The purpose of this paper is to evaluate the degree of comprehension and enforcement of social responsibility (SR) practices in micro, small and medium companies in Barranquilla (Colombia), based on the Stakeholders theory. Using an exploratory factor analysis on 779 companies it was found that the variables with a stronger explanatory influence for socially responsible performance are employees, environment, and community. By contrast, corporate management, value chain, and government/public sector condition the development of SR actions. Particularly, there is a weak perception and lack of will among owners and company managers to undertake comprehensive programs of social responsibility, as well as the formalization of those actions with an impact on the SR.

El propósito de este artículo es evaluar el grado de percepción y aplicación de prácticas de responsabilidad social (RS) en las micro, pequeñas y medianas empresas de la ciudad de Barranquilla (Colombia), siguiendo la teoría de los Stakeholders. Utilizando un análisis factorial exploratorio en 779 empresas se encontró que las variables con mayor influencia explicativa del desempeño socialmente responsable son empleados, medio ambiente y comunidad. En contraste, dirección corporativa, cadena de valor y gobierno/sector público condicionan el desarrollo de acciones de RS. Particularmente, se encuentra una débil percepción y falta de voluntad entre propietarios y directivas de las empresas para emprender programas integrales de responsabilidad social, así como la formalización de aquellas acciones con incidencia en la RS.

O objetivo deste artigo é avaliar o grau de percepção e aplicação das práticas de responsabilidade social nas micro empresas, pequenas e médias empresas da cidade de Barranquilla (Colômbia), seguindo a teoria dos Stakeholders (grupos de interesse). Usando uma análise de fatores exploratórios em 779 empresas, verificou-se que as variáveis com maior influência explicativa do desempenho socialmente responsável são os empregados, o meio ambiente e a comunidade. Em contrapartida, o gerenciamento corporativo, a cadeia de valor e o governo/setor público condicionam o desenvolvimento de ações de responsabilidade social. Particularmente, há uma fraca percepção e falta de vontade entre os proprietários e os gerentes das empresas para realizar programas integrados de responsabilidade social, bem como a formalização das ações que influenciam a responsabilidade social.

Despite growing recognition on the importance of implementing social responsibility (SR) practices in enterprises, investigations on the subject in micro, small and medium enterprises (MSMEs) in developing countries are sparse and less visible (Von & Melé, 2009). Most of the current literature is focused on developed countries, and mainly on large enterprises (Ma, 2012). However, the concern and relevance placed on studying the social scope on smaller enterprises in both developed and developing countries is concentrating more attention in SR specialized literature (Ma, 2012; Welford, 2005).

Globally, the volume of MSMEs1 and their contribution to economic growth, employment generation and enterprise participation amounts to 33% of GDP, 45% of total employment, and around 90% of the business fabric (Bell, 2015). This economic leadership has awoken a larger interest amongst the academic community, multilateral institutions, business associations, government and society, because of the social implications that these enterprises might have on their social environment. Thus, there are more investigations with different approaches and methods exploring the enforcement of SR practices in MSMEs in developed and developing countries (Adapa & Rindfleish, 2013; Coppa & Sriramesh, 2013; Demuijnck & Ngnodjom, 2013; Hsu & Cheng, 2012; Jenkins, 2006; Russo & Tencati, 2009).

In the context of developing countries, distinctive, fragmented, and ambiguous results (Linh, 2011) characterize research on SR in MSMEs (Jamali, Lund-Thomsen, & Jeppesen, 2015). The restriction of financial resources, commercial priorities, skepticism over the benefits of responsible practices, informal means of communication, centralized power, lack of knowledge about SR amongst directive, constitute some of the causes for the scarce interest in their research (Lepoutre & Heene, 2006; Vásquez & López, 2013; Vives, Corral, & Isusi, 2005).

In the case of Colombia, the limited research on SR in MSMEs has a descriptive reach, similar to studies executed in other developing countries, in which qualitative research of SR is predominant (Lockett, Moon, & Visser, 2006). In particular, Aya and Sriramesh (2014) have carried out a qualitative research on the perception and practices of RS (Responsabilidad Social) on a sample of Colombian MSMEs and have found in their informal practices, the culture and context that surrounds the genesis of the internal and external SR. Additionally, Sierra and Londoño (2008) propose a theoretic analysis on SR and MSMEs and suggest incorporating socially responsible practices to the traditional entrepreneurial schemes as a strategy that could contribute substantial benefits to enterprises and their Stakeholders. Both studies limit their scope to the descriptive analysis of their results, ratifying the need for literature to advance research that quantify and evaluate socially responsible practices (Gallardo, Sánchez, & Corchuelo, 2013).

In other papers in the same context, León, Castán, and Afcha (2015) found little evidence for the practices of SR, informality and a little relation to the management of business activities in the case of the MSMEs of Sincelejo (Colombia). Likewise, they show a direct relationship between the size of firms and compliance with SR practices, with lower standards for micro and small companies compared to medium-sized companies. In general, several authors acknowledge in the MSMEs of Colombia the distinctive and informal application of SR practices, with shortcomings in the internal and external communication of their SR actions and without any strategic focus (Duque, García, & Azuero, 2014; García, Azuero, & Salas, 2013; Sanclemente, 2015).

In that sense, the purpose of this paper is to contribute to the empirical literature available on the research of SR on MSMEs,2 drawing from the measuring of SR practices in the smaller enterprises of the city of Barranquilla.3

In particular, Barranquilla's microenterprises represent the largest sector of the city's businesses at 87.70%; besides, they contribute 23% to the local GDP, a corporate net investment of 30.2%, the stock of registered enterprises is 63%, the employment generation in the manufacturing industry is of 46.1% and they account for 1% of all the exportations (Cámara de Comercio de Barranquilla, 2016; Departamento Nacional de Estadísticas-DANE, 2015).

