This paper studies the evolution of auditing in Portugal, in an historical, legal and empirical perspective, since monarchy to the present day. This historical development began with the Código de Comércio published in 1888 (Commerce Law), the first law that focused on independent surveillance of public limited companies.

The economical and social context of the emergence of the auditor (Revisor Oficial de Contas), and the pattern adopted will also be commented. The present position of the profession is analyzed in an empirical study on the structure of the market demand and the offer, as well as the concentration of the statutory audit market in Portugal. In this analysis, we used data provided by Institute of Statutory Auditors (OROC), and reached the conclusion that the statutory audit market in Portugal, in the four years prior to the general use of the point system, from 2001 to 2004, a concentration tendency regarding listed and unlisted companies, was shown.

1. Introduction

The historical evolution of company auditing, in the context of the market economy, has been generally discussed in the various countries, because of its importance in the democratic system. A database of information is essential, permitting constant control and monitoring of the existence and efficient usage of resources.

The market economy, as a system of exchange partially self regulated, develops accountability systems, with the aim of being accountable and controlling the economy.

This inevitably led to the emergence of new laws and regulations accepted by the economic agents. This surveillance results in an auditing market, whose nature has been analyzed in various countries, especially in Anglo Saxon countries.

Moizer (1987, p. 118-123) assesses the English auditing market based on a methodology that takes into account the difficulty to measure quality of an audit ex-ante. Also the issue of the independence of the auditors in relation to the companies they are auditing and the self-regulation of the profession based on a monopoly with a strong professional structure. The author reaches the conclusion that the English market is strongly concentrated, Marten (1997, p. 7-23) reached the same conclusion in the case of the German market and Benau & Martinez (1998, p. 103-121) for Spain. This market monopoly, especially in the case of listed companies, could result in the establishment of explicit or implicit agreements (Dopuch & Simunic, 1980, p. 113).

In Portugal, there has been no study to quantify the degree of concentration or the tendency, regarding all companies subject to statutory audit of accounts. This is the objective of this study and it also aims to analyze the structure of the offer and demand of the auditing services and the concentration of the auditing market in Portugal, both as regards to auditing companies who audit listed companies and the rest of the market. For this effect, we used the data provided by the Institute of Auditors, in their annual reports, as well as the information collected by us regarding audit companies who audit listed companies. After collecting the said information we used various statistical tools to test the objectives of the study.

We came to the conclusion that in the case of listed companies, in a regulated market, the concentration process is clear. As for the unlisted companies, subject to statutory auditing, the administrative practice until 2004, created a relatively balanced distribution by all the auditors both in points and in geographical terms. However our study shows a concentration tendency since the years 2001, 2002, 2003 and 2004. The year 2004 is considered the year of change, because the paradigm changed. The points1 cease to be a criterion for the distribution of the companies.

The study is structured in four sections: first, we outlined the international framework of company auditing. Secondly we researched the legal-historical evolution of the profession in Portugal, from the beginning, during the monarchy to date, and then we analyzed the auditing market in Portugal, both from the point of view of the offer and the demand and lastly, we studied the concentration of the audit market.

2. International framework of auditing of companies

2.1. International position

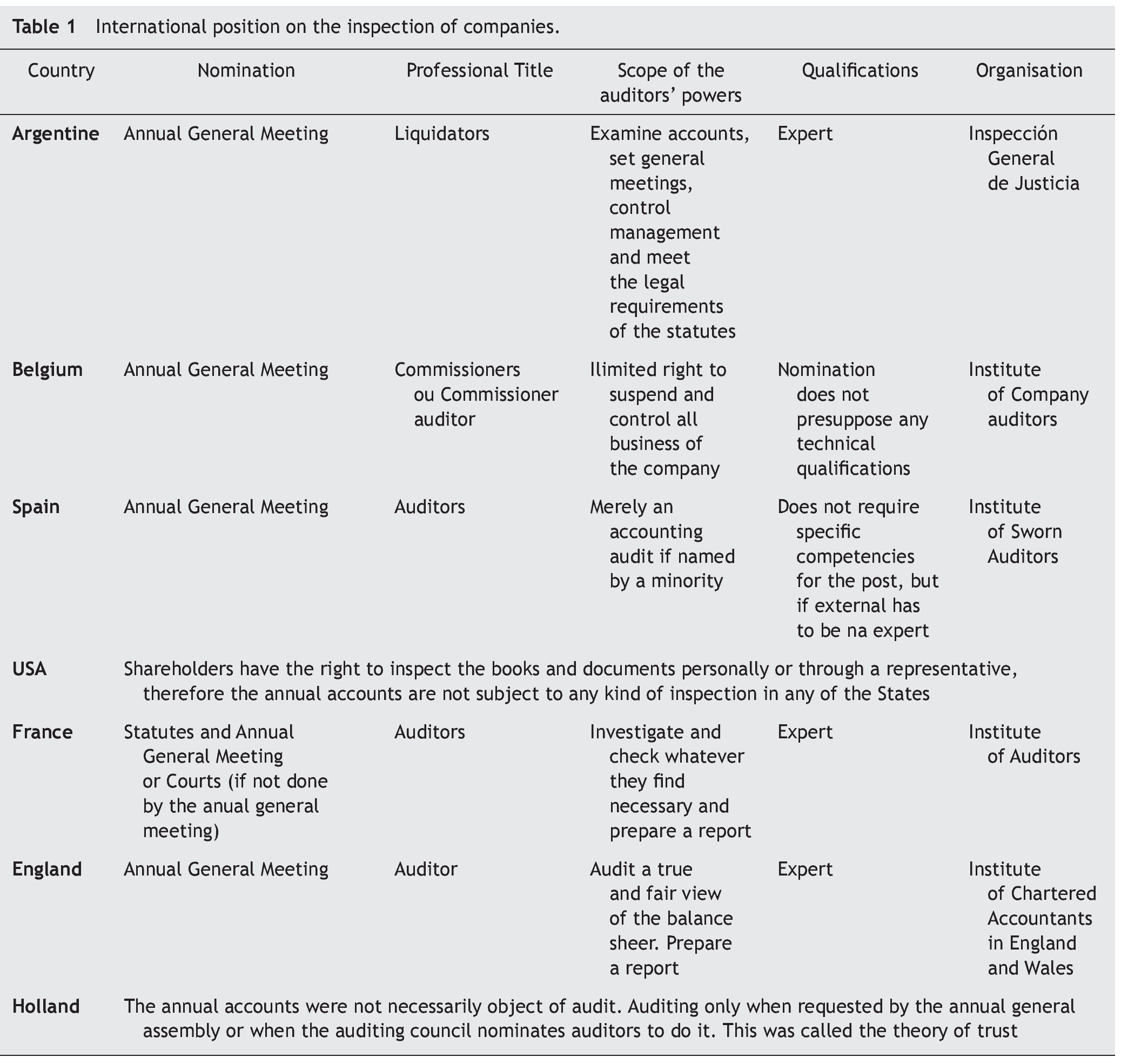

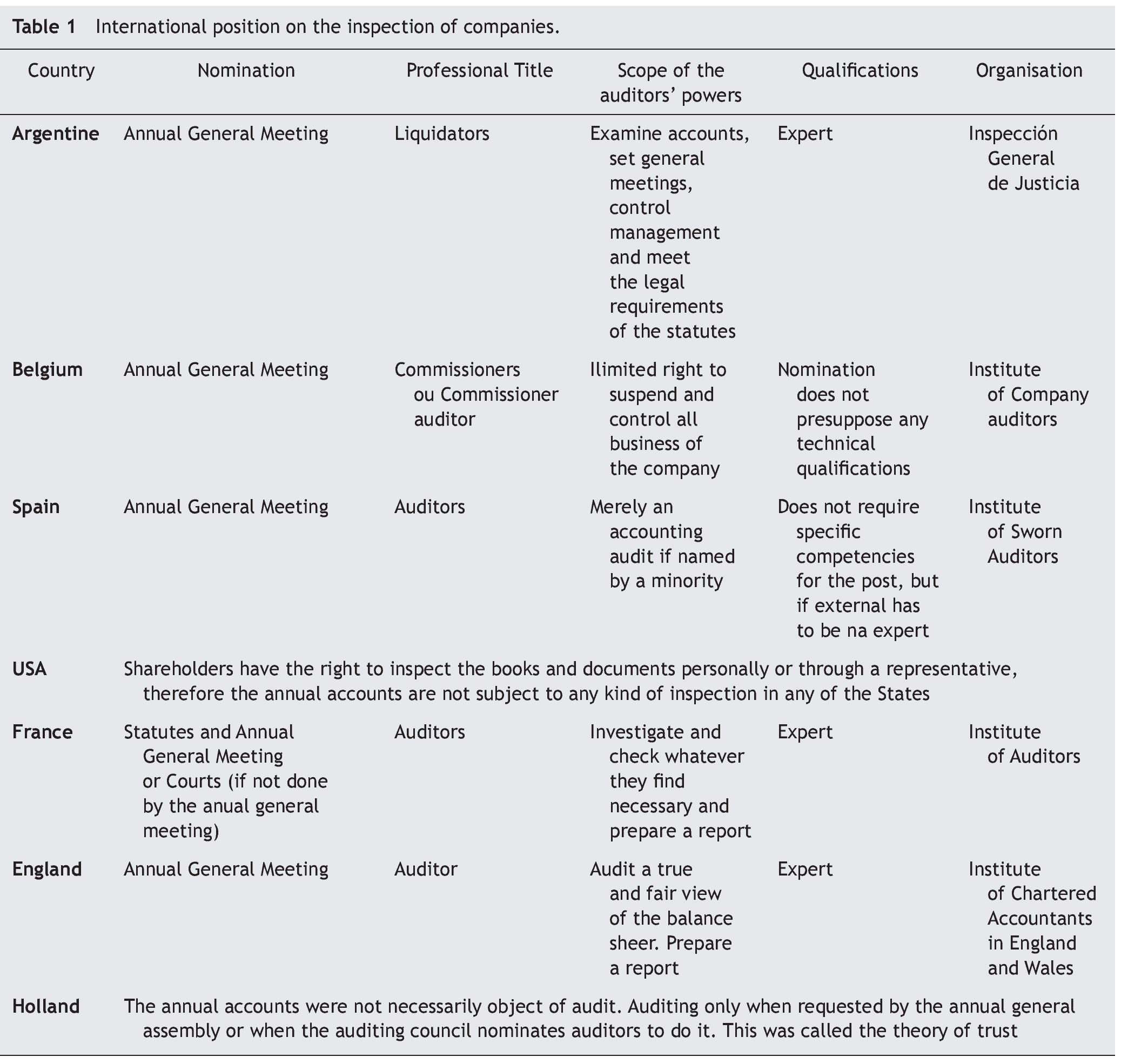

The international position, on about 1972, was as follows (Table 1).1

In terms of compared international practice, the auditing of companies differed greatly from country to country. Although in the Anglo Saxon countries, the scope of audit control of the companies had a more liberal and pragmatic approach, in England the law did not require any analogous control mechanism of the audit committee, so the audits were done by accountants, who did the normal auditing of companies2 and would give a true and fair view of the balance sheet and the business position of the company (Harris, 1937, p. 38). The extra control was done under the auspices of the board of trade3 and is more comprehensive and thorough, and could be requested by the representing shareholders or the court. These inspectors had extensive powers in the exercise of their profession. In the United States, the shareholders were not even questioned about the reason for requesting an audit. This could be done personally or by their mandatory's — right of inspection (Ballantine, 1946, p. 376). In effect the number of possibilities they have to check the societies or the administrators, and the extensive use that the courts make of the principle of equity, should in itself be sufficient inspire trust (Pimenta, 1972, p. 292).

In Holland, the philosophy of the theory of trust (Keuzenkamp, 1938, p. 180) implied that the annual accounts should be trustworthy giving the experts power to assess how manage ment was done.

The Spanish doctrine (Tena, 1959, p. 481) foresees that the unanimously nominated auditors, who had to be shareholders, could examine the accounts themselves or together with experts, all the accounts and everything connected with it in great detail. On the other hand the inspectors nominated by minority shareholders were only permitted to audit the accounts.4

In the French doctrine shareholding companies had to have public share capital and any who were not funded this way, but had a certain capital,5 should nominate "comissaires aux comptes" (auditors), whose duties were not limited to the preparation of the annual reports. By Law they could provide consultancy to the administration board, prepare annual accounts and, also report to the general meeting, any irregularities or discrepancies and also to the public prosecutor, any public crimes.

In Italy, the collegio sindicale had a similar function to the Portuguese audit committee, it was not their duty to do a full audit, not even from an accounting point of view let alone assess the opportunity or merit of the management (Colombo, 1969, p. 471). It made no difference, but in the case of in certain companies,6 one of the sindaci was chosen from the revisori ufficiali.

3. Historical judicial evolution of auditing in Portugal: From the Monarchy to the present day

The majority of the dictionaries do not associate the term auditing with accountancy. As a result there are a great number of research activities which are called by the researchers, audits. So in the primitive legal system of the Portuguese monarchy, there was the Ouvidor (ombudsman), whose duty was to hear the parties, collect evidence and bring the case to the master for a decision, that is, to higher instances. The ouvidor were magistrates, who performed a similar duty to auditing, because their work was to listen, think and collect evidence, so that if necessary, he was able to inform about the compliance of the procedures adopted with the standards set. This function, as the surrounding complexity increased, was successively subjected to a process of depuration and differentiation.7

In 1372, the "Vedores da Fazenda" (tax inspectors) substituting the "Ouvidores" with an important duty which included deciding on issues resulting from the administration of the kingdom, the collection of revenue and payment of public expenses. These tax inspectors, according to "Afonsine" ordinances, controlled the royal assets and public finances. Both the "Ouvidores" and the "Vedores", can be considered, in Portugal, in etymological terms, the forefathers of the expert accountants, because when questioned in court and by the administration, it was their duty to hear the parties, check the evidence and decide.

The Commercial Code8 approaches for the first time in 1888, the auditing of companies and awarded9 this duty to the board of auditors, elected by the general meeting and made up by at least three shareholders. The duties of the auditors board, was in general to:

— Audit the recording of accounts of the company;

— Audit the administration of the company;

— Check that the statutes of the company are adhered to;

— Give an opinion on the balance sheet, inventory (stock) and the administration report.

We are at the end of the 19th century. The majority of the authors10 researching this field of auditing, are unanimous in believing that the birth of this knowledge field, as we know it today, occurred in the second half of the 19th century, to meet the new control requirements resulting from the development generated by the industrial revolution.

