (2009), but a positive relationship between state-owned pension funds and financial performance (with the exception of ROE in non-linear analysis) is not proved. It is therefore possible that investors ascribe greater value to shares in companies in which domestic public funds have investments, even though they have no evidence that such funds improve the profitability of those companies. The participation of foreign funds does not significantly influence the results in any analysis.

This article has both theoretical and empirical contributions. In theoretical terms, it provides a better understanding of the concepts of the control structure of pension funds, an issue that has not been very much explored in Brazil. The theoretical review has shown that there is a controversy about the influence of the control structure of pension funds on the performance of companies. In practical terms, dynamic models of multiple linear and non-linear regressions, estimated by GMM-Sys, are used in an unbalanced panel of Brazilian companies from 1995 to 2015 to estimate the influence of the control structure of pension funds on performance, giving important results that help to clarify issues related to the monitoring of publicly traded Brazilian companies.

Some limitations that should be considered are the difficulty of comparing these results with other studies carried out in Brazil on the relationship between the control structure of pension funds and company performance, because research papers on this topic are few and very sparse. Another constraint concerns the fact that the relationship between efficiency and control structure may be endogenous. Suggestions for future research are the expansion of this study through a sectorial division, and by obtaining a sample covering all institutional investors in the Brazilian capital markets. Another suggestion would be to check whether there is a relationship between the managers of private funds and the advisers of companies.

Conflicts of interestThe authors declare no conflicts of interest.