Following the Stakeholders theory, the influence of each of these criteria on the enforcement of socially responsible actions was explored, and the practices with a highest impact on the presence of SR in the MSMEs of Barranquilla are measured, using an exploratory factor analysis (EFA). Likewise, the current research aims to answer the following queries: (i) Which economic characterization are exhibited by MSMEs in Barranquilla? (ii) What degree of knowledge and enforcement of socially responsible practices is experimented by MSMEs? and (iii) Which Stakeholders are more influential in the implementation of socially responsible practices in MSMEs?

This research has two contributions, first, it deepens the specialized literature on the measurement of SR in developing countries, through the examination of Stakeholders and their influence in SR practices in MSMEs. Secondly, it offers a wider view on MSMEs regarding SR by including a significant sample of the city's microenterprises. Finally, given that SR in MSMEs in Barranquilla has not been explored in Colombia, this research aims to fill that void, through an exploratory analysis that examines the level of development of socially responsible practices, along with the influence that different Stakeholders might hold over the implementation of socially responsible practices in local MSMEs.

This paper is structured in three main sections: the first exposes the theoretical bases that justify the participation of Stakeholders in MSMEs. The second describes the empirical methodology and instruments utilized. The third shows the results of the empirical analysis. Finally, in the last section, the results are discussed and the conclusions of the research are presented.

2Theoretical frameworkDespite a rise in recent years in literature specialized in SR characterized by a plurality of opinions, variety of approaches, and application in different ambits (financial, academic, technological sectors, amongst others), there is still a need to provide a theoretical framework that facilitates the understanding and orientation of socially responsible practices specific to SMEs (Jamali, Zanhour, & Keshishian, 2009; Jenkins, 2004), emphasizing the relationship between society and enterprise through a thorough knowledge of reality and a solid ethical foundation (Dunham, Freeman, & Liedtka, 2001; Garriga & Melé, 2004).

The construction of a theory and a generalized model for SR that provides a responsible perspective of the management of MSMEs is still far from being consolidated (Guibert, 2009; Russo & Tencati, 2009; Weltzien & Shankar, 2011). This restriction has limited the advancement of knowledge, leading to minimally conclusive results in existing research (Salzmann, Ionescu-Somers, & Steger, 2005). Therefore, the interpretation of Stakeholders as an alternative approach to the SR-MSMEs link is useful given the close relation between them; in addition to the strategies and structures particular to these enterprises (Herrera, Larrán, Martínez, & Martínez, 2016; Murillo & Lozano, 2006).

Accordingly, our article bases its approach on the theory of Stakeholders. Even though some authors consider this theory appropriate for large enterprises (Gelbmann, 2010; Key, 1999; Perrini, 2006) by incorporating policies and ambits of SR designed for their interests (Enderle, 2004; Jenkins, 2004) it is also evident in literature how the Stakeholders theory is used to measure SR in MSMEs (Gallardo et al., 2013) with results similar to those achieved in large enterprises (Coppa & Sriramesh, 2013).

Otherwise, to infer homogeneously on the responsible practices of MSMEs toward microenterprises is a recurring trend in some research, and because of that, our investigation segments the analysis of SR by size and economic sector, aiming to identify both common and distinctive patterns in the practice of SR amongst Barranquilla's MSMES.

Therefore, in order to explore the scope and relevance of the SR theory and its link with the Stakeholders in local SMEs, the explanatory arguments that justify the presence of Stakeholders and the influence that they can have in the context of smaller companies.

2.1Stakeholders theoryThe Stakeholders theory appeared in the mid-1980s, and ever since, its interpretative amplitude and application of its approach has been a constant in the entrepreneurial and academic ambits. However, the release of Freeman's book (1984) “Strategic Management: A Stakeholder Approach” stands out as the authoritative text that develops the “theoretical–practical” framework for the study and formal development of this theory. In this text, Freeman (1984) defines the Stakeholders as “any group or individual who can affect or is affected by the achievement of the organization's objectives” (p. 24); even though in one of its most recent definitions he conceives them as “those groups who are vital to the survival and success of the corporation” (Freeman, Wicks, & Parmar, 2004).

As for the initial version of entrepreneurial relations with Stakeholders, Freeman proposed to analysis them on three levels: (i) rational, which involves the comprehension and importance of the main Stakeholders and their role in the enterprise's development; (ii) as a process, by establishing the connections that implicitly or explicitly are held with Stakeholders allowing the construction of a generic initial chart with different Stakeholders; and (iii) at a transactional level, referring to the ensemble of frequent transaction with Stakeholders and their competing interests. The convergence and complexity of relations with Stakeholders lead to exploring and developing methods for strategic actions.

On the other hand, the evolution of this concept incorporates new trends and corporative challenges, even though it maintains a consensus with the traditional version (Brenner & Cochran, 1991; Carroll, 1989; Saeidi, Nazari, & Emami, 2014). In the development of the modern theory, Donaldson and Preston (1995) argued in favor of three categories for its analysis: (i) descriptive, which evaluates the interrelations and common interests of the enterprise with its Stakeholders and their respective behaviors; (ii) instrumental, which examines the links between the Stakeholders and the attainment of corporative goals, vinculating means and ends in their purpose (Jawahar & McLaughlin, 2001), along with cost effectiveness (Margolis & Walsh, 2001); and (iii) normative, which combines the interests of all Stakeholders for the benefit of the enterprise on the bases of a principle (Friedman & Miles, 2006).

For their part, Mitchell, Agle, and Wood (1997) proposed the theory of identification of Stakeholders, classifying their connection with the enterprise in function of the degree of incidence they have over the entrepreneurial goals. For that end, they put forward three objective criteria to be organized in the hierarchy of a corporation: (i) the Stakeholders’ power to influence over the enterprise; (ii) the necessary legitimacy to maintain the relations between the Stakeholders and the enterprise; and (iii) the urgency of the Stakeholders’ definite aspirations. The combination of these three criteria allows for a comprehensive typology of Stakeholders that allows modeling their outlines.

