In recent years, corporate social responsibility (CSR) has attracted much interest in both the academic world and the professional, proof of this are many studies on this topic that have been made. However, most studies of CSR focus on larger organizations, with few studies focusing on small and medium enterprises (SMEs), and even less on family SMEs. For this reason, the objective of this research is to determine whether there are differences in orientation towards CSR between family SMEs and non-familiar ones, and if this fact can be influenced by gender and the level of formal studies of the manager, among other factors. The results, on a sample of 123 SMEs, indicate that family SMEs are more socially responsible than no familiar ones.

En los últimos años la Responsabilidad Social Corporativa (RSC) ha suscitado gran interés entre académicos y profesionales, y muestra de ello son los numerosos estudios que sobre dicha temática se han realizado. Sin embargo, la RSC sigue estando asociada a las grandes empresas, siendo muy pocos los estudios centrados en las pequeñas y medianas empresas (pymes), y menos aún en las pymes familiares. Por este motivo, el objetivo del presente trabajo es conocer si existen diferencias en la orientación hacia la RSC entre las pymes familiares y las no familiares, y si este hecho puede estar influenciado por el género y el nivel de estudios del gerente, entre otros factores. Los resultados obtenidos sobre una muestra de 123 pymes ponen de manifiesto que las empresas familiares son más responsables socialmente que las no familiares.

Nowadays, business organizations play a decisive role in society, especially in the field of globalization in which the effects are multiplied exponentially in many dimensions, not only economic but also social and environmentally (Bajo Sanjuán, González Álvarez, & Fernández Fernández, 2013). Unfortunately, in the last years many companies have been characterized by business scandals and the benefit based on short-termism, so that some companies have looked for short term benefit with no regard to ethically irresponsible actions or worrying about social and environmental impact which could result in being lengthy and costly in the long term (Fraile, 2012).

Thus, for example, behaviour such as that of Union Carbide with the explosion of its chemical plant in Bhopal, the failure of Enron, the scandal of Nestle's powered milk of, the spills of Exxon Valdez on the coast of the Pacific, or the Nike case of the balls sewn by children from the third world countries. Together with the late response of many pharmaceutical companies with regard to the pandemic of AIDS in Africa and the double morality of fast food chains and the tobacco industry, citizens have lost their confidence in public and private institutions (Torras, 2009).

Besides, due to the emergence of Internet and social networks people can access information immediately, both locally and globally (Fraile, 2012). For this reason, costumers are more aware and behave in a demanding way starting to transfer their demands towards the brands to make them take responsibility for their actions (Córdoba, 2008). Consequently, companies have had the need to include good government practices to carry out their activities producing the implement of Corporate Social Responsibility practices (hereinafter CSR) (Herrera Madrueño, Larrán Jorge, Lechuga Sancho, & Martínez Martínez, 2014). However, the CSR measures are not as a corporate toll, which needs to be paid because it is fashionable, but it must be treated as a factor that must be integrated and aligned along with business strategy. Definitely, that is, doing things well (Córdoba, 2008).

It should be said that due to the importance that CSR has acquired recently, an area of interest has been created among the academics and researchers (Herrera et al., 2014). Nevertheless, studies have been centered on big companies, with a lack of attention to small and medium sized enterprises, and to family enterprises and even rarer the ones of larger sized family firms. For this reason, current analysis tries to know how larger sized family firms have an orientation to CSR, so we will analyze if there are differences among the behaviour of family firms and non-family firms, pointing out which is mostly oriented to CSR. So, the goal is to find out if sized family enterprises are more socially responsible than the non-family enterprises.

Regarding the structure of this project to achieve our goal, first a revision of the literature has been made to introduce CSR more specifically to later continue by looking at this concept in relation with family enterprises, what will result in the statement of the hypothesis. Subsequently, the methodology is exposed and the results of the analysis will be made and finally we will contrast them with the main proposals of the hypothesis.

Corporate social responsibilityThe current financial crisis around the world has increased poverty and unemployment levels in many countries. Along with this, hard adjustment measures have been taken by many enterprises, there is also a higher awareness towards social problems risen by the access to new information technologies, which has led to reports of situations considered unacceptable. In this sense, the implementation of CSR policies has led to a great progress for many enterprises (Ruizalba Robledo, Vallesprín Arán, & González Porras, 2014).