The power awarded to the audit committee included in the Portuguese Commercial Code of 1888, represents an important milestone in company law, especially with regards to the preparation, issuing and control of the accounts of commercial companies. However, when the duties of auditing/supervision, were done by the shareholders, suggested a lack of concern for the requirement of independence, which today is considered the corner stone of this function. Supervision has always been done throughout the history of commerce and finance. From the middle ages, it was done to assure that the persons with financial responsibilities towards the government or commercial responsibilities towards the shareholders of the company, performed their duties with honesty and prepared trustworthy reports. The audit looked for frauds maintaining this function until the 20th century.

At the beginning of the 20th Century, the legal requirements11 advocated a new company auditing system, based on a structure named Bureau of Technical Supervision of limited companies, composed of expert accountants who had the duty to mediate and the power to decide on a variety of auditing issues of limited companies. They were therefore the modern version of the "Ouvidores" and of the "Vedores da Fazenda". This legislation created this new profession, and also two departments, one in the north and another in the south, divided by the Mondego river. However these two organizations were never legalized and therefore never operated although the government of the time had instituted industrial and commercial education, creating commercial institutes and higher education institutes of commerce, who had the function to teach their students, competencies adapted to the economic and commercial needs of the country,12 namely, to exercise the position of accounts commissioners in commercial and industrial companies.

In 1911, we witnessed a test for the emergence, amongst us, of Statutory Audit of Accounts, through Law Decree of 14 January (Carqueja, 1972, p. 121).

In 1936, the issue regarding auditing companies is once again discussed. We emphasize the requirement of independence and competence (Pessoa, 1986, p. 93) of the audit body and its potential staff. This required sworn specialized experts, with the aim to improve the efficiency of the auditing regulation of the companies.13 In 1943,14 we witnessed a new concern about the existing auditing system for shareholding companies, proposing that the audit be done by sworn experts who were part of a body, namely, Chamber of Auditors of Shareholding companies, and the intervention of the accounts court. The Auditors had to, in general terms, examine all the accounts and proof documents of the transactions done, check the assets and liabilities, check that the statutes and the law are adhered to exactly, and prepare the annual reports to inform the Chamber of Auditors of any serious irregularities or illicit actions found during the audit. The rotation of the auditors was advocated. This measure ensures that no auditor could audit the same company for a period exceeding five years. It was up to the Chamber of Auditors, to establish standard accounting rules, considering the specificities of each economic activity.

In 1943, through Law 1995, of 17 March 1943, we witnessed a new attempt to sketch, in Portugal, Audit of Accounts (Carqueja, 1972, p. 121).

The audit of the annual accounts of the commercial and industrial companies, in the first half of the 20th century, obeyed the philosophy of the period that in principle only the shareholders,15 present at the general meeting, could control how their capital was administered (Pimenta, 1972, p. 279). The lack of effective control, resulting from the lack of technical knowledge, or lack of independence, was common. This was generally discussed and of particular concern amongst the business circle. As a result of theoretical practical discussions in other countries, such as Italy, France and Germany, the need to establish a permanent body, of specialized accountants, which were not elected, by the administration or the general meeting, began to emerge in Portugal (Cardoso, 1976, p. 293-294).

In Portugal, in the 60's, just like in other more developed countries in practices of external control, we discussed whether an Audit Committee, in a more complex organization, made up of only experts in accounting and management, would be considered qualified to control the organization totally.

The basic issue of independence was also being discussed, recommending that the members of the auditors' committee would not be nominated by the general meeting or by the administration, but the only request representing organizations to create and regulate.

At the end of the 60's, it was considered urgent to improve the auditing of companies, because of the business volume in question, the rate of development of the economy and the expansion of public subscription of capital. The law stated that limited companies would have an internal audit department auditing the management. This would normally be an audit committee, or a single auditor, made up of three permanent members and one or two substitute members, or five permanent and two substitutes, which could or not be shareholders of the company. At least one of them and one of the substitutes had to be chosen from the listed statutory auditors "Revisores Oficias de Contas". This led to the emergence on 15 November 1969, by Law Decree 49348, of 15 November, promulgating the new legal system of company audit, as per previously described tests. (Noel Monteiro, 1975, p. 159; Castel-Branco, 1981, p. 383).

A new professional figure, emerges, who would necessarily be part of the audit department of the company, with adequate up to date technical knowledge and permanent unrestricted access to information of the various management actions and guaranteed objectivity to act independently. This state of affairs quickly generated controversy because of independence, by all those who favored that the statutory auditors should not be part of the company (Costa, 1994, p. 578-588).

The guidelines for auditing limited companies, at the end of the 60's, were as follows (Pimenta, 1972, p. 314-386):

— Experts appointed by the general meeting were the universally adopted solution, which was essentially auditing to protect the shareholders, who had the right to nominate these experts, at the general meeting, and these could in turn be assisted by staff;

— Discussion if the independence of the experts is assured, in spite of the experts being chosen at the general meeting;

— Discuss if the experts should be nominated from amongst shareholders, or because of the requirement of independence, the nomination should be done from amongst experts registered in an institute that is able to audit and observe a strict set of ethical and deontological standards;

— The solution of registering, in a professional body, with the underlying idea that the expert auditors had special professional awareness and professional dignity, enabling them to protect the interests of all shareholders, creditors and even the general public.

The technical knowledge, independence and critical thought, would be preserved through the statutes ruling the Portuguese Chartered Auditors. They are subject to a strict scheme of accountability and together with the administrators are responsible for their actions or omissions, in the case of not meeting their audit obligations.

The regulating of the profession16 was subject to a new norm, which in article 1, defined the scope of the audit. This included the audit of the accounts of commercial companies or any other entities, as part of the duties of the audit committee, or the single inspector and providing consultancy services in the scope of their expertise.

There was no exact ruling as to what should be understood by auditing of the accounts, the profession emerged but did not develop. In effect the Decree-law 1/72 of 3 January appeared to expect Chartered Auditors to merely to have an accounting role, namely the auditing the regular recording of accounts. This situation was never made clear. In 1974, the first general meeting took place. This was considered the year the profession was created. However, the revolution of April 1974, put the development of the profession on hold until 1979. In spite of this, a new work group was nominated to analyze the legal framework of the issue of auditing limited companies and of the auditors. The group made up mostly by auditors representing the Ministry of Justice, handed a report in June 1975, entitled "Revisão Oficial de Contas", where it was discussed if the profession should be freelance — therefore independent or State dependent, that is, public officer. As the environment at the time was revolutionary, characterized by successive nationalization of companies, the work group proposed the creation of a public audit body to audit companies, as a substitution of the recent professional organization of Chartered auditors "Câmara dos ROC's". This was based on the fact that the private sector of the economy was merely residual and the State had the economic control of the productive wealth base. It was expected that the Chartered Auditor to be an expert in matters of management, economics, law, accountancy, sociology and labor science. This resulted in great controversy because it permitted law graduates to audit accounts (Monteiro, 1975, p. 166; Fernandes Ferreira, 1972, p. 364-367).

This report did not become law. On 10 November 1975, another work group was formed. Who based on the experience of some European countries, studied the "Issue of the Charted Auditors" favoring a defined scope of the statutory accounts audit, limited to analyzing the accounting records, and highlighting the need to follow the practice of accessing the accounting operations by an independent professional who assured reliability of the financial statements. This study, also favored, non inclusion of the chartered auditor in the audit committee, highlighting, however, the exercise of the activity in an autonomous and independent manner.

On the other hand, the audit committee had the duty to supervise the management in its total aspects.

On the 15th of May 1976, a team was appointed to prepare the project law on the auditing of companies. The audit function was conceived as a mechanism of external control, completely independent of the entity supervised, that is, without any kind of hierarchical subordination or economic dependence of the controlled company in relation to the controller. The authors based their doctrine on the already mentioned theory of trust, which established that the annual accounts should reflect the clarity and honesty in the management entrusted to the administrators.

The statutory auditing of accounts, according to the philosophy of the group, was an adequate report to show an assessment of how the legal and social statute standards were met.

Simultaneously, although in a slight manner, the autonomy of the committee in the preparation of the auditing standards, which would be approved and promulgated by the government, was considered. It was accepted that the auditors, considering the economic environment, should not be freelancers, but rather employees of a public entity of chartered auditors, legally and financially autonomous, employing all the practicing auditors in the country.

The previous theory did not succeed, and in 1979, the statutes giving the chartered auditors the required guarantee of independence from those entities they audited, were approved. This increased the efficiency of auditing and defined a level of professionalism and accountability in line with the responsibility of the chartered auditors (Oliveira, 1981, p. 433-452).17 In general terms, this duty, "the auditing of accounts of companies or any other entities, as per statutes", considered that auditors exercised a function of public interest. The most important aspects are stated in the manual of the duties of the chartered auditor in the scope of the Audit Committee. (Silvão, 1979, p. 127):

— Awarding the Chamber of charted auditors the authority in all matters regarding internships and examination of candidate auditors;

— Clarifying and broadening the scope of the activity of the auditors.

Significant changes occurred meanwhile, in the legal system and in the economic environment. The constitutional revision of 1989 establishes public associations, and in particular the Chamber of chartered auditors, as a public entity with an indirect responsibility of administration, that is giving legal power to a professional organization, entrusting them to regulate and exercise an activity of public interest. On the other hand in 1986, Portugal joined the EEC, which implied adapting the Code of Commercial Companies, to the Community legal framework. This extended the scope of work of the auditor, covering various areas reflecting the legal system, and at the same time there were great changes in the legislation of the capital markets.

As a result, a new standard emerged.18 Article 1, awards the Chamber of chartered auditors the status of a public entity. It had financial and administrative autonomy and the power to decide on all aspects related to the profession and with the authority to represent the auditors and the audit companies.

In 1999, in consequence of the significant changes in the internal legal system and in community law, such as the changes in commercial and capital markets law, a new decree19 emerged, aimed at harmonizing the legal system of the audit companies, with the dominant situations and tendencies in the European Union, keeping its social nature, adding flexibility to its legal aspects and improving its technical and administrative capabilities.

The said law acknowledges "the increasing relevance of the role of the auditor in safeguarding the public interest, credibility in auditing of company and other entity accounts, the acceptance of the public professional association20 covering everything in respect of the activity of revising accounts, being it legal, statutory or contractual, were subject to the normative discipline and the control of the charter. In Portugal, all external audit activity is under the jurisdiction of the Chamber of chartered auditors, who must register under the approved legislation and are subject to the following requirements:

— The requirement of an adequate degree as a minimum qualification to be admitted to the profession.

— Changes to the process of admission to the profession.

— Extending the scope of subjection to audit of accounts.

Statutory auditing has developed, very slowly, over a period of approximately 25 years. However, after Portugal joined the EEC, the evolution has been steady and constantly adapting to the European legal framework. Presently the mercantile law and the accounting information system, are perfectly in line with community directives on this issue — 4th, 7th and 8th directives — in such a way that Portugal is on the same level as the other European Union countries regarding to training, assessing, auditing and reporting of annual accounts of companies and company groups (Afonso, 1981, p. 401-404).

The Chamber of chartered auditors, as a legal entity takes on the responsibility to regulate auditing in Portugal in the broadest sense, advocating both the discipline and the total control of auditing. We have therefore a mixed regulation model of auditing, whereas together with a public provision of guidance, it is also the duty of the professional body of Chartered Auditors, delegated by the government, to stipulate the conditions for registering, prepare and review technical norms and control the quality of auditing.

Government gazette No. 24 of 20 November, in 2008, reflects the changes that resulted from transposing to the internal legal system Directive No. 2006/432/CE of the European parliament. This dealt with the statutory annual auditing of consolidated accounts, stressing on a community base, the quality of the chartered auditors, their independence, integrity and objectivity, in the preparation and presentation of a transparent report, as well as reinforcing quality control through the creation of a new surveillance model, instituted by the National Chamber of Auditing Supervision (CNSA — DL 225/2008 of 20 November). These new statutes reinforce the ethical and deontological powers of the development of a profession of public interest. It confirms the need to apply the international auditing norms, and chooses training as a priority, to achieve in the national legal system, a reinforcement of the harmonization both on a technical and an institutional level. This new framework is also considered an answer to the criticism leveled at statutory auditing, because it does not provide reasonable certainty regarding the corrections of the financial statements (Marques de Almeida, 2002, p. 408).

4. The Chartered Auditing services in Portugal

4.1. The nature of the market

The nature of the audit services in Portugal, in spite of some particularities,21 is not very different from the auditing services market in other community countries. According to the methodology of Moizer (1992, p. 333-348), in theoretical terms, the market is characterized by the following aspects:

— Assessing the quality of an audit is extremely difficult. It requires access to the planning documents of the auditor and knowledge of the control system and the financial and commercial risks of the clients. In spite of this being a service market, unlike the majority of other services, it is very difficult to make an assessment ex ante.

— The second important aspect of the auditing services is related with the problem of independence of the auditors in respect of the customer company. In Portugal, the auditors, are generally employed and dismissed by the customer company, and the intervention of the shareholders is minimal. Therefore the independence of the auditor is threatened by various factors, such as the length of the contract, the concentration of the profits, etc. In Portugal there is no rotation of auditors, publication of remuneration (with the exception of listed companies), these are solutions, often said to preserve the independence of the auditor.

— One of the characteristics of the market is that it is a professional monopoly. It has a strong professional structure, and therefore, it is in the interest of the organization that governs the profession to maintain the "self-regulation monopoly" and avoid government interference. This is the case of the Portuguese Chamber of chartered auditors. A peculiar aspect is the fact that the remuneration was set administratively. However at the moment Chamber of chartered auditors continues to recommend the adoption of the fee scale.

4.2. Collection of data

The methodology applied to the study of the concentration of the Portuguese audit market:

— The Portuguese legislation does not force the statutory auditor to declare the volume of operations and the respective payments. Therefore to analyze the competition in the auditing market, we use the indirect indicator of the point distribution per auditor — the non listed companies — is the number of audits carried out — listed companies—. These were the chosen variables, like in the empirical studies mentioned in the introduction.

— The concentration measures which are normally used in the empirical studies of this nature are indices of concentration in the order n, that is, the sum of the market share of the biggest companies in the market.

— The index 1, shows that the market is totally controlled by a single auditing company. While the = indicates the minimum concentration.

— After describing the variables, the following objective is to induce in quantitative terms, the level of activity of the statutory auditors, by selecting the number of companies who submitted their accounts to statutory auditing.

— This study naturally has its limitations, especially in the case of non listed companies, where the number of points was used, naturally the viewpoint of the explanatory variable.