Thus, the grouping of these criteria configures seven categories of Stakeholders: (i) with power and legitimacy, but without urgency; (ii) with legitimacy and urgency, but without power; (iii) with power and urgency, but without legitimacy to achieve their aspirations; (iv) with all three characteristics: power, urgency and legitimacy. Regarding the rest of the Stakeholders who can only offer one distinctive trait (power, legitimacy and urgency), there are: (v) with power, but without legitimacy or urgency; (vi) with legitimacy, but without power nor urgency; and (vii) with urgency, but without power nor legitimacy.

In summary, Mitchell et al. (1997) typify the different classes of Stakeholders as: (i) dominant, with power and legitimacy, which are part of the dominant coalition and are key to the long term organization; (ii) dependant, with urgency and legitimacy but with the power to directly assert their aspirations, which makes them dependent on others’ power, and prone to forming alliances; (iii) dangerous, those with urgency and power, but without legitimacy that may become violent and coercive in the search for their pretensions, even though they do not have legitimacy to enforce them. It is way, Fernández and Bajo (2012) suggest the experiment of topographically lifting the Stakeholder's map to categorize them according to the three characteristics, and to later ascertain the degree of connection and the level of institutionalization of these relations. Finally, knowledge of mutual expectations will allow to decide the positions and the largest possible scenario for interacting with the Stakeholders.

On the other hand, Friedman and Miles (2002) use two criteria to define the relations with an enterprise's Stakeholders. Their typology is based on two distinctions (i) compatible or incompatible in terms of ideas and material interests associated with social structures; and (ii) necessary or contingent, the relations between Stakeholders. The internal relations are necessary in a social structure or for an ensemble of logically connected ideas. The contingent relations are external or not connected integrally. As a result, four kinds of relations between enterprises and Stakeholders are discerned, giving rise to a situational logic that encourages a determined course of strategic actions.

In this sense, the logic can be: (i) type A, compatible relations which are necessary when all parts have something to gain from the connection. Its logic consists of protecting said relation as a strategy that safeguards their interests. (ii) type B: institutional provisions which will eventually be compatible. Both parts have the same interest, but there is not a direct relation between them. An opportunist strategy is most logical. (iii) type C: institutional relations which will eventually be incompatible; they only become conflictive when one of the parts tries to set their position above the others. The strategy consists of defending personal interests, inflicting maximum damage to the other part by trying to eliminate or discredit the position or opinion. (iv) type D: necessary incompatible relations happen when the material interests are intrinsically related, but their operations will form the relation whilst being threatened. The situational logic is to concede and compromise.

The previous review of the Stakeholders theory provides the theoretical basis for identifying and describing the influence Stakeholders of the RS in the MSMEs of the city of Barranquilla.

2.2Stakeholders and social responsibility in MSMEsSome studies point that the link between SR-MSMEs can be better understood under the Stakeholders theory (Jenkins, 2006). For the past few years, it has constituted the dominant approach to study the implementation of SR practices (Jamali & Mirshak, 2007) as the relations between enterprises and their Stakeholders become more intense and integrated (Asgary & Li, 2016). For many MSMEs, these relations condition their existence and survival as agents in the chain of value of large enterprises, which makes the direct or indirect implementation of responsible practices more likely (Lepoutre & Heene, 2006).

In a wider sense, the theory of Stakeholders distinguishes and classifies agents in regard to the homogeneity of the interests involved, either in dimensions (internal and external) or as primary and secondary agents (Clarkson, 1995). Primary Stakeholders are those that are fundamental to the enterprise in the market, such as: corporative management or shareholders, employees, clients and suppliers. Secondary Stakeholders involve community, competition, environment and government, with a smaller incidence in the enterprise's activity. In MSMEs some primary Stakeholders have differentiated influence over SR. Employees, clients and suppliers infuse greater sensibility onto owners and directives, even personalizing said relations (Murillo & Lozano, 2006). Likewise, corporate management is usually guided by regulatory compliance on an occupational, environmental and institutional level, encouraging socially responsible codes of conduct.

The local community can also be considered a “primary” Stakeholder, since it can affect the survival of small enterprises that lack the market power of large enterprises (Coppa & Sriramesh, 2013; Lepoutre & Heene, 2006). This condition of economic dependence involves the MSME with the community, favoring a chain of good relations that execute, even unconsciously, socially responsible practices.

In regard to secondary Stakeholders, the literature highlights the rise of environmental management, and the practices associated with the reduction of energy and water consumption, and recycling (Blackburn, 2007; Peña & Delgado, 2013; Walker, Redmond, & Goeft, 2007). As for relations with government or the public sector, some studies point to a scarce predisposition from owners and administrators to interact with the government or its agents, as the main cause of MSMEs’ reticence toward implementing sustainable practices (Brown & King, 1982; Williamson, Lynch, & Ramsay, 2006).

For the objectives of this article, the interpretation of the Stakeholders theory is tested through its assessment and incidence in Barranquilla's MSMEs, in the form of: (i) employees; (ii) corporate management; (iii) environment; (iv) community; (v) value chain (clients, suppliers and competition) and (vi) government/public sector.

The implementation of the Stakeholders theory as an approach to explore the development of responsible practices in MSMEs has been suggested by some studies that highlight its usefulness in smaller enterprises (Campopiano, De Massis, & Cassia, 2012; Nejati, Amran, & Hazlina, 2014). According to the previous statements, the following hypothesis is established: “The perception and execution of RS practices in the Mipymes of Barranquilla is influenced fundamentally by the internal Stakeholders”.

3MethodologyThis section outlines the process of data collection, sample determination and evaluation method. The data section describes the structure of the survey and the characteristics of the sample. For its part, the evaluation method considers the exploratory factor analysis technique to determine and quantify RS practices. Each component is described below.