The concept of CSR is related to terms such as: good corporate government, business ethic, code of conduct, sustainable development, among others. Such concepts cover a great variety of initiatives, so there is not a universal definition, but it has many definitions. The most accepted is the one of The citizens’ Network-Commission Green Paper (2001) which defines CSR as ‘the volunteer integration, by the hand of enterprises, of social and environmental issues in their commercial transactions and their relationship with their interlocutors’ (Juaregui, 2012:30) Despite this definition, CSR is an extremely complex concept and very difficult to use in the corporate environment (Marín et al., 2014), for this reason, it is usually defined as a multidimensional concept (Gémar & Espinar, 2015) which consists of the following dimensions:

- •

Economic dimension: it refers to the development of enterprises by means of ethical management of the business, and it also refers to the accomplishment of laws and codes of good government (Suárez, 2013). Then, it involves the development of honest business practice. To offer safe and good quality products by means of innovation and improvement of production processes (García & Rodríguez, 2011).

- •

Social dimension: in this dimension we include the following practices: hiring people in danger of social exclusion, improving employees living standard, involvement with the creation of employment, fomentation of the staff's professional development, maintenance and improvement standard of living of people and supporting social issues (Ruízalba et al., 2014:47). In the same way, social dimension refers to help the staff to conciliate their professional and social life, to protect them in health and work safety and to avoid discrimination and violation of human rights (Mababu, 2010).

- •

Environmental dimension: it refers to the impact that companies can have with their actions on nature, ecosystems, the Earth, air and water (Cabeza García, Sacristán Navarro, & Gómez Ansón, 2014). In this sense we can point out that eco-efficiency and environmental information of the company determine its level of implication and respect to the environment (Suárez, 2013).

Summarizing we can state that CSR is a new frame of business and organization management, which implicitly carries corporate ethic and it is considered as ‘the correct way of acting’ (Suárez, 2013), having in mind the responsibilities or duties that corporate management should have with all their stakeholders (López Davis, Marín Rives, & Baixauli Soler, 2014). Enterprises, specially leaders and managers, should be aware of accomplishing the expectations of shareholders and they should be also aware of the set of social acts which are needed to achieve success (Kliksberg, 2012).

Regarding the concept of stakeholders, it is based on the classical definition offered by Freeman (1984) (quoted in Caballero, 2009:67), “any group or individual that can affect and can be affected by the achievement of the aims of the organization”. For this reason, working in CSR is to analyze, manage and optimize the relations of the enterprise with all the stakeholders who are affected because of their activity (Almela, 2009), for a greater transparency the main stakeholders are presented in Fig. 1.

Regarding the previously mentioned, to manage a company responsibly offers several advantages as is reflected in Fig. 2.

Advantages of an active policy of CSR.

The most important benefits result from the improvement of the image of the company brand and from the increase of its corporate reputation (Almela, 2009; Colle et al., 2014; De la Peña, 2012; Gémar & Espinar, 2015; Kang & Hustvedt, 2014), getting competitive advantages (Marín & Rubio, 2008a). Besides, being responsible companies will contribute to a greater fidelity and commitment of the staff, improving their motivation and work environment, resulting in satisfied and loyal customers (Kang & Hustvedt, 2014).

In this line, Marín and Rubio (2008b) point out that the initiatives in CSR involve a recognition and an estimation of the stakeholders, which has an impact on the improvement of its relative position, regarding to the competence, showing the influence of CSR in the competitive success of enterprises and according to Gémar and Espinar (2015) without debilitating the profit of the company.

Corporate social responsibility in family SMEsFirst, it is necessary to introduce family enterprises studying their importance, concept, and particular features characteristic to them, once having seen the concept we will give more details on CSR.

The importance of family enterprise in the economy and the business world in general is unquestionable, as nowadays these enterprises are the most extended sort of business in any economic structure (Ruizalba et al., 2014). Consequently, family enterprises are the determining factor in creation of wealth and the basic engine of the regional productive economy. They represent a commitment to their territorial community through continuity, which is demonstrated by a higher degree of investment and even employment together with social responsibility (Blanco, 2014).

According to the Family Enterprise Institute, in the European Union more than 60% are family enterprises and employ more than 100 million people whereas in Spain there are more than 2.9 million of family enterprises, representing 85% of total companies. Besides, they employ 13.9 million people and the total amount of its invoice corresponds to 70% of the Spanish GDP (Blanco, 2014; Claver Cortés, Molina Manchón, & Zaragoza Sáez, 2015; Ruizalba et al., 2014).

To differentiate family enterprises from non-family enterprises, it is necessary to point out that a family enterprise is an enterprise in which the family exercises the ownership either of property or because of the function that it has in its government or management (Rojo Ramírez, Diéguez Soto, & López Delgado, 2011). Family enterprises are mainly characterized by the family factor, which conditions the decisions taken in the enterprise and its development (González, 2010). Therefore, affective and emotional ties make relations more intense (Martín, 2011). For this reason, the goal of a family enterprise is continuity through family harmony (Arteche & Rementeria, 2012).

