The present study was conducted to investigate the effects of mental workloads on the depression–anger symptoms and interpersonal sensitivities of accounting professionals. A model was created in keeping with the main objective of the study, and regression analysis was carried out on the questionnaire responses from 168 accounting professionals employed in Kayseri. The results revealed the significant positive impacts of mental workloads on the depression–anger symptoms and interpersonal sensitivities of accounting professionals.

El presente estudio se dirigió con el fin de investigar los efectos de la carga mental de trabajo en los síntomas de depresión-ira y sensibilidad interpersonal de los profesionales de la contabilidad. Se construyó un modelo para conseguir el objetivo fundamental del estudio, y se realizó un análisis regresivo de las respuestas a una encuesta de 168 contables en Kayseri. Los resultados revelaron un importante impacto positivo de la carga mental de trabajo en los síntomas de depresión-ira y en la sensibilidad interpersonal de los profesionales de la contabilidad.

Some professions are more physically and mentally demanding than others. In some professions, improved automation systems together with rapid technological developments, modern production and control tools have started to minimize the burdens upon the minds of relevant staff. However, due to the lack of any technological development, the minds of professionals in other professions have become overburdened. Such professions require the attention, concentration, motivation, judgment or evaluation of the individuals concerned. Accounting is one such profession. Accounting professionals have to work with high attention, caution and concentration levels for long periods of time. In the accounting profession, even a minor mistake may result in significant, serious and irreversible impacts on businesses. Therefore, accounting professionals exert significant mental efforts or, in other words, there is serious mental workload among them. It is evident that such a heavy mental workload may result in various negative perceptions, attitudes and behaviors. Therefore, the main objective of the present study is to investigate the effects of mental workloads on the depression–anger symptoms and interpersonal sensitivities of accounting professionals. Depressive symptoms, anger symptoms and interpersonal sensitivity were considered as the dependent variables of the study and mental workload was considered as the independent variable. Another objective of the present study is to evaluate the relationships among mental workloads and depression–anger symptoms and interpersonal sensitivity. Initially, a theoretical framework is provided and then the findings and discussions of the empirical study are presented.

1.1Mental workloadThere are several factors in a working environment that negatively affect the performance and health of individuals. Such negative factors and conditions should be minimized in order to allow individuals to work without any exposure to heavy workloads and stress. To minimize such negative factors and conditions, the characteristics of the relevant profession should be properly understood. The determination of the total workload level of a job is an important step in shaping the characteristics of a work environment or profession that result in overall physical and mental workload of employees (Dağdeviren, Eraslan, & Kurt, 2005, pp. 517–518). Within the total workload, mental workload is a prominent variable in some professions requiring a high level of attention, motivation, judgment and evaluations.

Mental workload is an intangible concept which by definition cannot be measured directly or assigned an absolute value. But, if one accepts that the human mind is limited in the rate at which it can process information, then mental workload can be seen as the percentage of that capacity in use at any time-point (Byrne, Tweed, & Halligan, 2014, p. 263). Mental workload is the amount of mental effort that an individual uses to perform tasks (Gao, Wang, Song, Li, & Dong, 2013, p. 1071). Mental workload is composed of the tasks to be performed by means of mental and perceptual activities such as calculation, decision making, communication, recognition and searching (Dağdeviren et al., 2005, p. 520). It is defined as the relationship between the mental resources required by a task and the individual ability to use such resources (Parasuraman, Thomas, & Sheridan, 2008, p. 146). According to Noyes et al. (2004), mental workload can be defined as the interactions between the task demands encountered while performing a job and the ability of an individual to overcome these demands (Öztürk, 2006, p. 8). Studies on mental workload were mostly conducted at the beginning of the 1960s with a greater emphasis upon the effects of mental workload on the quality of industrial works (Duru, Ermiş, Akay, & Kurt, 2005, p. 173). Such an emphasis is even more recognized nowadays together with the developments in computer technologies. Mental strength has become more important than physical strength with the increasing use of technology in working environments. There is significant evidence reporting the impacts of automated controls on mental workloads (Stanton, Young, Walker, Turner, & Randle, 2001, p. 233).

Mental workload also includes mental stress encountered while performing a specific task that requires perception, calculation and similar activities. Along with the characteristics of the task, it is a concept that also encompasses the task demands and ability and qualifications of an individual (Öztürk, 2006, p. 9). According to Young and Stanton (2001), the mental workload involved in a task is mediated by task demands, external support and previous experiences and it represents the level of resources toward the precaution required for meeting both objective and subjective performance criteria. In brief, mental workload depends on the characteristics of the task and the ability and qualifications of the individuals performing such tasks. Noise, hot or cold environments, light levels and similar environmental factors also affect mental workload and consequently performance (Teja and Guillermo, 2001, p. 412).