3.1DataThe data used to evaluate the SR practices in Barranquilla's MSMEs was collected through an in-person poll and email. The poll includes information specific to the enterprise and questions related to the perception and enforcement of social responsibility practices. The revision of literature and consultation of SR indicators from different sources (Donaldson & Preston, 1995; Freeman, 1984; Global Reporting Initiative, 2011; Instituto Ethos, 2011; Vives et al., 2005) allowed the investigators to create and adapt the instrument to the studied context. In order to analyze the size of the enterprises, a classification based on its number of employees was used. The poll was aimed at the owner or manager of the micro, small and medium enterprises of Barranquilla, similar to works from other contexts (Amato, Buraschi, & Peretti, 2016). The universe of enterprises consisted of 41,964 MSMEs enrolled in the mercantile registry of the Cámara de Comercio of Barranquilla in the year 2015.

With a confidence level of 95% and an estimation error of 3%, a sample of 1041 enterprises was obtained. Out of the sample of polled enterprises, 262 questionnaires were discarded due to being incomplete. Therefore, the final number of valid questionnaires was 779, disaggregated in conglomerates by size in micro (469), small (233), and medium enterprises (77) that were distributed in four economic sectors: industry, commerce, services and agriculture. The representativeness of the sample of enterprises was calibrated through the establishment of weighting coefficients according to the defined economic sectors. In order to manage the rate of non-response, replacement enterprises were predetermined.

From the initial questionnaire comprising 83 questions, two were eliminated during the pilot run in response to the recommendations made by some of the directives being polled and the validation of an expert in the matter. The final questionnaire with 81 questions4 has three sections. The first section has nine questions which include seven close-ended questions (5 being multiple choice and 3 dichotomic) and two open-ended questions. These questions configure the structure, economic and organizational characteristics of the enterprise. The second section has eleven questions, non-exclusive, and it contains nine close-ended questions of multiple choice and two dichotomic ones which evaluate the perception and enforcement of SR actions. The third section consists of 61 questions that uses the Likert five point scale (1 – Never to 5 – Always) to measure the execution of socially responsible actions in regards to the Stakeholders: (i) employees (8 questions), (ii) corporate management (7 questions), (iii) environment (10 questions), (iv) community (8 questions), (v) value chain (clients, suppliers and competition) (18 questions), and (vi) government/public sector (10 questions). This type of scale has been widely used in research on SR in MSMEs (Baden, Harwood, & Woodward, 2009). The analysis variables that assess the perception and application of RS practices are specified in Table 1.

Evaluation variables of RS practices.

| Variables | Description | Measurement scale |

|---|---|---|

| Perception of RS | Knowledge that companies have about RS | Dichotomous and nominal type questions |

| Application of RS practices | Execution of responsible actions with different Stakeholders | Likert scale with items measuring RS actions with employees, corporate management, environment, community, value chain, and government/public sector |

To determine and quantify the SR practices regarding Stakeholders in MSMEs in the city of Barranquilla, an analysis was carried out in two stages. The first stage of descriptive analysis characterizes the enterprises and explores the preliminary perception of corporate social responsibility. In the second empirical stage an exploratory factor analysis (EFA) is applied to establish the subjacent dimensions in RS attitudes, therefore determining the influence of Stakeholders in the decision of practicing SR.

The exploratory factor analysis (EFA) is a multivariable technique belonging to the family of methods which involve latent variables also called constructs, factors, or variables which cannot be observed directly. EFA's main objective is to study the structure of correlation between a group of variables, under the assumption that their association can be explained by one or more latent variables or factors. To determine the dimensionality of this matrix, the variables that integrate a factor must be strongly correlated amongst themselves, but weakly so to the variables that make up other factors (Esbensen, 2009; Johnson & Wichern, 2007). Additionally, the EFA can also be used to reduce a large number of variables. Its mathematical specification is as follows:

where F1, …, Fk are common factors, μ1, …, μp single or specific factors (not associated to common factors) and α11, …, αpk the factor loads. These factor loads reflect the relation between the factors and the variables. It is assumed that μ is independent for each variable, and also independent from factor loads (Afifi, May, & Clark, 2012; Mulaik, 2010). It is also assumed that: (i) common factors are not related amongst each other and have a mean of zero and variance of 1; (ii) specific factors are not correlated and have a mean of zero and variance of 1; (iii) common factors are not correlated to specific factors (Mulaik, 2010). Its specification is as follows:where hi2 is known as the commonality of the variable (variance of the variable X explained by common factors) and ψi represents specificity (variance not explained by common factors). The theoretical and applied validation of the explanatory factor analysis in empirical literature regarding SR has fomented its implementation in various works. The classification and diminishing of variables subjacent to the data that explain most clearly the vision of SR in different entrepreneurial contexts is highlighted in literature (Deniz & Cabrera, 2005; Quazi & O’Brien, 2000; Turker, 2008). Following this trend in literature, we test the structural validity and application of EFA as an instrument to measure SR-MSMEs in Barranquilla.4Results

The main results are presented in two subsections: (i) those that characterize companies economically and value the perception of RS practice, and (ii) those obtained from the exploratory factor analysis that measures the most influential Stakeholders of RS between the local MSMEs.