4.3. The structure of the demand

In Portugal, all limited companies, shareholding companies and other entities — e.g. co-operatives — that in terms of assets, own capital and number of workers corresponds to the minimum requirements for limited companies, are subject to statutory auditing.22 Requesting an audit is a legal requirement, there is strict regulation that masks the motive of the request as well as the attributes of the users that request this service (Benau & Martinez, 1998, p. 29).

4.3.1. Societies with shares listed in the market regulated since 200423

In the graphs below we can see the distribution of the companies with shares listed on the stock market24 in a market regulated by the auditing companies (Figures 1-5).

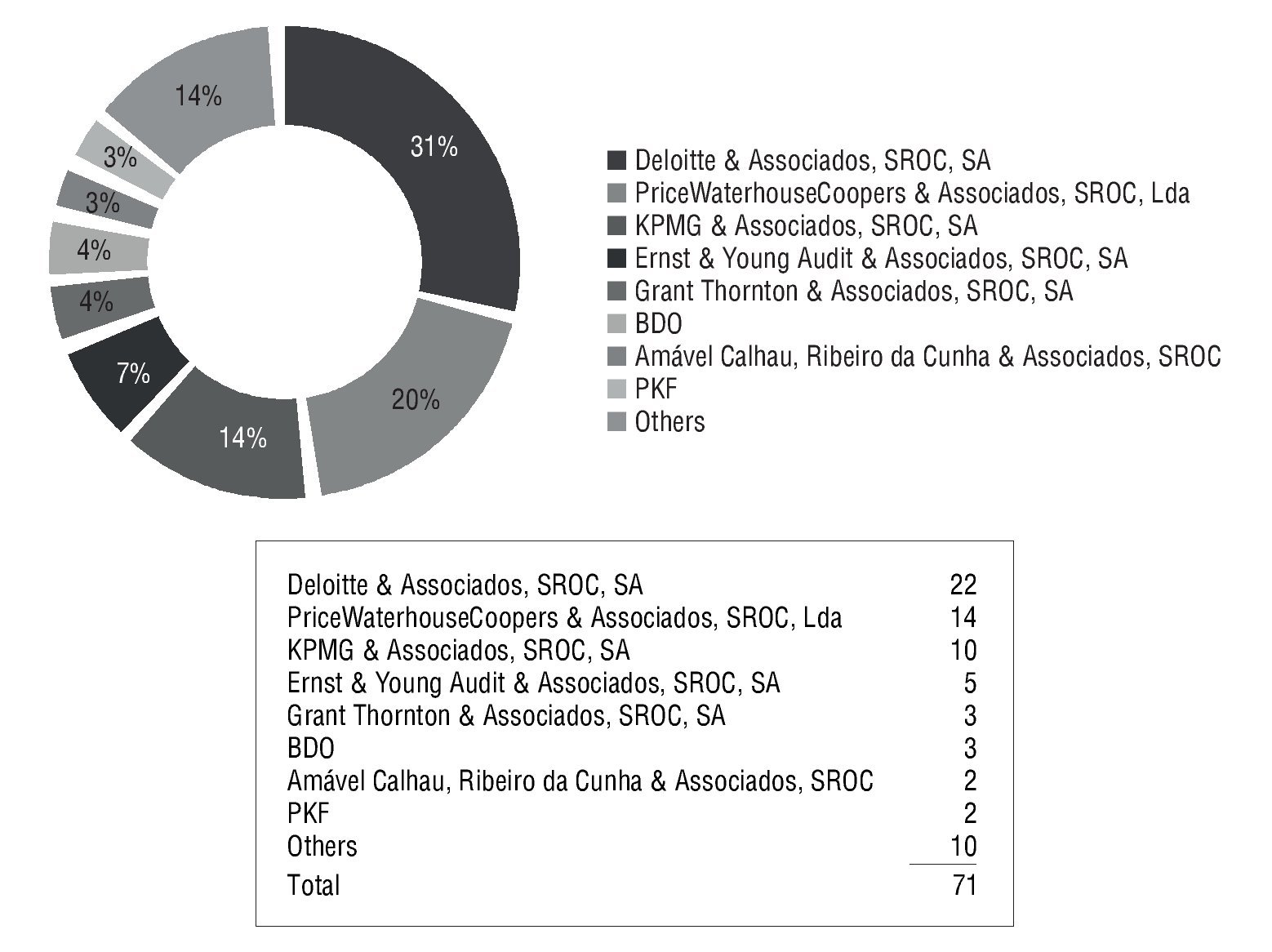

Figure 1 Distribution of the "SROC's" (Society statutory auditors) by activity sector.

Figure 2 Statutory audit in the financial sector.

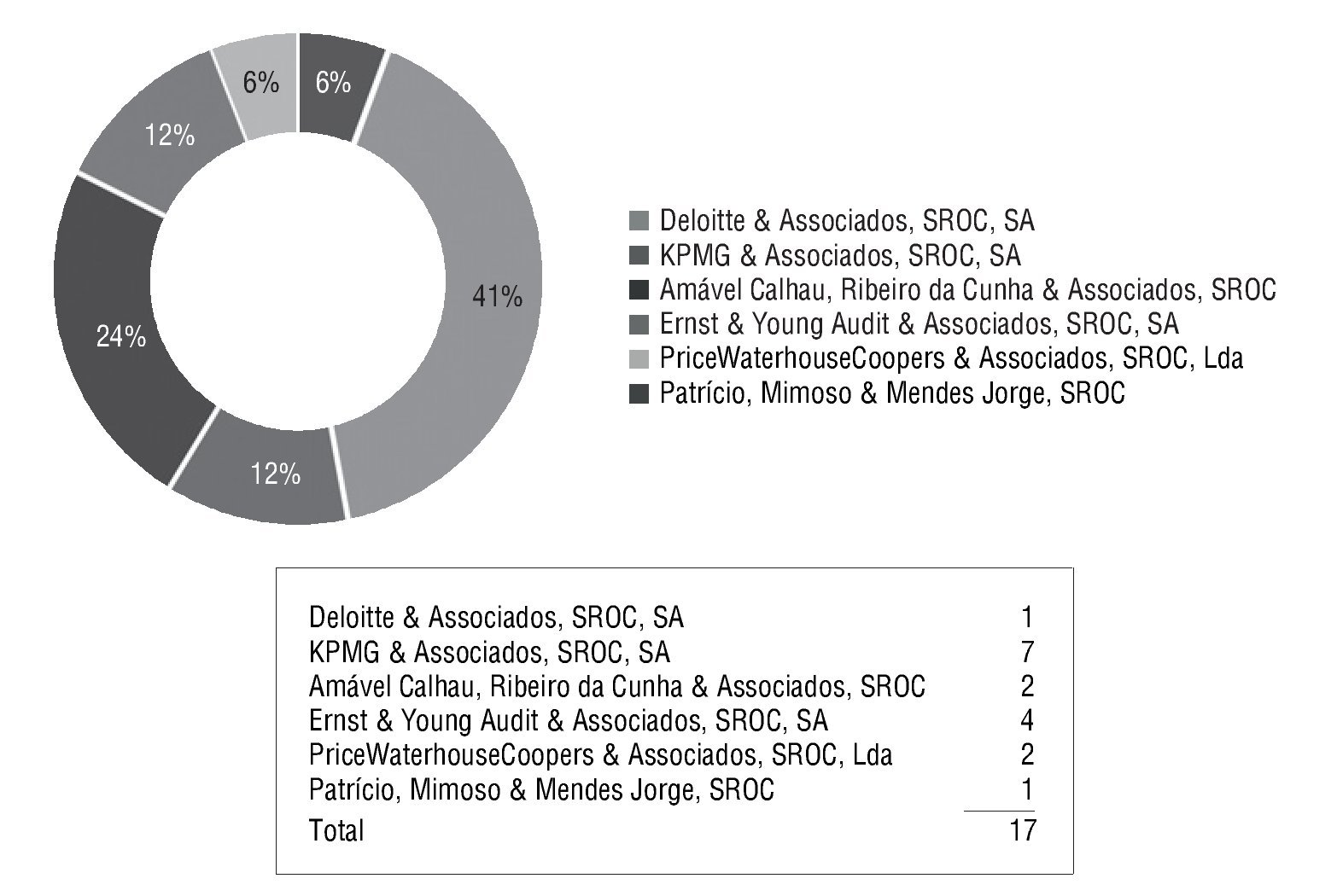

Figure 3 Statutory auditing in the industrial sector.

Figure 4 Statutory auditing to the consumer services sector.

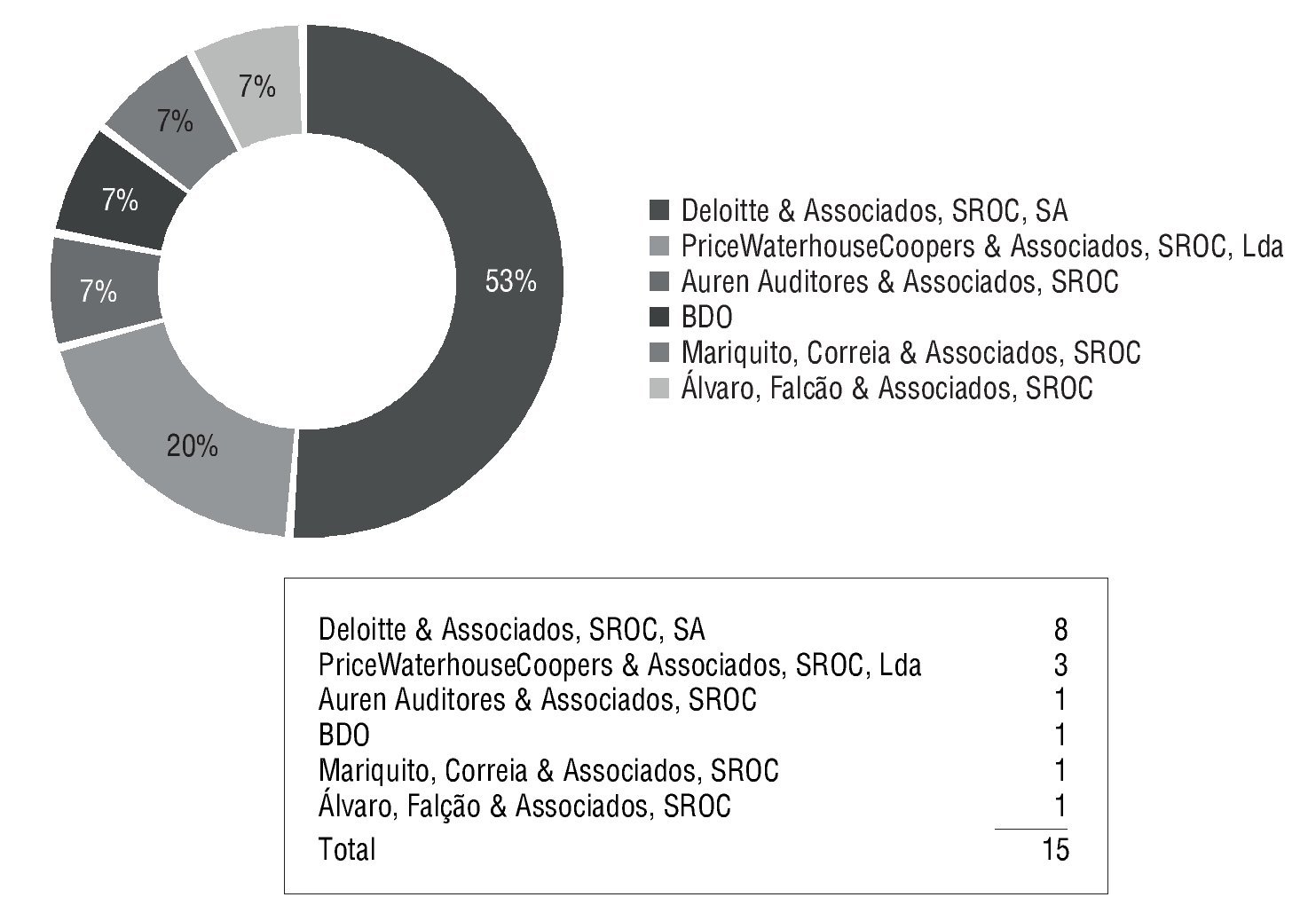

Figure 5 Statutory auditing in the remaining sectors.