Mental workload is commonly used in ergonomics and has an ever-increasing significance in such studies (Young & Stanton, 2001). Beside ergonomics, it is also used in psychology, medicine, statistics and some other disciplines such as engineering (Öztürk, 2006, p. 8). Mental workload has a critical significance on performance (Young & Stanton, 2001). The approaches for evaluating mental workload are considered under three categories. The first is subjective measurements. These measurements are applied with the rational scales provided after the use of the system (Wiebe, Roberts, & Behrend, 2010, p. 475). There are several single and multi-dimensional subjective scales (Subjective Workload Assessment Technique) and NASA (National Aeronautics and Space Administration-Tasl Load Index) scales are the most commonly used ones in workload studies (Luximon & Goonetilleke, 2001, p. 230). The second approach for evaluating mental workload is performance measurements (Wiebe, Roberts, & Behrend, 2010, p. 475). Most of the measurements in this approach depend on the time of response to the assigned mental task and on the accuracy of the response (Öztürk, 2006, p. 17). The final approach for evaluating mental workload is physiological measurements. Pulse rate, dilation of the pupil and similar physical measurements are also used for indirect evaluation of mental workload (Wiebe, Roberts, & Behrend, 2010, p. 475). Mental workload that can be measured by various means is recognized as a significant issue in the literature (Parasuraman et al., 2008, p. 147).

1.2Depression–anger symptoms and interpersonal sensitivityExhaustion, depression, reluctance, anhedonia, slowdown in behaviors, pessimism, numbness, culpability, remorse, psycho-physiologic functional disorders and similar psychological symptoms have become unavoidable problems in modern social life. In this sense, such symptoms are considered as both an individual and a social problem.

Depression together with mental collapse and sadness significantly affect physical and mental processes and result in social disabilities (Blazer, Swartz, & Woodbury, 1998). Depressive symptoms are evaluated under two groups as psychological and somatic and some of these symptoms can be listed as follows (Taneli, Taneli and Taneli, 2001:5): depressive temperament, grief, monotone speech, pessimism, desperation, hopelessness, poor morale, anxiety, discomfort, tension, mournful gestures, concentration difficulty, slowdown in thought flow, lack of energy, exhaustion, unreasonable decrease in cheer, insomnia, apathy, anorexia, loss of weight or obesity, difficulty in decision making, memory disorders, difficulty in remembering, stomach discomfort, constipation, feelings of worthlessness, feelings pressure in the chest, palpitations, feelings inadequacy, discomfort in breathing, feelings of guilt, etc. Depression affects the quality of individual life, as well as the quality of work life. It is a mental issue (Takagishi, Sakata, & Kitamura, 2011, p. 919) and may result in significant costs to businesses. The significance of this issue has already been pointed out in relevant studies (Kessler et al., 2013). Job absences in depressive employees are usually higher than in others and depressive employees also have low performance and productivity levels (Welsh, 2009, p. 320).

Similar to depression, anger also has serious negative impacts on both individuals and organizations. Depressive individuals were reported to have less interpersonal ability, higher communication problems and negative lives than normal individuals (Şahin, Batıgün, & Koç, 2011, p. 18). Biagio (1989) defined anger as a powerful emotion created against an actual or assumed hindrance, threat or injustice and as an emotion orienting the individual to eliminate the disturbing stimulants (Balkaya & Şahin, 2003, p. 193). Anger may result in aggressive behavior, inner-family violence, substance addiction as well as physical disorders (DiGiuseppe & Tafrate, 2006, p. 70).

Interpersonal sensitivity is expressed as the stress created by feelings of inadequacy and self-humiliation in an individual (Aştı, Acar, Bağcı, & Bağcı, 2005, p. 27). There are various reasons for interpersonal sensitivity such as long working hours, physical and social negative working conditions (Selvi et al., 2010, p. 241). Therefore, accounting professionals are also considered as sensitive individuals with regard to interpersonal sensitivity since they have to work for long hours with a high level of caution, attention and concentration.

Protection of the physical and mental health of employees and prevention of the negative psychological and sociological impacts of work life on employees are among the basic targets of modern sciences (Özgür, Gümüş, & Güldağ, 2011, p. 296). The characteristics of relevant tasks, and the required physical and mental workloads may easily affect the psychological processes of individuals. Therefore, the basic objective of the present study is to investigate the effects of mental workloads on the depression–anger symptoms and interpersonal sensitivity of accounting professionals.