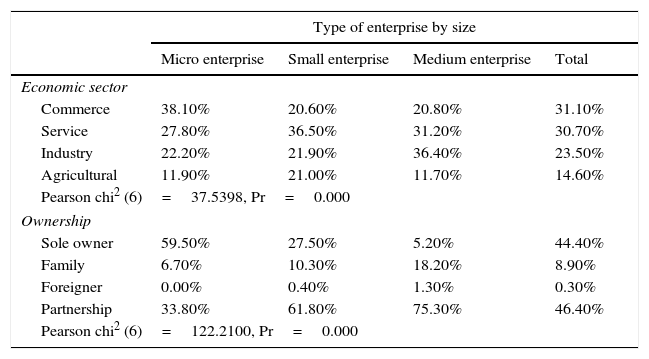

4.1Characteristics of MSMEsThe data in Table 2 reveals the presence of enterprises operating mainly in the sectors of commerce and service (more than 60%) following the sectoral trend of the MSMEs universe from the economic juncture bulletin of Barranquilla in the first trimester of 2016 and the regional report from the large MSMEs survey in 2015 (Asociación Nacional de Instituciones Financieras, 2015; Cámara de Comercio de Barranquilla, 2016). The composition of the enterprises by economic activity is very similar in the different types of enterprise, since more than 50% of micro, small and medium enterprises perform their activity in the sectors of commerce and service. As for the corporative ownership, there is an important concentration of sole owners (44%) and partners (46%). When disaggregated, the majority of microenterprises possess an ownership structure consisting of a sole owner (59%) with a judicial organization of a natural person (50%), in contrast to small and medium enterprises with an ownership structure of partners in more than 60%. Regarding small enterprises, 50% of them correspond to joint-stock and limited companies, while 52% of medium enterprises are stock and joint-stock companies. This judicial composition is coherent with studies on SR which point to a trend in Colombia of the formalization of a judicial person as the enterprise grows in size (Martínez, Torres, & Vanegas, 2007).

Organizational characteristics of MSMEs in Barranquilla.

| Type of enterprise by size | ||||

|---|---|---|---|---|

| Micro enterprise | Small enterprise | Medium enterprise | Total | |

| Economic sector | ||||

| Commerce | 38.10% | 20.60% | 20.80% | 31.10% |

| Service | 27.80% | 36.50% | 31.20% | 30.70% |

| Industry | 22.20% | 21.90% | 36.40% | 23.50% |

| Agricultural | 11.90% | 21.00% | 11.70% | 14.60% |

| Pearson chi2 (6)=37.5398, Pr=0.000 | ||||

| Ownership | ||||

| Sole owner | 59.50% | 27.50% | 5.20% | 44.40% |

| Family | 6.70% | 10.30% | 18.20% | 8.90% |

| Foreigner | 0.00% | 0.40% | 1.30% | 0.30% |

| Partnership | 33.80% | 61.80% | 75.30% | 46.40% |

| Pearson chi2 (6)=122.2100, Pr=0.000 | ||||

Another aspect with the largest relevance to the outline of MSMEs in the city of Barranquilla is the scarce participation in international markets; only 9% of them reports any sort of commercial relation (exportation) with the world. This data reveals the important challenges that Barranquilla's MSMEs face to strengthen their exportation productive capability, and the possibility to venture into international markets.

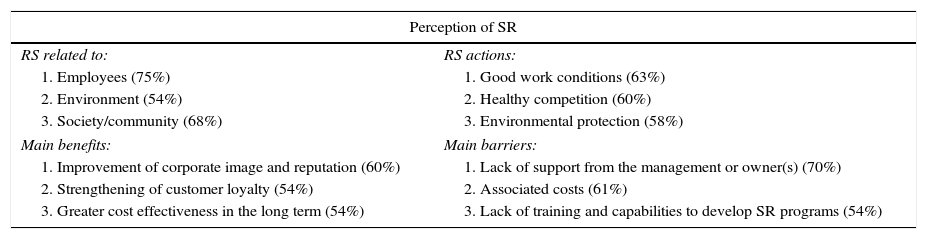

Regarding the general perception and implementation of social responsibility practices in MSMEs, an appreciation of SR related to employees, environment and community was primarily observed (Table 3). This recognition reveals the interest and impact of sustainable development, the importance of talent, and the influence that the community might have on the enterprise's development. However, the “ranking” of answers differs when enterprises are disaggregated by size. The variable most associated to SR in medium enterprises is environment (93%), otherwise, in micro and small enterprises the term of employees predominates with 75% and 71%, respectively. These findings are consistent with some research that points to differences in the perception of SR depending on the size of the enterprise (Gulyás, 2009; Vives et al., 2005).

Summary of SR perception of MSMEs in Barranquilla.

| Perception of SR | |

|---|---|

| RS related to: | RS actions: |

| 1. Employees (75%) | 1. Good work conditions (63%) |

| 2. Environment (54%) | 2. Healthy competition (60%) |

| 3. Society/community (68%) | 3. Environmental protection (58%) |

| Main benefits: | Main barriers: |

| 1. Improvement of corporate image and reputation (60%) | 1. Lack of support from the management or owner(s) (70%) |

| 2. Strengthening of customer loyalty (54%) | 2. Associated costs (61%) |

| 3. Greater cost effectiveness in the long term (54%) | 3. Lack of training and capabilities to develop SR programs (54%) |

As for the main SR initiatives carried out by MSMEs, these are good work conditions, healthy competition and environmental protection (over 60%). Regarding the perception of the benefits and barriers of SR in MSMEs, the main benefits were: (i) improvement of corporate image and reputation; (ii) strengthening of customer loyalty; and (iii) greater cost effectiveness in the long term. The main barriers that hinder their development were: (i) lack of support from the management or owner(s); (ii) associated costs, and (iii) lack of training and capabilities to develop SR programs (Table 3).

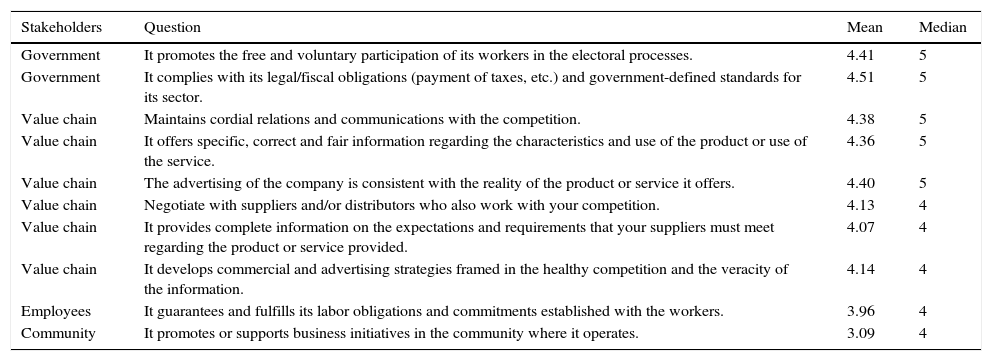

4.2Exploratory factor analysisThe third component of the instrument evaluates the execution of SR practices associated to each Stakeholder in a 60 item Likert scale (1 – Never to 5 – Always). The first results of the main poll offer a descriptive valuation of the mean and median of the items (Table 4) assigning to the categories of government/public sector and value chain (clients, suppliers and competition) the highest incidence of SR practices in MSMEs in Barranquilla. With a mean over 4 Likert points and a median of 5, the practices related to legal or fiscal obligations and fomenting electoral participation, are established as the two most frequent practices for the Stakeholder “government/public sector.” Despite the fact that legal and administrative obligations intervene as stimulators of SR activities in MSMEs, they also generate doubts over their willingness, as pointed out by Vives et al. (2005).