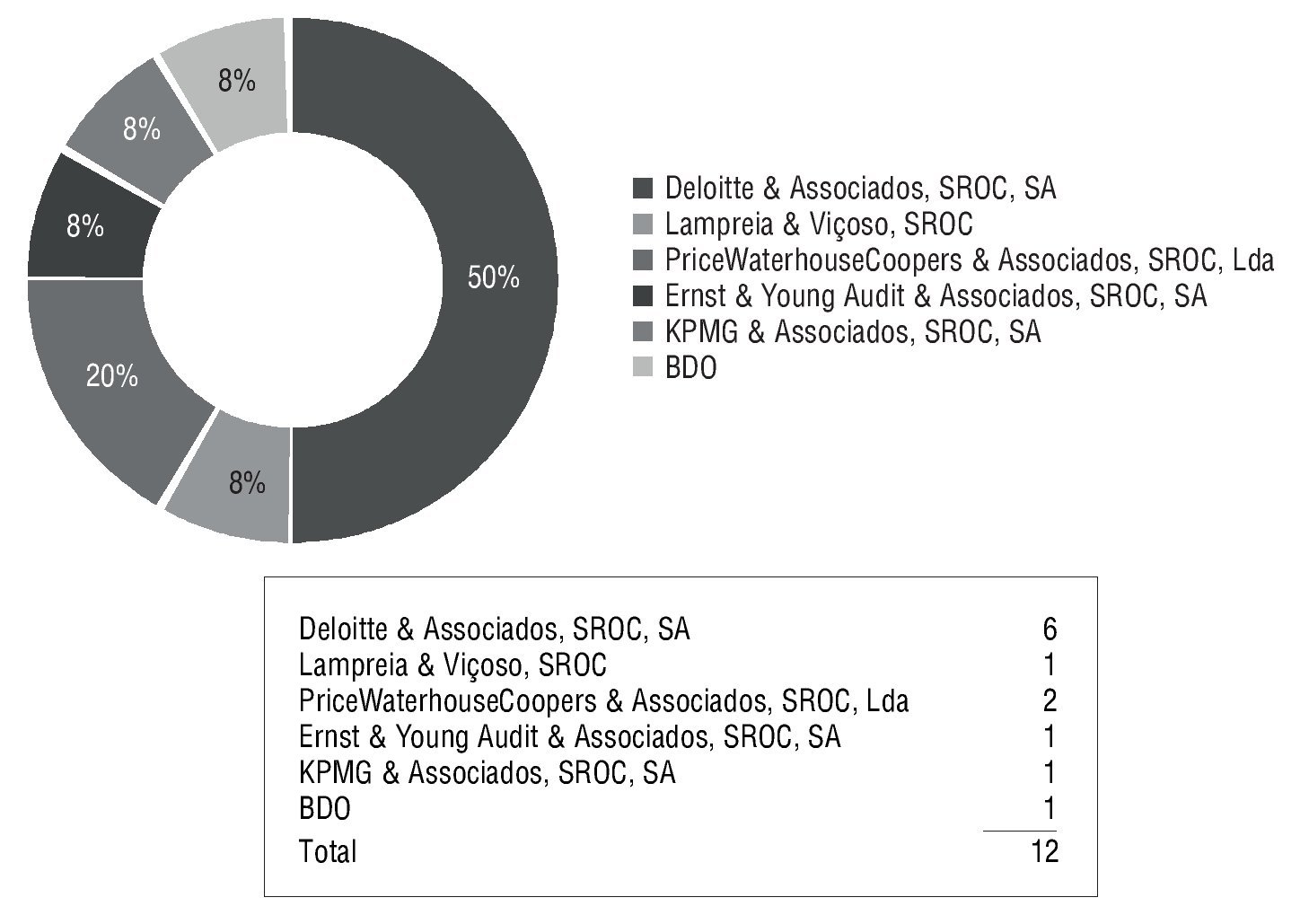

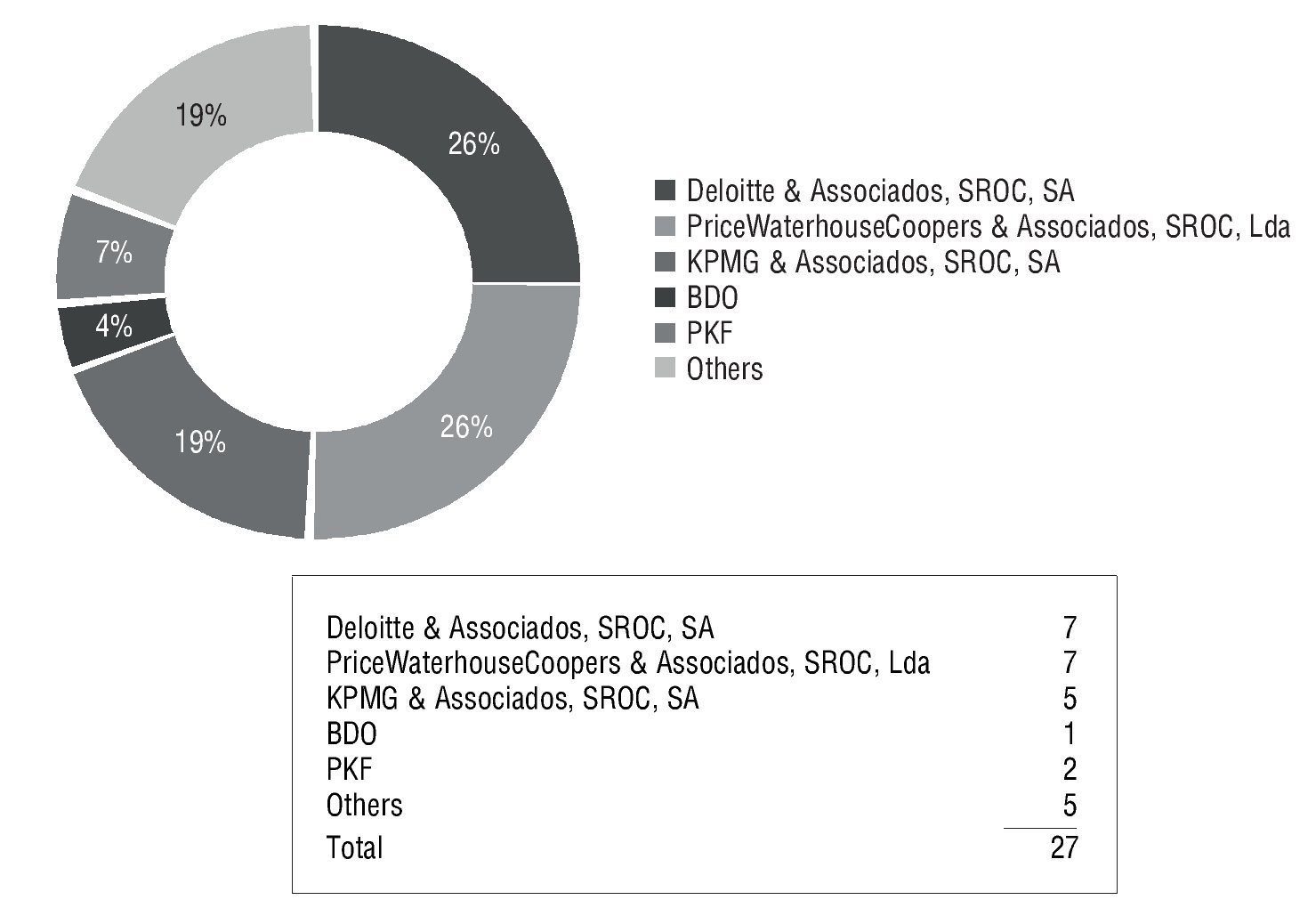

In Portugal, of the 71 listed companies on the stock market, 51 were audited by auditors connected to the four biggest international audit companies. Deloitte & Associates, auditors society, legally certified the accounts of 22 enterprises in a universe of 71 which corresponds to about 31% in total. The bigger international audit companies with the largest portfolio audited about 72% of the listed companies. In effect, the market share of those companies, in Portugal, shows the same tendency as detected by Marten (1997), and in the case of Germany, by Beattie & Fearnley (1994), for the United Kingdom, by Maijoor et al. (1995), and in the case of Holland and Benau & Martinez et al.(1998) in Spain.

The explanation for this situation is essentially based in the increasing internationalization of the Portuguese economy favoring societies well placed worldwide with a strong image and credibility, which act as a barrier preventing the national offer to enter the market.

When detaching the analysis in the case of the various sectors — finance, industrial, services and remaining sectors — it was also found that Deloitte & Associates, audits the majority of the companies, with the exception of the financial sector, where the predominant company is KPMG, auditing 7 societies of this sector. In global terms, in the financial sector, the international companies dominate. They have 94% of the market share. The same is shown in the industrial sector where Deloitte and PWC, lead with 73% of the market share. In the remaining sectors the panorama is similar.

As in the case of Spain (Benau & Martinez, 1998, p. 117) we found an uneven market structure, with competitor characteristics very similar to oligopoly. The provision of audit services for listed companies in the regulated market, makes the registration of that organization compulsory in the Security Exchange Commission (CMVM), which is another entry barrier, showing that not all suppliers are in the same situation regarding the market share they have. Considering that the chosen period by the auditors for these companies is generally three years, we see a stable market share. Furthermore, it is accepted that the competitor's behavior or the typical behavior of the oligopoly market, can operate in Portugal, especially the latter which can lead to agreements so that the exogenous oligopoly competition cannot occur. This war or understanding was checked on the level of the audit market by Dopuch & Simunic (1980) who suggested that the international audit companies may enter into explicit or implicit agreements: in Portugal the audit companies that examine the accounts of the listed societies, and are not international audit companies leave the initiative to the producers of oligopoly audits and adapt to the market environment.

One possible explanation for this concentration resides in the economic and social dimension of the companies with listed shares, as well as the complexity of the transactions and of the organizational structures that rule them. These are not compatible with the structure of the services offered by the national audit societies, who generally have small technical and human resources, whereas the abovementioned companies tend to look for more specialized auditors.

Like Spain and other countries (Benau & Martinez, 1998, p. 133) it is highly unlikely that the national audit societies or the independent auditors compete in the listed companies market. It is also noted as per Dopuch & Simunic (1980, p. 113)25 that the smaller the company is the lower probability of hiring an international audit company.

Choosing an auditor, in the audit choice mechanism, in Portugal, in the case of the required statutory auditing can be explained by the theory of homogeneity of the audit service emphasizing price as the explicative variable. However the theories about service differences, where quality is a factor, can be important in Portugal, especially in case of listed companies as these have the highest agency costs, as their capital is dispersed needing therefore a better quality audit. In smaller companies the choosing process is based on the reputation of the auditor has in the national or regional market, the social network he is in and verbal publicity made by other clients. The probability of searching in the official list is unlikely or not at all. The reputation and the social image are determinant factors.

4.3.2. Total number of companies subject to statutory audit of accounts

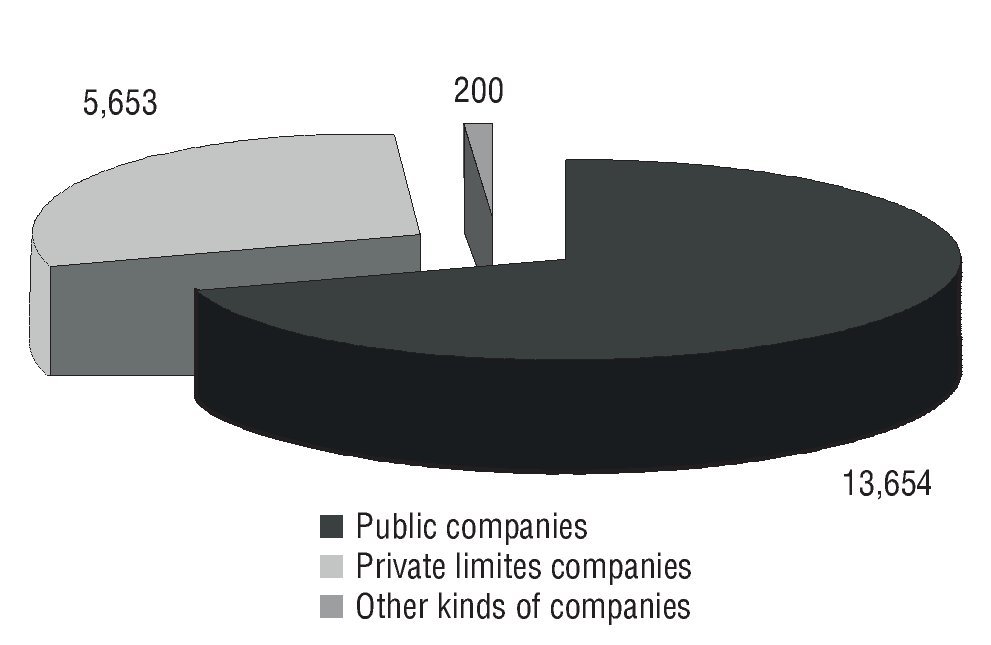

Over the four years analyzed, the average number of companies subject to legal audit of accounts, according to data furnished by the Chamber of chattered auditors, is 19,507. On the same date the National Institute of Statistics, had registered 13,654 companies of which 71 had been admitted to share market. We conclude that the rest were divided into companies limited by shares and other kind of companies: co-operatives, EIRL,26 etc., with the latter being considered residual in our study. See Figure 6 and Table 2.

Figure 6 Entities subject to Statutory audit of accounts.

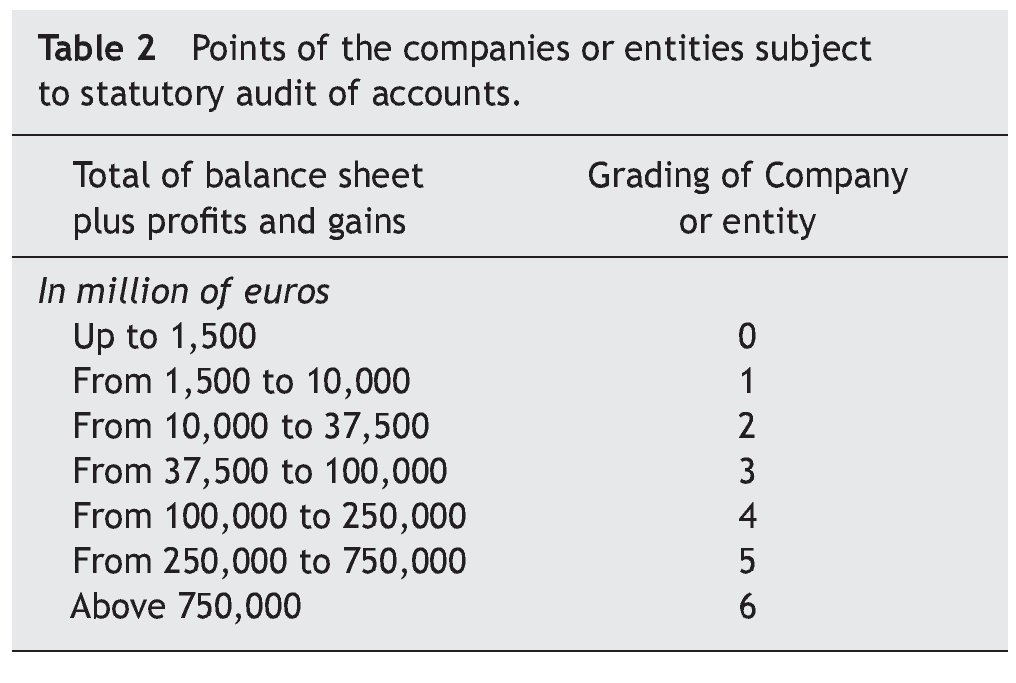

This table of points which is applied to the listed and non listed companies shows the specific incompatibilities that in practice limit the number of companies that each auditor may certify as audited.

In fact, each auditor could not audit for legal, statutory or contractual reasons, on long term a number of companies or other entities if the points awarded exceed 36 points, calculated according with the table above.

On the other hand the constitution of societies is promoted by increasing the limit for the auditors societies, multiplying the number of certified auditor members by 1,3 and so the regime of exclusivity permitted that the ponderation factor to be 1,5. This limited the exercise of the auditor's activity, in the case of those who did not exercise their profession in exclusivity.