However, family enterprises are becoming more professional in general, as is shown by the study carried out by PWC (2014). In this study, the priorities of family enterprises have been quantified, focusing on ensuring the future of the enterprise in the long-term and improving the profit. Following these priorities, it is important to highlight: attracting qualified people, rewarding the staff properly, having a greater innovation and professionalizing the business. Therefore, in recent years, there has been an increase in the development and the success of family enterprises.

However, although family enterprises are becoming more professional, it is necessary to avoid the informality of familiar treatment, a feature of family enterprises moving to business environment (Martín, 2011). For this reason, it is important to have preventive mechanisms in order to anticipate and manage potential conflicts and other problems efficiently, to guarantee the survival of the enterprise (Monreal Martínez, Sánchez Marín, & Meroño Cerdán, 2010). In more detail, we refer to the Family Protocol, that is a familiar statute in which we find the rules that regulate family enterprises (González, 2010). It includes issues related to money, role in the family enterprise, the inclusion of new members, succession, among others (Tápies, 2012). It is also necessary to talk about family council as governing body, it is the body that regulates the proper function of family enterprises and, in particular, the relationship of the family with their business and other activities related to the company or to the family wealth. By contrast, the administration council represents the family owners and non-owners’ interests, and it tries to regulate business judgement (Arteche & Rementeria, 2012).

Regarding CSR in family enterprises, firstly it is necessary to state that the concept of CSR was born in relation with big multinational companies, but over the years, and given its economic importance, it has been necessary to move the concept, practices and instruments to family enterprises, as they represent the large majority of the European companies (Campos, 2009).

Although in many cases family enterprises exist constraints in terms of resources (financial, human, etc.) and, consequently, they present some resistance to adopt CSR measures, they also have numerous advantages. In particular, family enterprises have greater flexibility when they have to meet the requirements of their customers, they have greater involvement on behalf of the staff concerning the company's progress, they also give greater emphasis to personal relationships. Besides, as they do not have developed formal structures, they are less complex and it makes them more based on personal relationships than big companies (Argandoña, 2008).

Family enterprises tend, mainly, to maintain control of the enterprise under family ownership, to preserve the culture and personal values (Cabrera, 2012), the reputation and the recognition of their costumers, the local community, and consequently, the family enterprises will probably be more involved in considering and developing long-term ties with their stakeholders than big companies (Argandoña, 2008).

Shown below, in Fig. 3, we have synthesized the main advantages that family enterprises have by integrating CSR in their management, and how it positively affects these companies.

Advantages and benefits of CSR in family enterprises.

The main concern of family enterprises is the survival of the organization (Argandoña, 2008). Due to this, family enterprises are associated with particular values and behaviour such as staff respect and protection, quality of the products, local involvement, reputation concern about both corporate and family, long-term orientation, importance of tradition and family values, as well as austerity and integrity (Cabrera Suárez, Déniz Déniz, & Martín Santana, 2011). In this regard it is worth mentioning that family enterprises are more cautious about the income earned, as they associate that money of the company is also money of the family. Similarly, they control the expenses more, avoid falling into debt and consequently they do not feel obliged to fire employees in times of crisis, avoiding risks, worrying more about their staff to guarantee the survival of their company and its continuity in future generations (Martín, 2015).

Besides, for family owners, it is essential to maintain the social-emotional wealth of the company, for this reason it is more likely for family enterprises to participate in social compliance than non-family enterprises (Cabeza et al., 2014). In fact, from a theoretical point of view, family enterprises are more concerned about the aspects related to CSR than nonfamily enterprises, due to the fact that family enterprises have an amount of intrinsic conditions that facilitate the integration of CSR in the day-to-day management (quoted in Herrera Madrueño, Larrán Jorge, Lechuga Sancho, & Martínez Martínez, 2013).

Nevertheless, there are also arguments and evidences that the family aspect of the enterprises affects the adoption of CSR actions negatively. For example, a family enterprise that has a great amount of money invested in the company is usually more concerned about return of investments, to reassure the viability of the company and its continuity for future generations, than about social and environmental issues (Cabeza et al., 2014).

Thus, a change of structure among companies is necessary, especially among family enterprises, in order to make them familiar with the concept of CSR, and to make them understand that CSR activities are not an expense without counterpart but a way of managing the company in a responsible way to provide medium and long-run benefits (Campos, 2009). To do this, they must communicate by means of the publication of CSR reports and memories to their stakeholders. The memory of the CSR is considered as an instrument that is used by organizations to disclose their efficiency and economic, social and environmental impact. In fact, the companies that publish sustainability information through reports, are the ones that mostly implement CSR practices (Herrera et al., 2013).