Descriptive evaluation of main RS practices.

| Stakeholders | Question | Mean | Median |

|---|---|---|---|

| Government | It promotes the free and voluntary participation of its workers in the electoral processes. | 4.41 | 5 |

| Government | It complies with its legal/fiscal obligations (payment of taxes, etc.) and government-defined standards for its sector. | 4.51 | 5 |

| Value chain | Maintains cordial relations and communications with the competition. | 4.38 | 5 |

| Value chain | It offers specific, correct and fair information regarding the characteristics and use of the product or use of the service. | 4.36 | 5 |

| Value chain | The advertising of the company is consistent with the reality of the product or service it offers. | 4.40 | 5 |

| Value chain | Negotiate with suppliers and/or distributors who also work with your competition. | 4.13 | 4 |

| Value chain | It provides complete information on the expectations and requirements that your suppliers must meet regarding the product or service provided. | 4.07 | 4 |

| Value chain | It develops commercial and advertising strategies framed in the healthy competition and the veracity of the information. | 4.14 | 4 |

| Employees | It guarantees and fulfills its labor obligations and commitments established with the workers. | 3.96 | 4 |

| Community | It promotes or supports business initiatives in the community where it operates. | 3.09 | 4 |

Likewise, the main practices related to the “value chain” are demarcated by the coherence of advertising, transparent information about the service/product being offered, and good relations with the competition (Table 4). As for the Stakeholder “employees”, the fulfillment of labor obligations is highlighted. In relation to “community”, the most common practices regard the support of the community's entrepreneurial initiatives.

As it has been indicated in some studies, the implementation of responsible practices associated with the legal compliance of the company with the government or public sector, at the labor and environmental level, raises doubts about the voluntary and integral spirit of RS. For this reason, the average of means for the survey data is calculated in order to identify the average pattern of each Stakeholder (Table 5). Although the overall score of all Stakeholders in the Likert ordinal scale is intermediate, the value chain (csc) is maintained as the driver of the RS. However, “government/public sector” does not act as an ally to the development of RS. In particular, there are three Stakeholders who favor the execution of responsible practices: “corporate management”, “community”, “clients, suppliers and competition”. In contrast: “employees”, “environment”, “government/public sector” have lags in the application of RS shares. These descriptive results are tested using the AFE.

The viability and reliability of results from an EFA are more optimal with a big sample, there being different rules and methods to evaluate the adequate size for the sample. Tabachnick and Fidel (2001) suggest that at least 300 cases are required for EFA. For their part, Comrey (1973) suggests different levels of adequacy of the sample: 100 cases is a poor sample, 200 is an acceptable sample, 300 is good, 500 is very good and over 1000 cases it's excellent. Statistically, the Kaiser–Meyer–Okin (KMO) test represents the proportion of the variable correlation table and of the partial correlation table, and it measures whether the sample is large enough to extract the factors in a reliable manner. The variables in the database have a KMO of 0.97, which according to KMO criteria, is excellent. Another requisite to perform a factor analysis is centered on the type of data contained in the variables, which must be measured in an interval. In the particular case of the database used in this study, the objective variables are placed on the Likert scale, which is assumed to be on an interval scale (Ratray & Jones, 2007) even if the scores are discrete.

On the other hand, there are two fundamental aspects with regards to the correlation matrix: the variables must be intercorrelations, but they should not be too correlated (extreme multicollinearity), given that they would cause difficulties in the determination of the individual contribution of each variable to a factor. For that end, the correlations between different variables have been calculated and Bartlett's sphericity test has been carried out resulting significant for the set of variables; therefore, no item is excluded from the factorial analysis.

In this way, the AFE was used to create a factor structure among the RS attributes. For the analysis, the main factor method was used as the factor extraction method, due to the non-normal nature of the Likert scale. One of the fundamental aspects of a good factorial model is the adequate choice of the number of factors, since the overestimation or underestimation of the number of factors retained may lead to substantial errors that would alter the solution and interpretation in the results of the AFE (Hayton, Allen, & Scarpello, 2004).

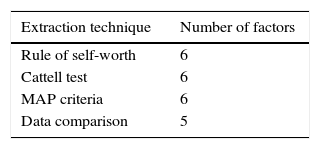

This work uses four criteria for the determination of the number of factors, compared to other works that use a smaller number of criteria (Deniz & Cabrera, 2005; Turker, 2008). The criteria used are Keizer's own value rule, Cattell's test, the minimum average partial (MAP) and the data comparison technique by Ruscio and Roche (2012). The application of these criteria and the consideration of the literature that recognizes in the overestimation less damage with respect to the underestimation in the number of factors (Beavers et al., 2013), allowed to extract 6 factors that explain 93% of the total variance (Table 6).