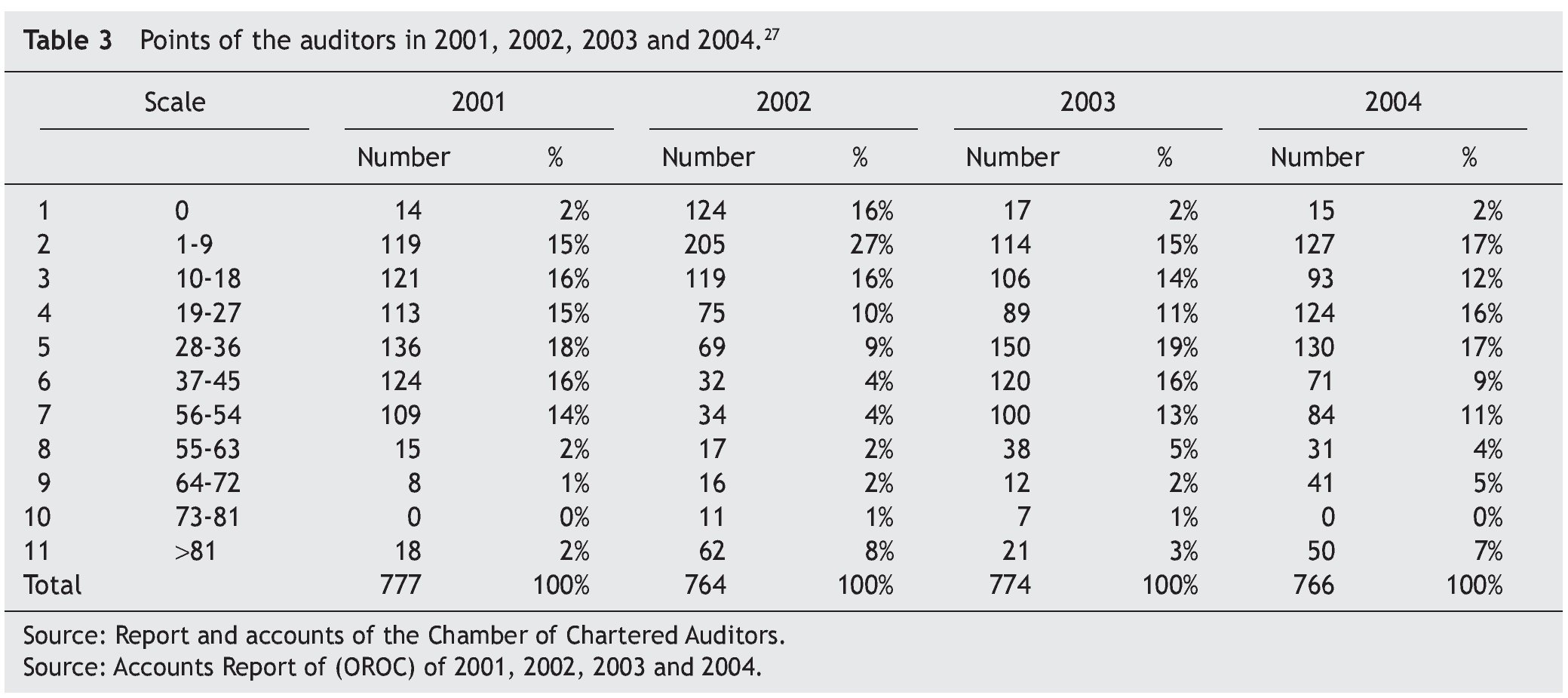

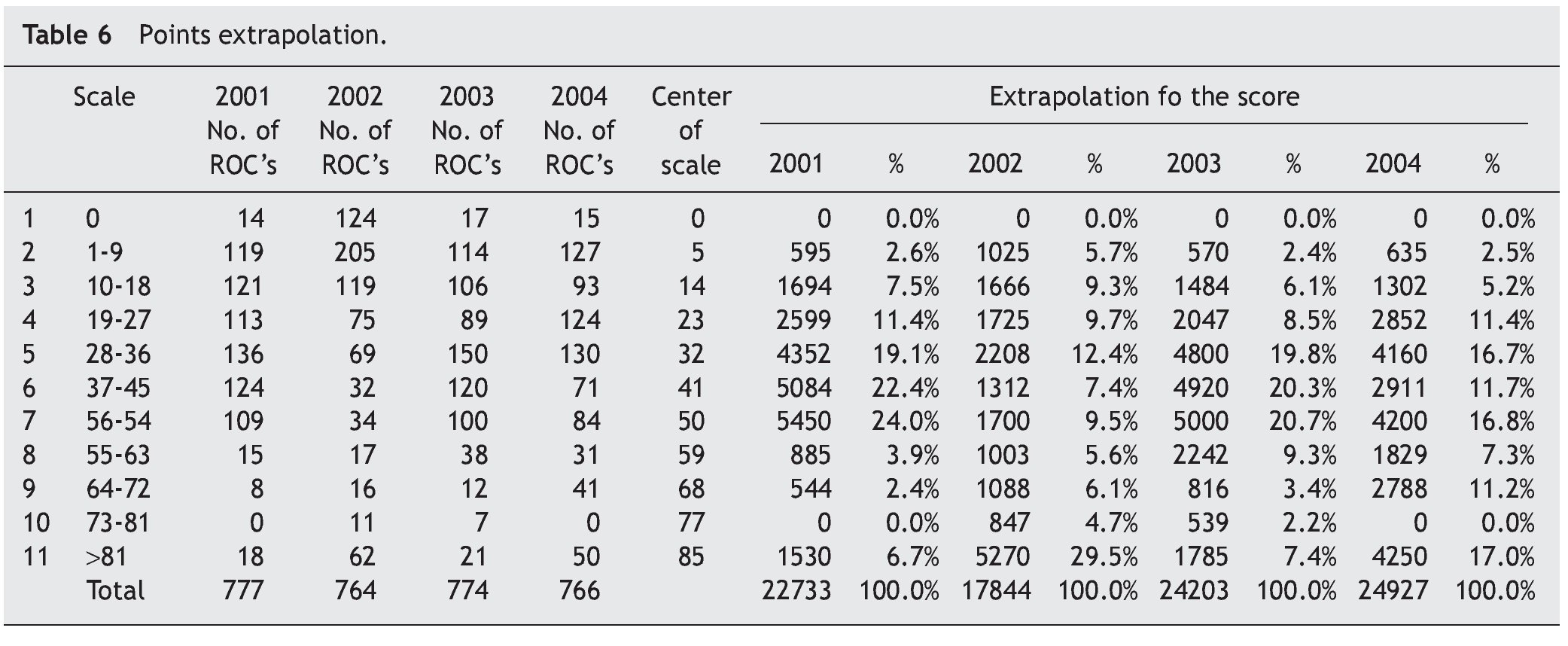

This practice gave rise to some collateral effects. It permitted on one hand, that some auditors "sold" their quotas to other auditors in exchange for financial gain, in order to remain inactive or not to leave the main activity they had — an adverse effect. On the other hand it permitted the sharing out of all the quotas amongst almost all auditors registered in the Chamber — positive effect — although the big enterprises generally were in the client list of the international audit firms. These did at the same time, both the audit and the statutory audit, stating that they provided two services for the price of one. The registration of new auditors in the Chamber in the 90's and beginning of the 21st Century was made extremely difficult by an entrance exam. The market demand was aimed generally at auditors with available quotas, even if the service quality was not compatible with the remuneration paid. In the year 2004 we had the following distribution, in quantitative quotas (for the study we considered 11 scales, considering what is described on footnote No. 28) (Table 3).

The number of active auditors in 2004 was lower than in the year 2001, which means that in the four years under study, due to the barred entry, no new members were admitted to compensate for the members that had left, increasing the number of non active auditors. We witness some in and out movement in the scales, the number of auditors with a nil grading reached its highest in 2004 the same as in 2001, about 2% of all the active auditors. The seventh bracket, in accumulated terms, is a strong mark, because it represents in 2001, 95% of the total number of active auditors and in 2004, the numbers accumulated of the said bracket still represent 84%. It means that during the period under study there was a sharing evenly of the companies with a residual number of elements with over 55 points.

It is necessary to explain, in terms of activity, the existence of auditors with a zero points. This did not mean that they do not audit companies. From Table 2, we found that when the audited societies, show a total assets, plus profits and income lower than 1,500,000€ they do not have a score. In Portugal a great number of societies pay a minimum or slightly above remuneration and therefore do not count for a score in the client list of the auditors. The above table shows a distribution of the societies subject to statutory audit by professionals, geographically spread over the country. The issue of the proximity, in Portugal, as well as the reduced dimension of the companies and their location on the coast line and the interior, are possible reasons to explain the sharing of these companies by 766 registered active auditors. We suspect also that the companies see the profession more as an instrument of planning and tax consultancy, than a mechanism of control and accreditation of financial information furnished to the various shareholders.

This shows that auditing and the relationship of accountability are connected with the economic, social and cultural development of the society where the auditing takes place. Portugal was until 1975 a dictatorship, where the economic levels were very reduced, with a delayed industrial revolution in relation to the majority of other countries. With a strong resistance to the enforcement of legal audit, an activity started in 1974 with the many changes in the process of development. In this context the auditing offer was administratively regulated. This regulation was the duty of the Chamber of chartered auditors, providing an apparent balance in the distribution of companies by a Professional body dispersed over the country.

4.4. Statutory Audit Services offer

4.4.1. The structure of the offer

In Portugal, the auditors have the exclusive competencies of the following functions of public interest:

— Statutory audit of accounts, when resulting from legal orders.

— Auditing of accounts when resulting from statutory or contractual orders.

— Services related with the previous points, or with a specific aim or with a specific or limited scope.

— The exercise of any other duty when the law requires the services and independence of an auditor.

The exercise of these duties implies the compulsory registration in the Chamber of chartered auditors, after a long training process made up of 4 written exams on issues related with law, taxation, financial accounting and management accounting, amongst others, culminating with a compulsory oral exam on the acquired knowledge. This was followed by a three year internship, successfully completed in order to register with the Chamber of auditors.

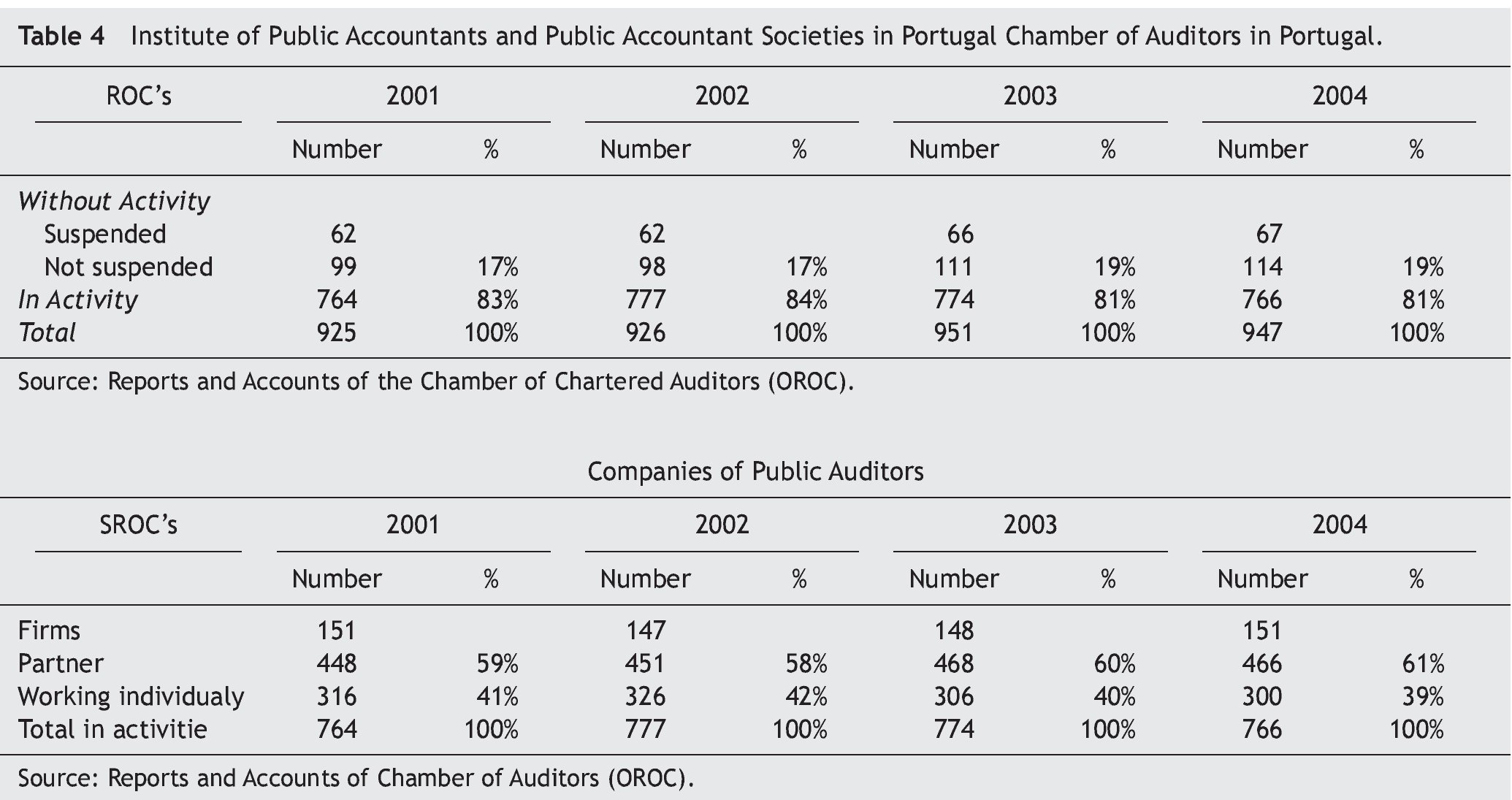

The following tables (Tables 4 and 5) show the number professionals qualified by the Chamber to exercise their profession:

The structure of the auditing offer in the Portuguese market, considering the reduced number of Portuguese companies listed in the stock market and the small size of the Portuguese companies in comparison to other in the European stock markets, still permits the co-existence of auditing companies and public auditors working individually. There is however a strong movement for individual public auditors to join the existing auditing companies or European auditing networks.

We understand from the reports of the Institute a decrease of 8 active auditors from 2003 to 2004. The total number of auditors registered in the Chamber also decreased as well as the auditor members that were part of societies. One of the possible explanations for this was the actual registration process, the very long time delay between the enrolment for the examination and the final registration (about 5 years). This may result in an "apparent" decrease in the number of statutory auditors.