2Method2.1Research model and hypothesesA theoretical model was created in this study to investigate the effects of mental workloads on depression, anger and interpersonal sensitivity in accounting professionals. The model is provided below (Fig. 1):

In line with this model, three hypotheses were formed to test the relationships among mental workload and depression–anger symptoms and interpersonal sensitivity. The hypotheses are as follows:Hypothesis 1 Mental workloads have significant positive effects on the depression symptoms of accounting professionals. Mental workloads have significant positive effects on the anger symptoms of accounting professionals. Mental workloads have significant positive effects on the interpersonal sensitivity of accounting professionals.

The research universe was composed of independent accounting professionals in Kayseri. Therefore, the universe included certified public accountants, certified public accountant financial advisors and sworn-in certified public accountants. In Kayseri, there are 173 certified public accountants, 869 certified public accountant financial advisors, 25 sworn-in certified public accountants, making a total of 1070 accounting professionals. Some of them work independently in their private offices and some work as waged employees in businesses. Considering the fact that independently working accounting professions and those working for a business (waged ones) may have different mental workloads, and in order to create a homogenous universe, only independently working certified public accountants were included in the study and waged ones were not included in the research universe.

There were 541 accounting professionals independently working from their offices during the research period. The formula of the simple randomized sampling method was used to determine the sample size at 95% confidence level and ±5% standard deviation (Nakip, 2003, pp. 212–214) and it was decided that questionnaires should be administered to 225 accounting professionals.

2.3Data collectionResearch data were gathered by means of a previously created questionnaire form. The addresses of accounting professionals to be included in the research universe were obtained from the website of the Kayseri Chamber of Certified Public Accountant Financial Advisors. Then the questionnaire forms were distributed to the offices of those accounting professionals. Of the distributed forms, 168 responses were received. The representation rate of the sample for the universe was 31%.

2.4ScalesData were gathered through questionnaire forms. The forms were composed of three sections: Section 1 included questions about the demographic characteristics of the participants. Section 2 contained the scale to determine the mental workload of accounting professionals and Section 3 included the scale to determine depression and anger symptoms and the interpersonal sensitivity levels. Information about the relevant scales is provided below.

2.4.1Mental workloadMental workload may vary as professions. For instance, the pilot's mental workload requires more than one measure (Wilson, 2009, pp. 4–5). In this research, the NASA Task Load Index (NASA-TLX) method was employed to determine the mental workload levels of the participants. Although there are several studies in the literature about the measurement of mental workloads, the NASA-TLX method has been shown to be a more precise method than others (Duru et al., 2005, p. 175; Hancock, 1988; Luximon & Goonetilleke, 2001). The relevant method is composed of 6 different mental workload dimensions. These are (Duru et al., 2005, p. 175):

- •

Mental stress: Necessity of mental or perceptual activity, intensity of mental and perceptual activity, easiness or difficulty of the task, simplicity or complexity of the task (thinking, perception, calculation, remembering, analysis).

- •

Physical stress: Amount, easiness or difficulty, slowness or rapidness, ease or difficulty of the necessary physical activity (walk, push, pull).

- •

Time limitation stress: Time pressure during the performance of processes or process steps. Sequential occurrence of tasks, like the start of one task before the end of another task.

- •

Effort: Hard working and consequent mental and physical effort.

- •

Performance: Rate of success in implementation of tasks. Level of satisfaction of both the employee and the employer following the implementation of a task.

- •

Tension: Insecurity, stress, lack of courage felt by the employee or the reverse of them.

To measure the mental workloads of accounting professionals, they were asked about the level of exposure to the above specified stress factors and were requested to grade it in a scale of 0–100. In this scale, “0” indicates low mental workload and “100” indicates high mental workload.

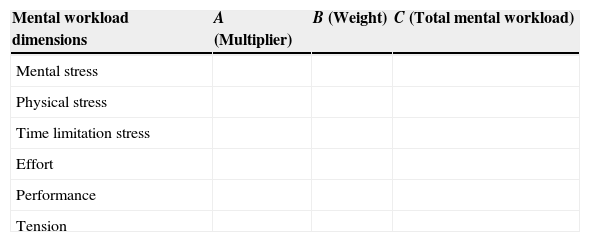

To calculate the mental workload of the participants, they were requested to order the significance of each mental workload dimension from 0 to 5. In this scale, “0” indicates low significance and “5” indicates high significance. The mental workloads of accounting professionals were calculated by the method provided in Table 1.

Calculation of mental workload.

| Mental workload dimensions | A (Multiplier) | B (Weight) | C (Total mental workload) |

|---|---|---|---|

| Mental stress | |||

| Physical stress | |||

| Time limitation stress | |||

| Effort | |||

| Performance | |||

| Tension |

A (Multiplier): Significance order of the mental workload should be between 0 and 5 and the total should be 15.