To simplify and clarify the structure of the analysis, the oblique rotation method is used, based on the assumption that the factors may be correlated. Once the load of the 60 variables in the different factors were examined, those with weights greater than 0.5 were extracted, resulting in a factorial structure of 37 variables (items) and six different factors with their own values greater than 1.0 that capture 96.62% of the variance of the 37 items. Table 7 shows the new configuration of AF retained variables is classified into six factors called: Factor 1 “good internal practices” which includes legal and extralegal actions in favor of employees, as well as good governance practices at internal, environmental and community levels. Factor 2 “good practices suppliers” includes those actions focused on the use of environmental and labor criteria for the selection of suppliers. Factor 3 “good community practices” groups those practices aimed at improving the community where it operates. Factor 4 “good governance practices” focuses on joint actions with the government for the realization of social and civic initiatives. Factor 5 “good business practices” brings together those advertising strategies that highlight consistent and correct information in advertising programs. Factor 6 “economic relations with the government” adopts those actions concerning the participation of calls for public contracting and economic relations with local and/or national government.

Factor structure of RS variables and factors.

| Variables | Stakeholders | Factors |

|---|---|---|

| 17 | 6 items employed, 5 corporate management, 2 environment, 2 community and 2 value chain | 1. Good internal practices |

| 4 | 4 items value chain | 2. Good practices suppliers |

| 3 | 3 items community | 3. Good community practices |

| 3 | 3 items government | 4. Good governance practices |

| 7 | 7 items value chain | 5. Good business practices |

| 3 | 3 items government | 6. Government economic relations |

Finally, the factor composition was complemented with an ungrouped analysis to identify the distinctive influence of the Stakeholders. For this, the variables common to each Stakeholder were organized, given their factorial loads, and the respective means were calculated. A mean of ≥0.70 was set as the influent value of RS (Table 8). Thus, the results of the scale based on the factorial analysis present two changes on the drivers of RS regarding to the descriptive results identified in Table 5. In particular, “employees”, “environment”, “community”, stand out as the Stakeholders of greater explanatory contribution of the execution of responsible practices of the MSMEs of Barranquilla. For their part, “corporate management”, “value chain”, “government/public sector” are less influential. The new configuration of variables and factors as a function of factorial weights explains the variation of results between the two tables, given the restriction of the influent value of RS (≥0.70) and the elimination of weakly related variables in the descriptive evaluation. In both analyzes, the Stakeholders “community” prevails as the driver of RS, while “government” maintains a passive condition.

In general terms, micro, small and medium-sized companies in the city of Barranquilla emphasize their corporate social responsibility in strategies aimed at the well-being of employees, care and preservation of the environment, and actions aimed at good understanding with the community. There are few initiatives aimed at corporate management, value chain and government/public sector. Greater culture and training around the responsible practices of micro and small enterprises in Barranquilla would contribute to generate an environment conducive to raising the social awareness of these organizations.

5Discussion of results and conclusionsThis paper investigates the empirical relationship of the RS with the MSMEs of the city of Barranquilla, based on the actions carried out and the influence of the Stakeholders. The results suggest that certain practices associated with certain Stakeholders act as drivers of SR in the local MSMEs. In this sense, the first question of the investigation has to do with the economic characterization that identifies the local MSMEs. As evidenced by the data obtained from the fieldwork, there is a greater presence in economic sectors of commerce and services; proprietary concentration in few owners; under export performance and an average age of 13.4 years. The largest single owner and family owner presence in microenterprises (66%) and companies in SMEs (55%), coupled with the age of the companies (6 micro and 17-years-old SMEs) as well as the smaller exporting vocation of microenterprises, seems to influence the heterogeneity of the knowledge and expansion of RS among the MSMEs of Barranquilla. The smaller participation of microenterprises in international markets with respect to SMEs, mainly determines the learning and execution of responsible practices already standardized in other contexts that demand in the supply chain the compliance with sanitary, environmental, labor standards and other actions close to RS.

The second question of the investigation was to identify the degree of knowledge and implementation of responsible practices that MSMEs experience. In this sense, the results show a greater knowledge of RS in SMEs with ownership structure of companies (89%) compared to microenterprises with single or family power (68%); highlighting the separation of ownership and control at the corporate level as a way to favor the recognition and development of socially responsible practices in the SME, as is evidenced by the work of Herrera et al. (2016). There is also a positive relationship in SMEs, between seniority and understanding of the RS (87%), expressing in the time an important factor for their understanding, which suggests that RS is developed over time and is assimilated and experienced by company directives as a strategy to promote and integrate SR policies in the management of the company.

It seems that owners and managers of MSMEs are aware of the potential of some responsible actions and the general perception reveals the interest in deepening their participation. The vision of the improvement in the corporate image and profitability in the long term with 60% and 54%, respectively; as well as the recognition of the importance of performing RS actions (51%) support our appreciation. In the same way, the implication is larger as the size of the company increases in line with the literature (Baumann, Wickert, Spence, & Scherer, 2013; Niehm, Swinney, & Miller, 2008) which indicates the development and execution of RS shares according to business size.

The third question of the investigation explores the most influential Stakeholders in the execution of responsible actions of MSMEs. Following the methodology of other papers (Quazi & O’Brien, 2000; Russo & Tencati, 2009; Turker, 2008) the AFE was applied to determine the factorial structure underlying the set of variables that evaluate RS actions and group them according to patterns that empirically explain the execution of responsible practices. It is found in employees, environment and community, the most influential Stakeholders of the RS in the Mipymes of Barranquilla; thus refuting the initial hypothesis, since it is the external Stakeholders that show a greater presence in the RS activities of the local MSMEs. These results are congruent with those obtained by Murillo and Lozano (2006), which show in the smaller companies a greater commitment by the community and those of Herrera et al. (2016) that indicate in the environment the execution of several socially responsible actions. Likewise, we can observe in the size of the companies some Stakeholders with differentiated influences of the RS. In addition, the role of the community in the MSMEs as an important actor in the RS, in line with the findings of Coppa and Sriramesh (2013) and its proposal to address it as an “internal” Stakeholder, given the commercial and cultural link next.