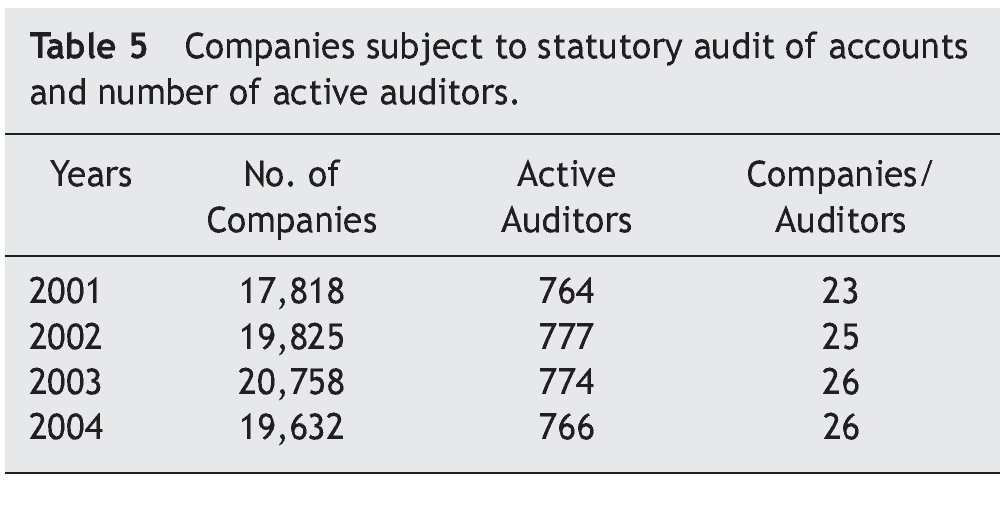

Below (Table 5) is the number of companies according to the records of the Chamber of auditors:

On the table (Table 5) above and based on the year 2001, we found that the number of companies subject to statutory audit, had increased by 10%. On the other hand the number of auditors remained the same, there were two more auditors. This resulted on average more work for each auditor, although unequally distributed.

We found that this activity occurred increasingly more within societies of professionals. The number of auditors working freelance decreased over the four years under study. The reason for this tendency resulted from volume pricing resulting from auditing companies.

5. Analysis of the concentration of the statutory audit market in Portugal

The international literature mentioned, points out that to adequately classify the nature of the market, we should focus on the analysis of the concentration of the market.

Thus, we study the level of concentration inherent to the unlisted companies and in the case of the listed companies, using three measures of concentration analysis28: Gini Index, Lorenz Curve and the Herfindahl Index. These indices take into consideration all the Auditors (ROC) (in the case of listed companies) and all the audit companies (in the case of companies with negotiated shares) and shared the work amongst the auditing services.

5.1. Analysis of the concentration in relationship to the non listed companies

5.1.1. Linear Extrapolation and main tendency measures

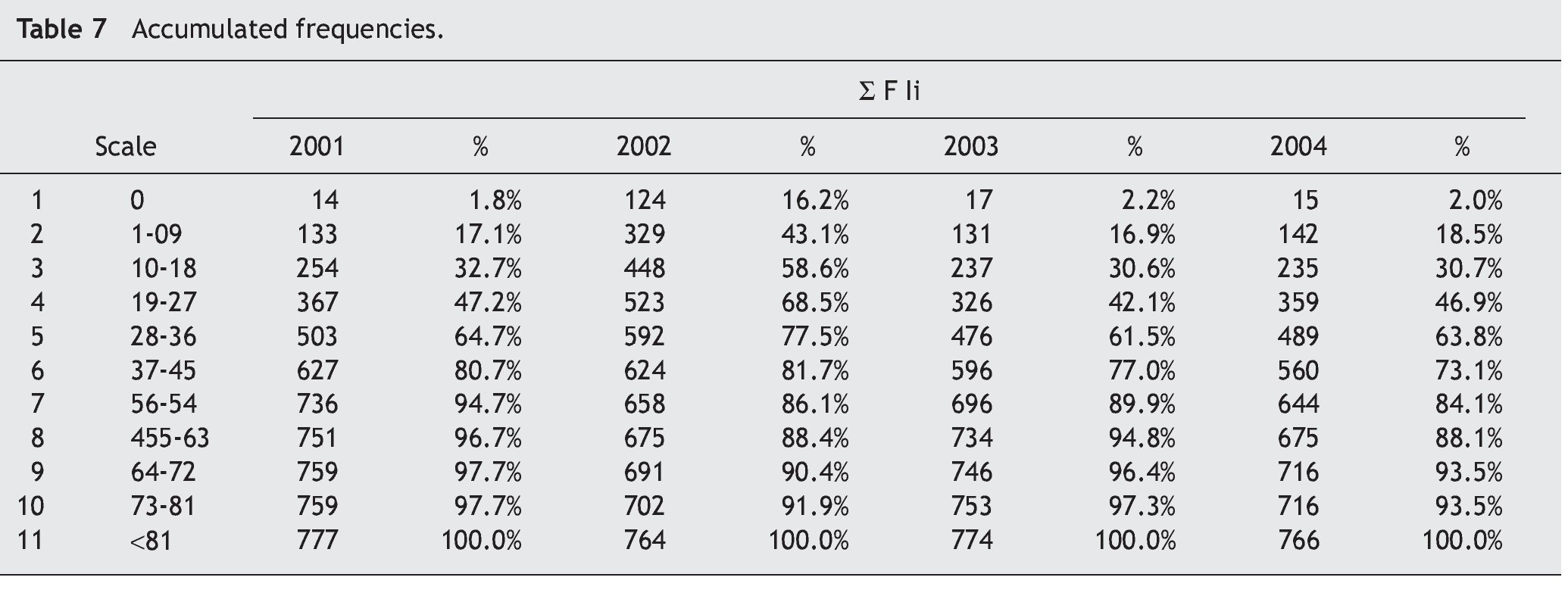

Due to the fact that the database of the Chamber of chartered auditors does not provide information by sector of the audited economic activity, we will analyze the activity reports referring to the years 2001, 2002, 2003 and 2004, regarding the "Evolution of the professional activity". The report, as stated previously, shows the points awarded by scales, as well as the number of professionals within each scale. As mentioned before the remuneration was fi xed administratively, based on the set legal minimum, which is the negotiating basis for all the professionals registered in the Chamber. All the scales have an interval of 9, and all active auditors are counted in each case. Using the average of each scale, assuming that the frequency is distributed evenly in each class, we proceed with the points extrapolation for each scale. For the last scale that has no upper limit, we accept similar amplitude to previous scales. We conclude the total number of points for all active professionals auditing accounts in Portugal (Table 6).

The development of the professional activity, over the four years under study measured in terms of quota, shows stagnation, considering a small increase of 6,5% from 2001 to 2004. By this situation we concluded that the market of legal auditing at the time was stabilized, both in terms of offer and demand. Therefore the number of entities be it freelance or belonging to a society exercising the activity have decreased by four auditors due to the joint effect of admitting eight new members and twelve withdrawals due to cancellations or death. Regarding the company structures, these are mainly small and medium size companies family owned, for which statutory auditing could be considered as excessive. In spite of the majority being legal companies, the majority of the funds obtained to finance their substitution or expansion investments are from their own resources or financed traditionally and not by canvassing public share capital attracting the participation of small shareholders. The relationship of agency as a general explanation for auditing is not generally applicable to this business world.

On the level of internal mobility dynamics between scales, we note that in spite of the number of active auditors having decreased, we found some movement within the scales, showing a considerable increase in the higher scales, which shows some concentration of the activity of the auditors who have a large client list, as seen in scale C9 and C11, and the lower scales C2 and C4, usually, filled by young auditors looking for a place in the market.

Analyzing the accumulated frequency regarding the first extrapolation table considered above (Table 7).

We found in the analysis of the period, over half of the professionals registered in the Institute, have a grade below 36. The table also shows a transfer of auditors to the last scales, as pointed out previously.

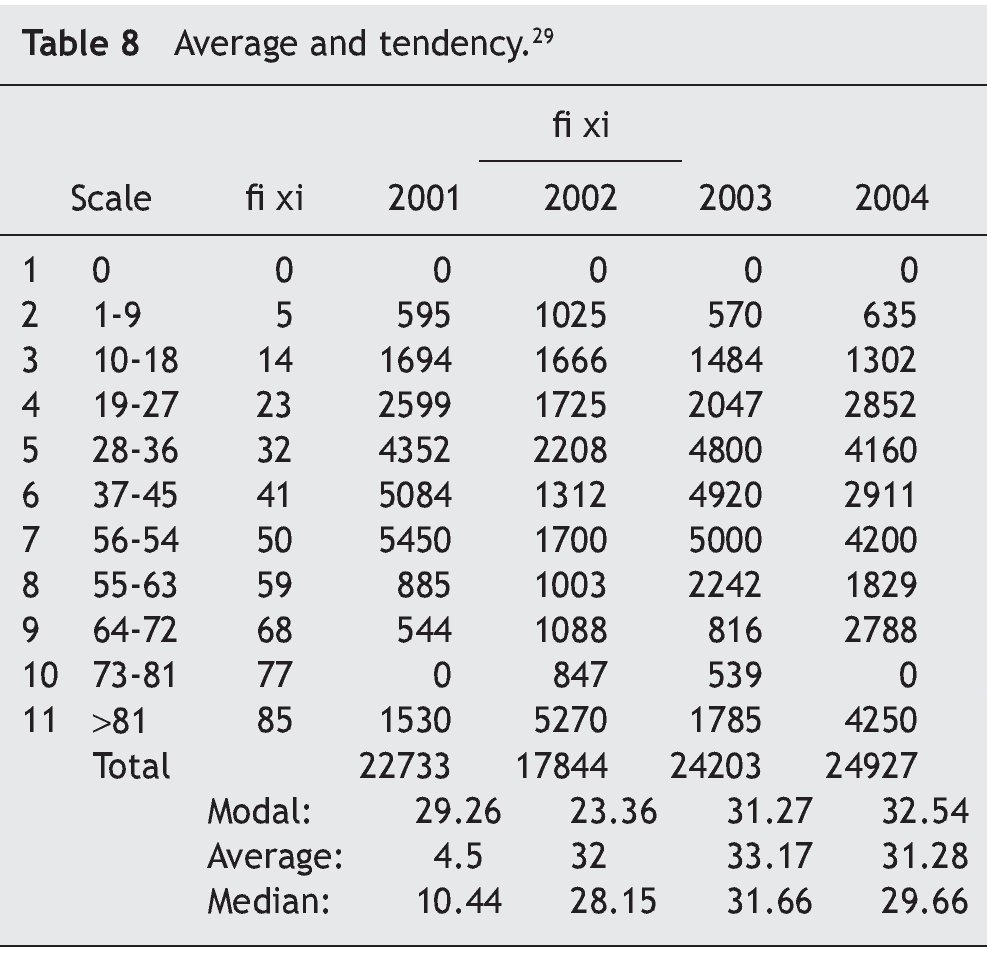

Applying to the previous table the descriptive measures of the central tendency — average and tendency — we arrived at the following amounts (Table 8).

The measures of the central tendency, referring to the four years analyzed suggest that auditors, on average, contacted more auditing services, increasing therefore their group of clients and consequently their remuneration.

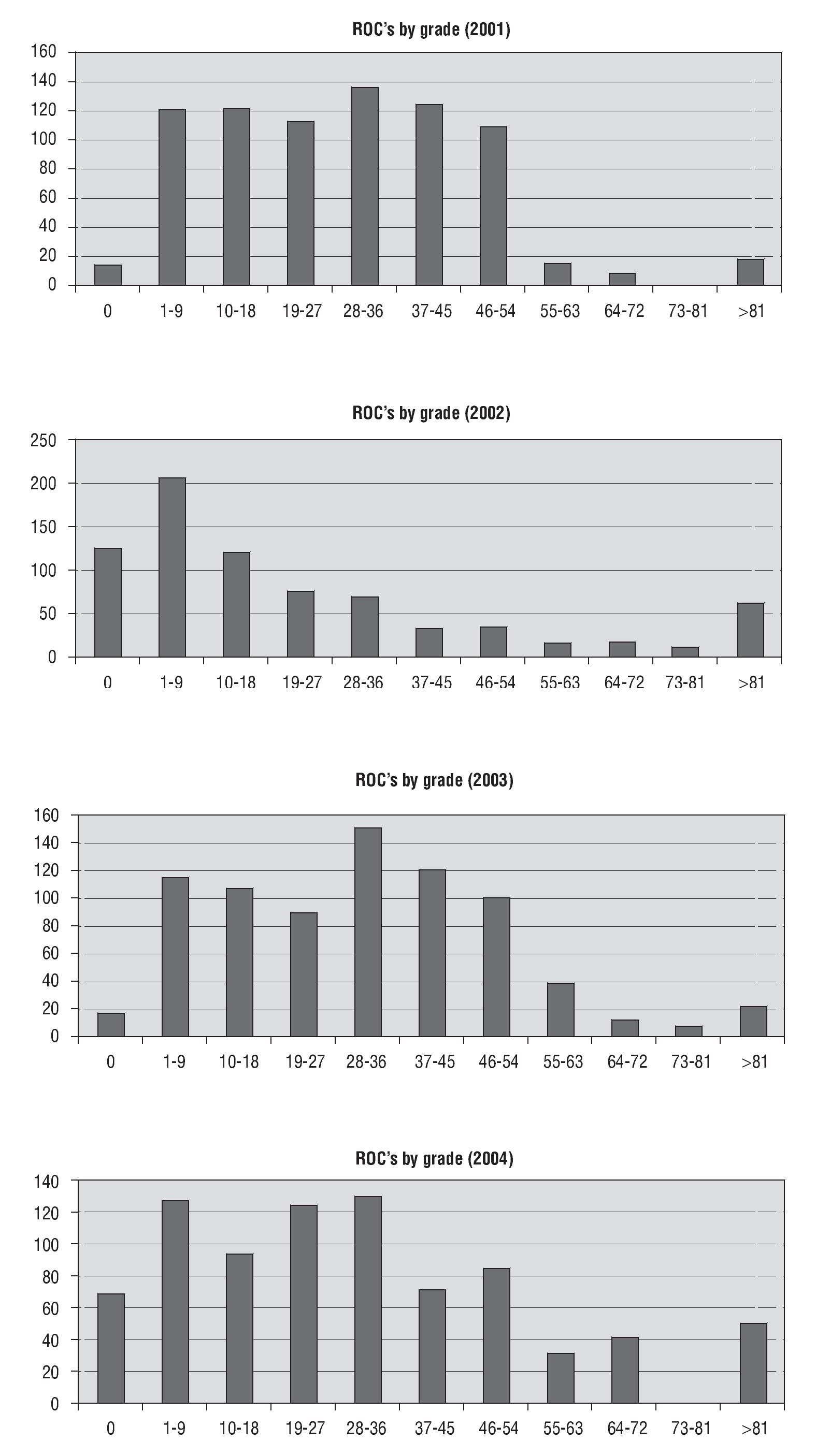

It is therefore clear the variable value observed, that is the modal class, in the year 2001 is of the order 3, which means that the majority of auditors worked with a grade between 10 and 18. However in the year 2002, the majority of auditors worked with a reduced number of companies, considering that the modal class is of the 5th degree. In the years that follow the modal class once again moved is also the 5th, which means that a greater number of auditors worked with companies representing between 28 and 36 points (Figure 7).