B (Weight): Weight of the exposed mental workload dimensions should be between 0 and 100.

C (Total mental workload): (C=A×B).

Weighted average workload=Total mental workload/15.

The Brief Symptom Inventory (BSI) scale developed by Derogatis (1975) was used to determine the depression, anger and interpersonal sensitivity levels of the participants. The scale is composed of 5 points and the frequencies of the feelings of the participants during the last 7 days were asked for. Scale reliability (Cronbach Alfa) was calculated as 0.79. A Likert type scale was used to determine the depression, anger and interpersonal sensitivity levels of the participants. In this scale, “1” indicates never and “5” indicates always.

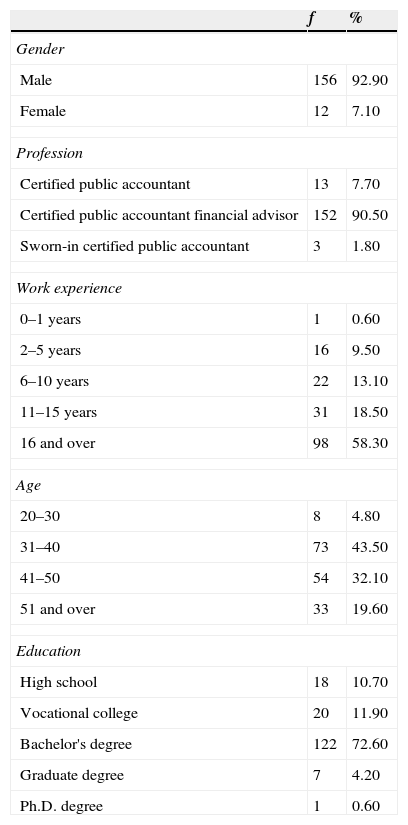

3Results3.1Demographical characteristicsThe demographic characteristics of the participants (gender, work experience, age and educational level) are provided in Table 2.

Demographic characteristics of participants.

| f | % | |

|---|---|---|

| Gender | ||

| Male | 156 | 92.90 |

| Female | 12 | 7.10 |

| Profession | ||

| Certified public accountant | 13 | 7.70 |

| Certified public accountant financial advisor | 152 | 90.50 |

| Sworn-in certified public accountant | 3 | 1.80 |

| Work experience | ||

| 0–1 years | 1 | 0.60 |

| 2–5 years | 16 | 9.50 |

| 6–10 years | 22 | 13.10 |

| 11–15 years | 31 | 18.50 |

| 16 and over | 98 | 58.30 |

| Age | ||

| 20–30 | 8 | 4.80 |

| 31–40 | 73 | 43.50 |

| 41–50 | 54 | 32.10 |

| 51 and over | 33 | 19.60 |

| Education | ||

| High school | 18 | 10.70 |

| Vocational college | 20 | 11.90 |

| Bachelor's degree | 122 | 72.60 |

| Graduate degree | 7 | 4.20 |

| Ph.D. degree | 1 | 0.60 |

Demographic characteristics were not evaluated with regard to the criteria specified in the research model. Analyses were not performed about differences or relationships, were demographic characteristics included in the hypotheses. Demographic questions were asked only to get a general idea about the research universe. Such characteristics were also provided to allow the other researchers to see the characteristics of the universe.

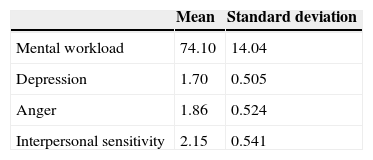

3.2Mean value of variablesMean values of research variables and their standard deviations are provided in Table 3.

Considering the 5-point Likert scale to measure the depression–anger symptoms and interpersonal sensitivity levels of the participants, the mean value should be “3”. Therefore, the current values of depression–anger symptoms and interpersonal sensitivity levels seemed to be lower than the averages. Based on the above specified calculation method, the mental workload average should be 50. Therefore, the average mental workload values were found to be much higher than the mean values.

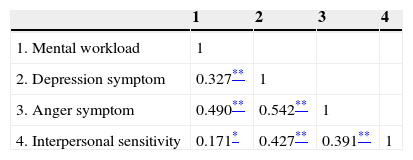

3.3CorrelationThe correlation matrix indicating the relationships among the mental workload, depression, anger and interpersonal sensitivity of the participants is provided in Table 4.

Table 4 reveals significant positive relationships among mental workload and depression–anger symptoms and interpersonal sensitivity. Such results indicated increasing depression, anger and interpersonal sensitivity levels with increasing mental workloads in accounting professionals.