On the other hand, by breaking down companies by size, the presence of corporate management, community and value chain as the main Stakeholders in the microenterprise segment that drive the development of responsible practices. The important presence of economic sectors of commerce (38.9%) and services (28.36%), coupled with the large concentration of ownership of a single owner (59.28%) may be demarcating the distinctive actions of RS practices in microenterprises, and the economic priority of owners to survive in the market. SMEs, on the other hand, have better indicators for the rest of Stakeholders, with the exception of “government/public sector”. In particular, “government/public sector” does not seem to be a good driver of SR practices in local SMEs. In general, it is observed in the MSMEs of Barranquilla the presence of specific actions or activities of SR little integrated or related to formal SR strategies and influenced to a greater or lesser extent by certain Stakeholders. These findings are consistent with other papers (Jenkins, 2004; Perrini, 2006; Raynard & Forstater, 2002; Roberts, Lawson, & Nicholls, 2006) that point out in SMEs the execution of responsible informal actions associated with SR practices intuitively.

With regard to theory and types of Stakeholders, local MSMEs seem to emphasize their relations mainly at the contingent level (Friedman & Miles, 2002), transactional (Freeman, 1984), instrumental (Donaldson & Preston, 1995) and in the internal–external dimensions (Mitchell et al., 1997). The frequent operations, cultural and contextual aspects of MSMEs with their community; business to business orientation; the concern to survive and try to maximize the benefits, as well as the related relations with different Stakeholders, configure the nature and approach of SR practices linked to this type of agents. However, the recognition of voluntarily establishing codes or manuals of good behavior in these companies (97%), contrasts with perceived barriers to their development. In fact, the lack of owner support and corporate management (70%) associated costs (61%) and the lack of training to develop SR programs (54%), constitute the main obstacles to be revolved. These findings reveal that the establishment of SR programs in MSMEs requires strategic alliances with other agents, such as the government, large companies, academic institutions, etc., to strategically promote and support responsible initiatives in MSMEs. Additionally, it is observed that managers of micro and small enterprises are less likely to establish programs and execute RS actions compared to medium-sized enterprises that report greater interest in undertaking and executing such a program. These results may explain the narrow view on social responsibility experienced by micro and small enterprises.

In addition to the results and contributions of the present study, the limitations are noted. The first is related to the subjective perceptions of the respondents and the impossibility of establishing the existence of response bias, mainly in microenterprises. The second limitation has to do with the absence of sufficient and reliable secondary data, which justified the collection of primary data. The third limitation is the lack of financial information in the survey that will evaluate the execution of SR programs in relation to the investment made. Therefore, it is recommended to carry out studies that empirically evaluate the economic investment that MSMEs have to undertake RS programs. Finally, with the application of the AFE to the MSMEs, a large part of environmental actions (80%) was excluded, which is anomalous. The explanation for this phenomenon can be found in the large volume of responses of micro-enterprises that differ significantly from small and medium-sized enterprises. Specifically, the AFE reveals in micro-enterprises a weak presence of environmental actions in their productive and business processes. This lack of concern for the environment is consistent with previous studies indicating resistance and skepticism of environmental actions in microenterprises (Gadenne, Kennedy, & McKeiver, 2009; Revell & Rutherfoord, 2003), in contrast to some studies that find a favorable link between the SME and the environment (Gallardo & Sánchez, 2014; León et al., 2015).

In summary, the presented results offer some ideas that contribute to the knowledge of the RS-MSMEs relationship in developing countries, providing new empirical evidence on RS actions in smaller companies, and that in any case should be interpreted with caution. In particular, the micro, small and medium enterprises of the city Barranquilla experience a certain level of familiarity with the practices and awareness of the RS; especially in actions related to employees, environment and community; and to a lesser extent, corporate management, value chain and government/public sector. However, there is a weak perception and unwillingness among owners and managers to undertake integrated social responsibility programs (64%), as well as the formalization of those actions underlying the operational function of the company with an impact on responsible practices. Similarly, issues such as the lack of training and skills to develop RS programs stand as barriers to adopting formal social responsibility measures.

FundingThis work was financed within the framework of the research project “Characterization and evaluation of social responsibility in micro, small and medium enterprises of the Caribbean Region of Colombia”, resolution No. 003247 of the internal call “Caribbean Impact” of the Universidad del Atlántico, 2014.

Conflict of interestsThe authors declare that they have no conflict of interest.

The authors are grateful for the comments and recommendations of professors Sergio Afcha and Antonio Vives, as well as the collaboration of officials from the Cámara de Comercio de Barranquilla. Finally, we thank the anonymous reviewers for their comments and suggestions.

The paper “Micro, Small, and Medium Enterprises. Around the World: How Many Are There, and What Affects the Count?” by the World Bank, reveals the existence of 125 millions of formal MSMEs throughout 132 economies in the world; of which, 89 millions exist in developing countries. There are around 31 MSMEs for every 1000 habitants.

In Colombia, the 905 law from 2004 classifies MSMEs based on their number of employees and on their assets. In terms of the number of employees, microenterprises are those with 10 employees or less, small enterprises have between 11 and 50 employees, and medium enterprises between 51 and 200 employees. According to data from the Confederación Colombiana de Cámaras de Comercio (Confecámaras), in 2015 Colombia had 1372.923 MSMEs, out of which 1273.017 (92.72%) are micro enterprises, 79,926 (5.82%) area small enterprises and 19,980 (1.46%) are medium enterprises.

Barranquilla is the city with the highest rate of entrepreneurial activity in the Caribbean Region of Colombia and fifth in the country, according to the “Región Caribe 2012–2013” report from the Global Entrepreneurship Monitor (GEM). It contributes with the 4.3% of the National GDP and as of June 2016, it has 41,274 MSMEs enrolled in the Cámara de Comercio de Barranquilla. Nationally, it is the fourth city with the largest amount of MSMEs. The city has a population of 1,386,865 habitants and is considered the most important city of the region.

Link to the virtual survey https://docs.google.com/forms/d/e/1FAIpQLScUiPmdGek5gu1-KuvVcYBnoeQgCIZk0AwmFeL-47zqdtK-kA/viewform.

www.publicationethics.org.