Figure 7 Distribution of statutory auditors by grade.

We have a symmetrical distribution when the average is the same as the most frequent and the median, and is represented by a normal curve or a curve in the shape of a bell. In the case of the slope the figure suggests asymmetry of the distribution.

The distribution of the grades by the active auditors is heterogeneous, in the four years in question, showing a decrease in basically all levels of grading for 2002 with the exception of the higher grading scales, which, are made up the client list with a higher invoicing value, which shows a bigger concentration.

5.1.2. The Gini concentration index applied to statutory auditing of non listed companies

It is important now to study the professional body of Statutory Auditors considering the awarding — points — which reflects the number and size of the companies they audit, to determine if the activity is exercised in a contracted form or not.

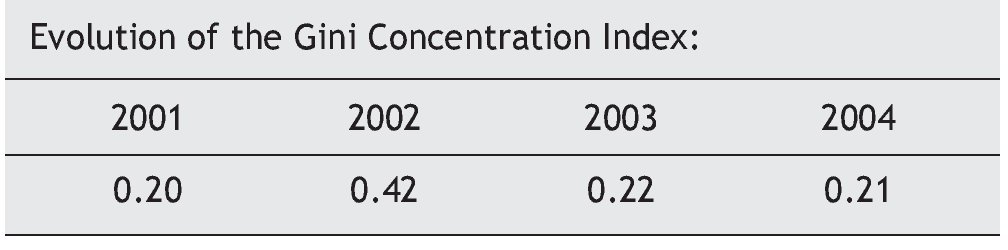

The data shows that, in the four years analyzed, the concentration of points and therefore the activity increased. However this is still a minimum concentration. Actually, we do not have a situation of maximum concentration, where only one auditor concentrates all the points, or a situation of nil concentration, where each auditor has equal proportion of points. That is we have a minimum situation, where the points are unequally shared by the auditors, but where the market is shared by all the auditors.

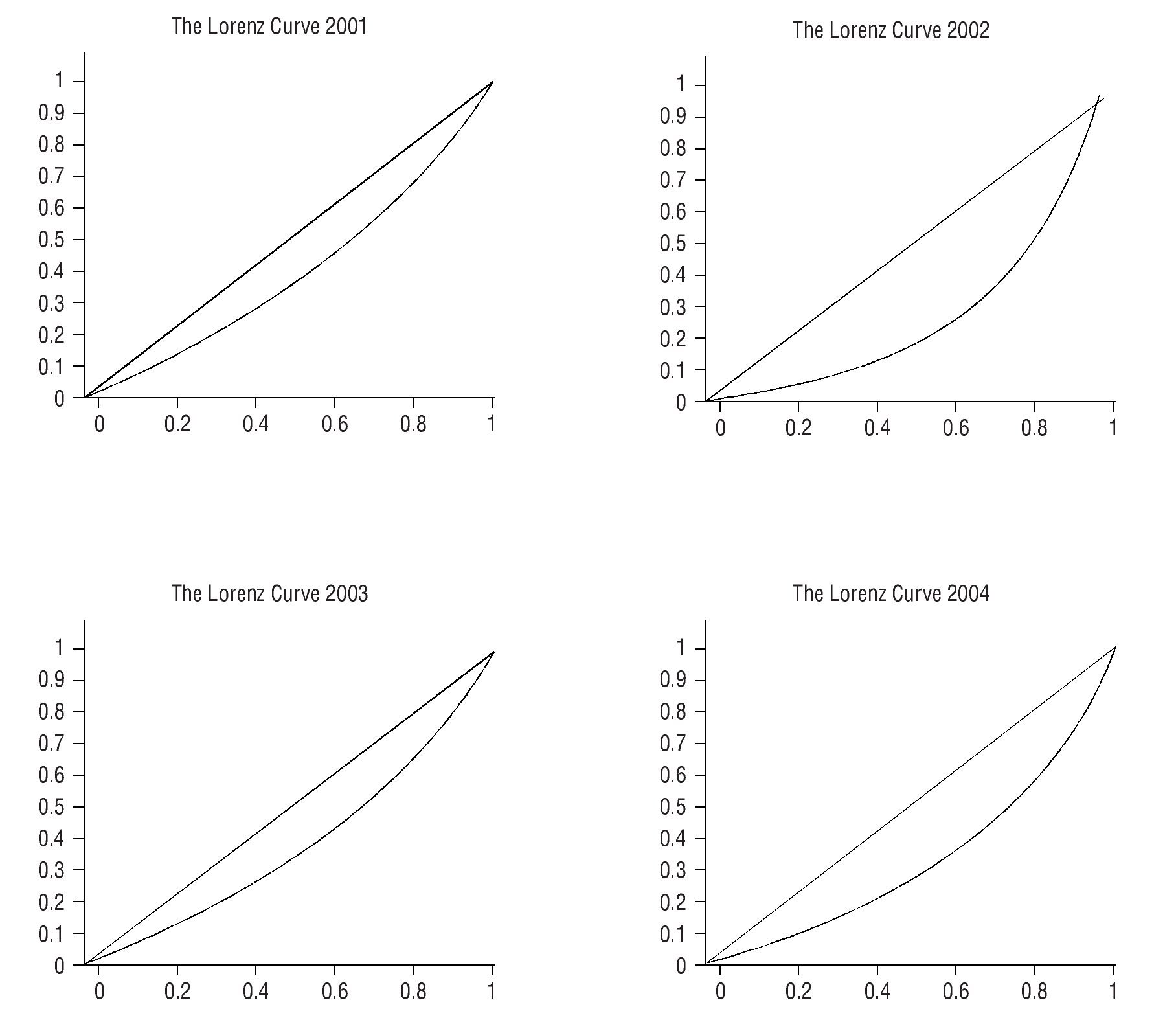

5.1.3. Concentration curves of Lorenz applied to statutory auditing of non listed companies (Figure 8)

Figure 8 The Lorenz curves for the audit market in 2001, 2002, 2003 and 2004.

The Lorenz curve shows the tendency concentration. We can see that the Lorenz concentration curve is moving away from the straight line of equal distribution, assuming, in 2004, a greater area, that is, the coefficient although intermediate, became bigger, which agrees with the Gini concentration index. In 2003, the distribution was more even than in 2004.

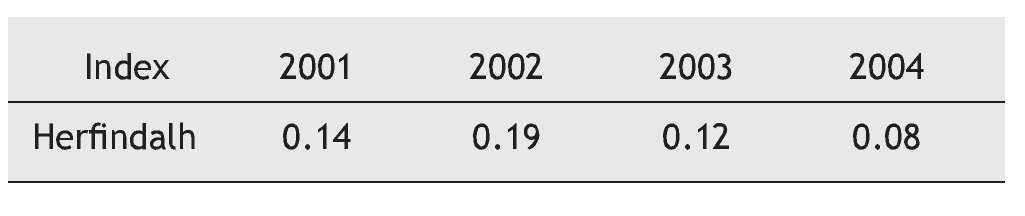

5.1.4. The Herfindahl index was applied on a sample corresponding to the three classes with the higher number of points, applied to non listed companies subject to statutory auditing of accounts

The evolution of the Herfindahl30 Index has the following evolution:

The importance of this indicator lies in the fact that it considers all the auditors are operating in the market and the distribution amongst them. When the value is 1, this indicates that the market is totally controlled by one society of auditors. The index is sensitive to the number of active auditors and the degree of activity measured by the ponderation, which is the pondered sum of the market quotas, translated into the number of points of each auditor. The auditors with the least points exercise less influence. The index also reflects the measure of dispersion of the market quotas between the various active auditors. This index measures in this c ase the activity of all the auditors working. An empirical study, like the concentration measures of the order n, suggests a minimum concentration shared by all the participants.

5.2. Analysis of the concentration of statutory auditing in listed companies on the regulated stock market.

5.2.1. Techniques of the concentration indexes31

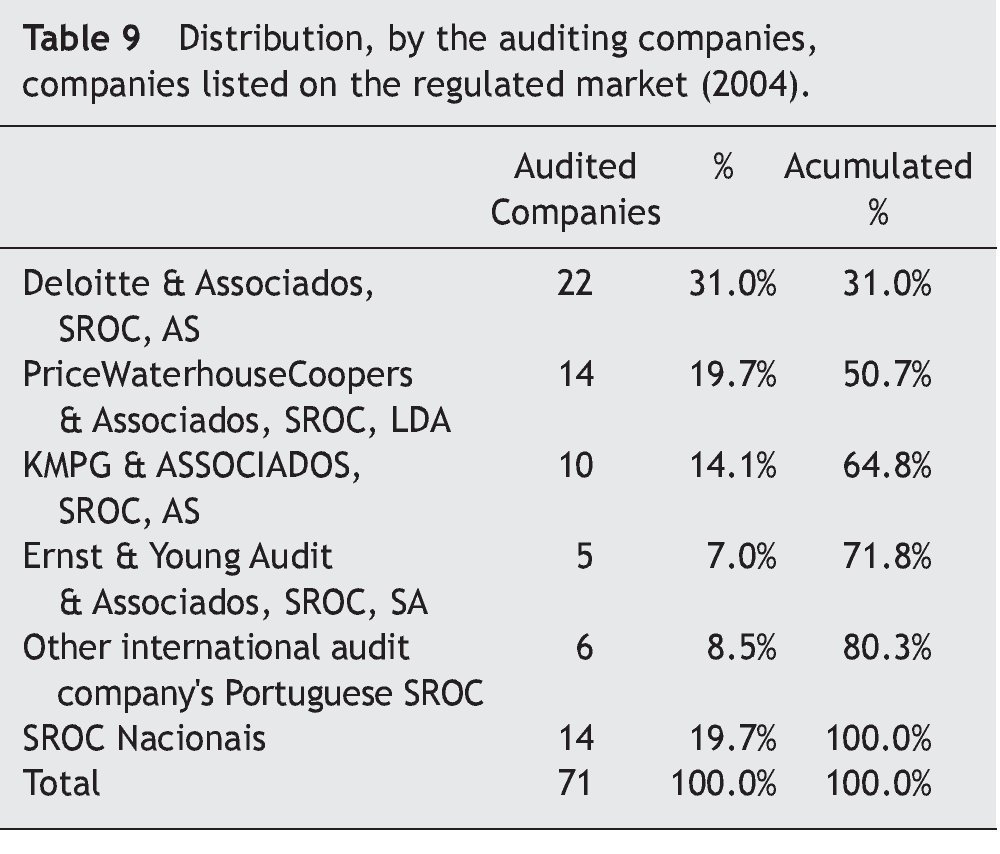

Distribution in case of companies with shares admitted on the stock market by international auditing companies (Table 9).

Applying the techniques of the concentration32 indexes of the order n, we found that 80% of the market of statutory auditing of listed companies is controlled by the international auditing companies. This situation is totally different from the one analyzed previously, regarding the listed companies that although they do not have a symmetric distribution, it reflects a market structure far from the concentration that occurs in the listed companies.

5.2.2. Herfindahl Index

The application of the Herfindahl Index shows a value of 0.92696, which shows a high degree of concentration of the company's audit of accounts of listed companies.

5.2.3. The Gini Index

The application of the Gini Index shows a value of 0,62, which shows that the statutory audit of the accounts of listed companies, is concentrated mainly on multinational audit companies operating in Portugal.

5.2.4. Lorenz Curve

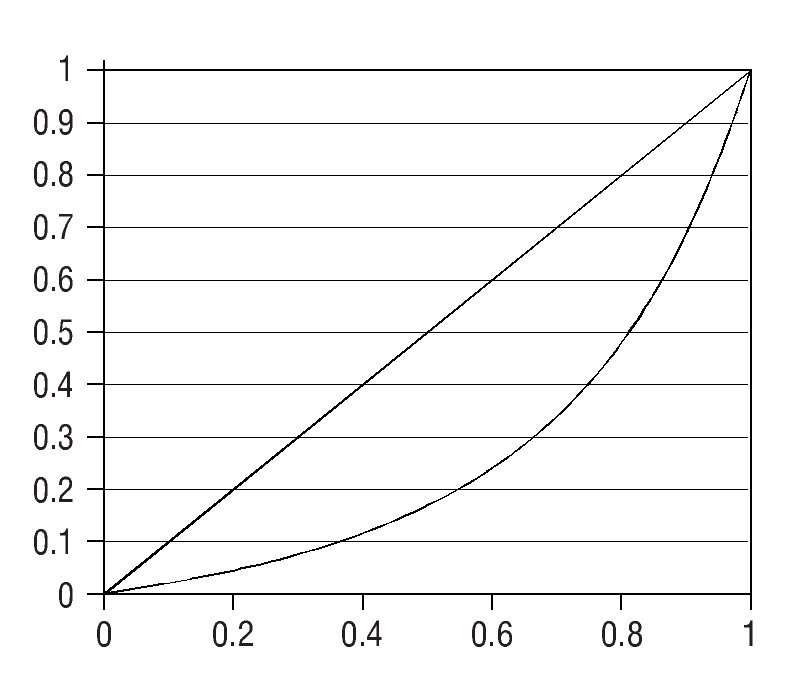

The same is shown in the Lorenz curve (Figure 9).

Figure 9 Lorenz curve.

The graph shows a situation of great concentration. The statutory auditing market in Portugal, of these types of companies, has an oligopoly nature, far from the theoretical structure of the perfect economy. The international auditing companies have a market share of 80%. Deloitte & Associates, SROC, SA, controls 31% of the market, followed by Pricewaterhouse Coopers & Associates, SROC, SA, of KPMG & Associates, SROC, SA. However it is not possible to suggest that international auditing companies, aim to eliminate competition from the market of listed companies, made implicit agreements with the aim of changing positions of statutory auditing by contractual auditing and through this eliminated all competition of national companies, stabilizing their market share quotas for statutory audits. A similar situation is seen in Spain (Benau & Martinez, 1998, p. 118) and this can be explained by the fact that in Portugal, in the 70's, although there was no compulsory statutory audit, all contractual auditing was done by international companies. These became rooted in the market due to their international prestige, technical knowledge, human resources, and contact with international clients and large scale economies.