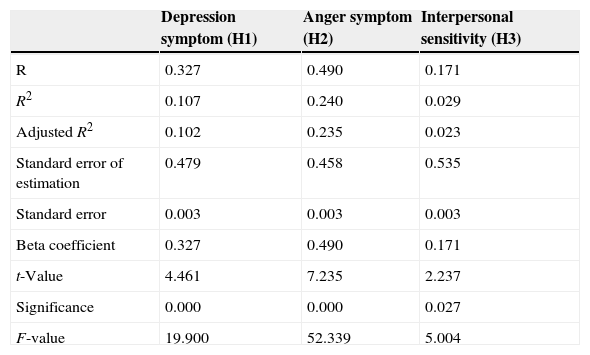

3.4Testing hypothesesRegression analysis was performed to test the effects of mental workloads on depression–anger symptoms and interpersonal sensitivity in accounting professionals. The results of regression analysis are provided in Table 5.

Results of regression analysis to test the hypotheses.

| Depression symptom (H1) | Anger symptom (H2) | Interpersonal sensitivity (H3) | |

|---|---|---|---|

| R | 0.327 | 0.490 | 0.171 |

| R2 | 0.107 | 0.240 | 0.029 |

| Adjusted R2 | 0.102 | 0.235 | 0.023 |

| Standard error of estimation | 0.479 | 0.458 | 0.535 |

| Standard error | 0.003 | 0.003 | 0.003 |

| Beta coefficient | 0.327 | 0.490 | 0.171 |

| t-Value | 4.461 | 7.235 | 2.237 |

| Significance | 0.000 | 0.000 | 0.027 |

| F-value | 19.900 | 52.339 | 5.004 |

Dependent variable: depression, anger, interpersonal sensitivity.

Independent variable: mental workload.

Considering the values presented in Table 5, all 3 hypotheses were accepted and the research model was found to be significant as a whole (FH1=19.900, FH2=52.339, FH3=5.004).

The results revealed that the mental workloads of accounting professionals were able to represented 10.2% of their depression symptoms, 23.5% of their anger symptoms and 2.3% of their interpersonal sensitivities. The calculated beta coefficients were positive indicating increasing depression–anger symptoms and interpersonal sensitivities with increasing mental workloads in accounting professionals.

4Results and discussionThe present study was conducted to determine whether or not mental workloads have significant effects on the depression–anger symptoms and interpersonal sensitivity of accounting professionals. A model was created in line with this objective and three hypotheses were formed and tested.

The first hypothesis of the research model was concerned with the increase in depressive symptoms of accounting professionals with increasing mental workloads. The results revealed increasing depressive symptoms with increasing mental workloads.

The second hypothesis of the research model was concerned with the increase in anger symptoms of accounting professionals with increasing mental workloads. The results revealed that mental workload had significant positive effects on anger symptoms in accounting professionals.

The third hypothesis of the research model was concerned with the increase in interpersonal sensitivity levels of accounting professionals with increasing mental workloads. The results revealed that mental workloads had significant positive effects on the interpersonal sensitivities in accounting professionals.

Accounting professionals perform the tasks of defining, measuring and reporting the documented economic activities of businesses to help the end-users to judge such activities. Therefore, they serve as a bridge between the information users and the businesses. The information provided by accounting services should be reliable, comparable, transparent, and clear and should be available for decision making. It should also be free from prejudice. Otherwise, the decision made by the users of this information will not be reliable.

Certified public accountants have significantly high mental workloads within today's working environment since the tasks they perform require extreme caution and attention and should be free of any mistakes. Ever-changing legislations, the keeping of the daily accounts of businesses, the significance of timing and similar factors continually increase the mental workloads of accounting professionals. Therefore, attempts should be made to reduce their mental workloads so that they can perform better.

Reductions in the mental workloads of accounting professionals will definitely minimize their depression symptoms. Increasing depressive symptoms may significantly affect their physical and mental health and reduce their performance, commitment, life quality and satisfaction. Therefore, the components of mental workloads should be brought under control and relevant measures should be taken to lessen the mental workloads. Such measures will not only result in healthy and happy individuals but will also allow the accounting business to gain the desired status and prestige. Thus, sporting activities, reduction of working hours and number of ledgers, taking a vacation in financial recess periods, and going to the theatre, cinema and similar places may be recommended to accounting professionals reduce their mental workload and allow them to have some respite from their heavy workload.

Similar studies may be conducted in different provinces and with different scales, such studies may also focus on intermediate variables, which are able to reduce the mental workload of accounting professionals.

Conflict of interestThe authors declare no conflict of interest.