6. Conclusion

With this study we tried to make an analysis of the historical evolution of auditing companies in Portugal, setting this issue in the international context. Company auditing, be it because of market demand or a legal requirement, led to the development of an auditing market. We also tried to do an empirical study to show market demand and offer of auditing services. The research led to the following conclusions:

The auditing of the companies is a concern of the governments in most continental and Anglo Saxon countries. This control especially of the listed companies is essential for the investors and the public in general since the financial and non financial information provided is the logic input of the system in decision making. The intervention of the State in the economy or its regulation must be seen as supplementary and for the common good.

— In Portugal, the auditing of the companies dates back to the end of the 19th century, and the Commercial Code awarded this duty, to at least three shareholders, who naturally did not meet the two fundamental requirements of those auditing: independence and competence. The concern to improve the auditing of listed companies in Portugal, was shared by the Portuguese society in the late 60's. Fernando Pessoa, the writer, acknowledged the uselessness of the Auditors Boards and Government Commissioners in the banks and the Limited companies.

— In our research, we did an historical and critical analysis of the professionalization process of chartered auditors (accounts) in Portugal, through a series of events that shaped the profile of the auditor and his professional statute. Chartered auditing began in 1974, at time economically and socially unstable, developing in very slowly, stabilizing with the adherence of Portugal to the EEC. In effect the entry of Portugal into the European Union in 1986, caused a strong boost on statutory auditing in Portugal.

— The history and evolution of statutory auditing in Portugal, shows a series of historical conditions evidencing the important role and the market share that the Big Four had, at the time the Big Six. Until the emergence of the statutory auditor, the Portuguese situation was marked by a total absence of auditing of all non listed companies. Therefore the awareness of the society for the need of regular auditing leading to a protected and regulated statutory market.

— The new Professional position — statutory auditor — is approved first by Decree-Law No. 49381, of 15 November of 1969 — New Auditing Rules for Companies —, and the activity is regulated Law Decree No. 1/72 of January 1972, and the first Annual General Meeting took place in 1974. This was considered the year the profession was created.

— The statutory auditing in Portugal developed until 2005, with a strong legal background, controlled by the Chamber of chartered auditors, and the structure of the offer was managed administratively, allocating a limited number of companies to each statutory auditor as well as setting the remuneration. This promoted a structure of balanced offer as well as an equitable geographical distribution of the minimum concentration although with uneven distribution.

— Statutory auditing in Portugal, at the beginning of 2005, shows a stabile and consolidated market. As a result at the beginning of 2005, the number of companies subject to Statutory Auditing of Accounts was 19.632, and the structure of the offer included 766 Chartered Auditors. The aim of our research was to understand how the auditor market was shared by the various Auditors, using indirect indicators to measure the activity. The indicators were the "points" earned by each auditor, and the number of listed companies audited. The results showed a level of concentration similar to other European countries — in the listed companies — and seemed to be organized in a virtual distribution, acquired administratively, for unlisted companies. This administrative management also had negative effects, such as not complying with the requirements set by the Chamber of chartered auditors, leading to a certain "management" of the of the available "points" by the auditors who did not wish to practice the profession.

— The entry barrier, namely the limitation of the points resulted in a generally equitable distribution of statutory auditing, both in quantitative and geographic terms.

— The fact that auditing was not compulsory resulted in a much lower demand. Since auditing has the same concerns that are characteristic of public property, various countries requested the use of auditing services. The auditing market is therefore an unusual market because the demand is not directly important to the companies but indirectly for the users of financial information.

— In Europe, the interest in the research of the national audit market, in the nineties of the last century, and the different studies published regarding the international scene show an high concentration in the market of the of the audit services especially on listed companies. Our aim was to find out if the European tendency was also applicable to Portugal.

— The empirical study done was based fundamentally in getting evidence regarding the structure of the market offer and demand in Portugal. In order to do this we analyzed the data provided by the Chamber of charted auditors for the years 2001, 2002, 2003 and 2004, found in accounts reports and in the list of listed companies. The research of these informative documents, gave us a better insight into the structure of the offer — the auditors and the structure of the demand — the companies subject to statutory audit of accounts.

— The activity is going through a process of internal change and the study made showed that the concentration of the activity in some auditors and audit companies is increasingly clearer. That is the degree of concentration of statutory audit in the listed companies is great and centered mainly on international audit companies. These controlled about 72% of the listed companies in 2004, which is explained by the increased internationalization of the Portuguese economy. This level of concentration is not different from the studies carried out in Spain, Germany, Holland, and confirms the nature of the oligopoly. On the other hand, when the process of the statutory audit was started, the international auditing companies were implanted in Portugal, which explains their dominance.

— The indices of concentration applied to the Statutory audit of accounts of non listed companies, Gini & Herfindahl and the Curves of Lorenz, suggest that:

• The concentrations are minimal in 2001, 2002, 2003 and 2004 (Gini), which reveals that the administrative criteria for sharing the points produced some equilibrium in the distribution.

• The Lorenz curve, in the years in question, when deviating from the distribution shows a slow tendency of concentration. The theory of the homogeneity of the auditing service has an evident explanation, the price, we believe, it is the most significant variable.

• On the other hand, the dimension of the listed enterprises, the complexity of their operations and transactions, as well as the corporate structures, require specialized audit services, that audit companies generally have difficulty in providing. The theory of service differentiation is applicable here.

— The previous analysis results in the statutory audit market of listed companies, shows a model of imperfect competition, because only a very small number of companies have an important capacity to dominate the provision of the services, resulting in high level of concentration.

— As from 2005, the Chamber of chartered auditors no longer published the distribution of the points by the auditors, therefore it is not possible to continue with the study after this. However, the study done suggested that, because of the lack of rotation of the auditors, the continuous renewal of their mandates and the entry barrier imposed on new auditors, resulted in the concentration tendency increasing in the years that follow.

1. The auditors had their practice limited to the number of companies were they could audit their accounts according to the number of points awarded to each company taking into consideration two indicators (gross assets the total of profits and earnings), that is, an indirect method of assuring the quality of auditing, limiting the number of companies that each auditor or audit society could have. As from the year when the score was set, the societies implemented quality control mechanisms for the adequate auditing of accounts in the exercise of their profession.

2. Companies Act, 1929; 1948; 1967.

3. Ministry of Commerce and Industry.

4. The inspectors nominated by minority shareholders should be members of the Instituto de Censores Jurados de Cuentas, Institute of sworn inspectors.

5. In the companies where the capital exceeded 5 million francs.

6. The capital not under 50 million liras.

7. During the reign of D. Dinis (1279-1325), there was already a differentiation between the different Ouvidores: Ombudsmaen of the Court, Ombudsmen of the requests, Ombudsmen of Crime, Ombudsmen of the Royal Deeds. Ordinance Ombudsmen, etc. These audited issues resulting from Royal properties Royal taxes and Expenses.

8. Started on 28 June 1888.

9. In art. 171º and 175º.

10. Knechel (2001), Liggio (1974) and Guy & Sullivan (1988).

11. Decree-law of 13 April of 1911.

12. Decree-law 5:029, of 5 October 1918.

13. Law 1936, 18 March — Base VII.

14. Law 1:995 17 May, which was never regulated.

15. According to some authors, such as Benau & Martinez (1998, p. 89), this is a fictitious audit.

16. Set in Decree-law 1/72, of 3 January.

17. And Decree-law 519-L2/79, of 29 December.

18. Decree-law 422-A/93, of 30 de October.

19. Decree-law 487/99, de 16 de November.

20. Meanwhile call the Chamber of chartered auditors.

21. Linking companies because of points awarding system, for example.

22. The societies that surpass 2 of the 3 limits listed below, for two consecutive years, are subject to statutory auditing: balance sheet total 1,500,000€, total gross sales and other profits 3,000,000€ and a 50 average number of workers during the exercise.

23. The situation the following years do not differ from the present because of renewal of mandates and the number of listed is limited. The year 2004 is the reference year due to the fact that it was the last when the activity was checked. The situation in previous years is similar for the said reasons.

24. List supplied by the Chamber of statutory auditors.

25. Quoted by Benau & Martinez, 1998, p. 113.

26. Individual Establishing Individual of Limited Responsibility.

27. The percentage relates to the totality of the ROC with activity in the year under review.

28. As shown the international studies mentioned in the introduction.

29. For easier calculation, the modal value coincides with the average point of the modal class, which does not distort the conclusions, that is, we consider that the distribution is symmetrical.

30. It is an index used in industrial economics to measure the market concentration. Applied to auditing, taking into account active auditors on the market and the spread of the activity of the structure of the offer of the auditing services. The mathematical equation is as follows:

where: H — index of Herfindahl, Zi — market share of the company and n — the No. of active companies in the market.

This index is the pondered sum of the market whereas smaller companies have a lower influence on the index than the larger companies.

31. The concentration analysis has various applications in economic and company studies. The rule 20/80 and the method ABC, are examples of the application of this type of analysis to the stock management.

32. This concentration does not reflect the Dynamics of the movement of income and expenses, nor the changes of the relative positions. The formula of the concentration indices is as follows: Cn = Σ Fn / F, where: Cn — market share of n companies, n — number of companies studied, Fn — number of companies, F — total number of companies in the market.

Received 1 December 2009; accepted 26 November 2011

E-mail address:

brunojmalmeida@gmail.com (B.J. Machado Almeida).

References

Afonso, J. D. (1981). A auditoria e a Certificação de Contas. Revista de Contabilidade e Comércio, n.º 180, vol. XLV.

Ballantine, H. (1946). On corporations, New York, USA.

Beattie , V., & Fearnley, S. (1994). The changing structure of the market for audit services in UK a descriptive study, Bristish Accounting Review, 26.

Benau, M., & Martínez, A. (1998). Qué espera la sociedad de la auditoría? La contabilidad del siglo XXI, Técnica Contable, Madrid.

Benau, M.A.G. Barbadilho, E.R., & Martínez, A. V. (1998). Análisis de la estructura del mercado de servicios de auditoría en España, Ministerio de la Economia y Hacienda.

Cardoso, P. (1976). Fiscalização das sociedades anónimas. Empresa Nacional de Publicidade, Lisboa.

Carqueja, H. (1972). Reflexões sobre os Revisores Oficiais de Contas. Revista de Contabilidade e Comércio, XXXIX (154).

Castel Branco, A. C. D'Aça. (1981). Revisores Oficiais de Contas — Profissão que singra. Revista de Contabilidade e Comércio, XLV (182).

Circular 36/04 de 4 de Junho, Ordem dos Revisores Oficiais de Contas.

CNSA — DL 225/2008 de 20 de Novembro.

Código das Sociedades Comerciais, (1992).

Código de Comércio (1888).

Colombo, G. (1969). Il bilancio di esercizio delle societé per azioni, Milan, Italy.

Companies Act (1929).

Companies Act (1948).

Companies Act (1967).

Costa, B. (1994). Sobre a inclusão dos ROC nos órgãos de fi scalização das sociedades. Revista de contabilidade e Comércio, L (200). Decreto-lei 487/99, de 16 de Novembro.

Decreto-lei 1/72, de 3 de Janeiro.

Decreto-lei 422-A/93, de 30 de Outubro.

Decreto-lei 5:029, de 5 de Outubro de 1918.

Decreto-lei de 13 de Abril de 1911.

Diário da República nº 24 de 20 de Novembro.

Directiva nº 2006/432/CE do Parlamento Europeu.

Dopuch, N., & Simunic, D. (1980). The nature of competition in the auditing profession: a descriptive and normative view. In Buckleh, J., & Weston, F. (Eds.), Regulation and accounting profession. Lifetime Learning, New York, NY, pp. 77-94.

Fernandes Ferreira, R. (1972). Ainda os Revisores Oficiais de Contas. Revista de Contabilidade e Comércio, XXXIX (156).

Guy, D., & Sullivan, D. (1988). The expectation gap auditing standards. Journal of Accountancy, April, New York.

Harris, J. (1937). Business organization and the public accountant. In Organization des Betriebs und des accountants, VII-International Accountants Congress.

Keuzenkamp, T. (1938). Prüfung des Jahresabschusses. In V International Prüfung und Treuhand Kongress, Berlin.

Knechel, W. (2001). Auditing, assurance & risk. South-Western College Publishing, 2ed, University of Florida.

Lei 1:995 de 17 de Maio

Lei 1936, de 18 de Março — Base VII.

Liggio, C. (1974). The expectation gap: the accountant´s legal waterloo. Journal of Contemporary Business, 3, 27-44.

Maijoor, S., Buijink, W., Van Witteloostuijn, A., & Zinken, M. (1995). Long-term concentration in the Dutch audit market: The use of auditor association membership lists in historical research, Abacus, 2.º, 152-177.

Marques de Almeida, J. J., (2002). A profi ssão de ROC: evolução e perspectivas. Revista de Contabilidade e Comércio, LVIII (230). Marten, K. (1997). Developments in concentration on the German audit market. In Workshop on auditor regulation in Europe. EIASM, Copenhagen.

Moizer, B. (1992). The state of the art in audit market research. European Accounting Review, (2).

Moizer, P., & Turley, S. (1987). Surrogates for audit fees in concentration studies. Auditing: A Journal of Practice and Theory, 7(1), 118-123.

Monteiro, M. N. (1975). Revisão Oficial de Empresas. Revista de Contabilidade e Comércio, XLII (166).

Oliveira, A. (1981). Revisão Oficial de Contas: Que ficção? (Breve comentário ao Dec.-lei 519-L2/79). Revista de Contabilidade e Comércio, XLV (180).

OROC (2001). Relatório e Contas da Ordem dos Revisores Oficias de Contas, OROC.

OROC (2002). Relatório e Contas da Ordem dos Revisores Oficias de Contas, OROC.

OROC (2003). Relatório e Contas da Ordem dos Revisores Oficias de Contas, OROC.

OROC (2004). Relatório e Contas da Ordem dos Revisores Oficias de Contas, OROC.

Pessoa, F. (1986). Da inutilidade dos Conselhos Fiscais e dos Comissários do Governo nos Bancos e nas Sociedades Anónimas. Revista de Contabilidade e Comércio, XLIV (193/96).

Pimenta, A. (1972). A prestação de contas do exercício nas sociedades anónimas. Edição do autor, Lisboa.

Silvão, A. J. P. (1979). Esboço de Manual das Funções de Revisor Oficial de Contas. Revista de Contabilidade e Comércio, XLIII (170 e 171).

Tena, G. (1959). La responsabilidad de los administradores de la sociedad anónima en derecho espanol. Anuario de Derecho civil, p. 19 e segts.