Attitude and strategy of the family enterprises towards their staffIn this respect it must be emphasized that due to the dimensions and the limitation of resources of the family enterprises, their policy of corporate responsibility is mainly manifested at an internal level, that is, to improve their policy on human resources, energy saving and incentives for workers (Mababu, 2010).

For example, proceedings such as the maintenance of the staff, conciliation of working and family life, equal opportunities, taking advantage of the wealth of equality and sociocultural mixing, having a fluid communication and making them participate in decisions. Moreover, developing the professional skills for adequate performance, knowing how to improve the own development of the workers, investing if necessary in personal progress. All these actions, among others, affect the organization positively, as they create a good working environment, achieving a motivated and encouraged workforce, who will be committed with the company and its proper functioning (Campos, 2009; Sánchez Vidal, Cegarra Leiva, & Cegarra Navarro, 2011).

In this direction, it is important to highlight that family enterprises retain their employees longer than non-family enterprises, even in times of crisis. It is so because of the good working environment and the culture of commitment common in these companies, since they are more concerned about their staff, invest in their training and in this way they retain their skills too (Martín, 2015).

Likewise, the study carried out by Monreal et al. (2010) and later by Carrasco and Sánchez (2014), agrees that family enterprises apply equitable and professional criteria in the management of human resources. Particularly, family enterprises, to select and promote their employees, consider the specific requirements and merits regardless of their family relationship. Regarding the policies of training, family enterprises consider not only short term elements but also consider the flexibility of the labor force to prepare it for the possible changes and future adaptations.

It is important to remark that the training increases the involvement and motivation of the staff with the company, as well as lining up the interests of both sides. This fact is very important for family enterprises, so that the owners who have invested a great part of their personal heritage in their business are aware of the importance of having qualified employees to maintain their company in the long run thanks to the competence of their human resources. Afterwards, we could reach to the conclusion that training in family enterprise should be greater than in the non-family enterprise (Carrasco & Sánchez, 2014).

Consequently, taking into consideration the lack of agreement of several studies, but predominating the evidence in favor of a major concern about training and their employees on behalf of family enterprises than non-family enterprises, we could state this hypothesis:H1 Family enterprises are more concerned about training and employees than non-family enterprises.

In this aspect it is important to highlight that family enterprises due to their size and their affective ties produced in the companies make staff feel more integrated in the community where they develop their activity. Besides, they see themselves more affected by social pressures so we could induce that they are more involved in preserving the environment and helping to improve living standards in general, since the increasing lack of natural resources and the impact of environmental abuse make protection and sustainability of the environment occupy an essential role in the success strategies of the companies (Fraile, 2012).

According to several authors, family enterprises tend to adopt more proactive environmental strategies than non-family ones. The main reasons are because family enterprises want to avoid the risk of being considered irresponsible by citizens. Besides, they are more sensitive regarding local pressure on environmental issues due to the low dependency on financial incentives in the long run which promote environmental responsibility (Garcés Ayerbe, Rivera Torres, & Murillo Luna, 2014).

Likewise, as the objectives of family enterprises go beyond profit maximization, those are more prone to have more strength and less weaknesses towards CSR (Herrera et al., 2014). Therefore, family enterprises are in favor of protecting the environment due to their social and corporate responsibility (Garcés et al., 2014). Consequently, they are actively involved in promoting ecological values in their actions (Cabrera Suárez, Déniz Déniz, & Martín Santana, 2002), which makes us state the second hypothesis:H2 Family enterprises are more socially responsible than non-family enterprises.

Family SMEs can have different orientations towards CSR. This is due to the existence of multiple factors which may have an influence on their behaviour. On account of this, we think about whether the gender of the owner or manager and the training level should also be considered as important factors towards having more responsible behaviour.

As regards gender, several authors such as Hazlina and Seet (2010) point out the existence of evidence which suggests that women are more ethical and socially responsible, having a greater philanthropic instinct. Unlike men, who are associated with more reactive behaviors and focused on goal achievement. Therefore, male gender is attributed a more economic approach. Besides, family enterprises run by women do not note the lack of financial resources as a possible reason not to introduce sustainable practices in the enterprise as opposed to men (Herrera et al., 2014).

Likewise, leading women show a greater tendency than men to cooperation, achievements based on teams, support and long-lasting relationships as well as a greater sentiment. Then, a wider gender diversity could give different points of view when making decisions as well as ease the relationships with stakeholders (Cabrera et al., 2011), thanks to a more diplomatic and participative female way of management (Vázquez & López, 2010). Therefore, a female point of view in enterprise management may contribute to considering some other aspects of reality and better anticipation of the consequences of actions in the long and medium term (Chinchilla & Jiménez, 2013).

Regarding the training level, research done by Herrera et al. (2014) indicates that managers of family SMEs with a university education have a greater motivation to consider the pressure made by stakeholders and give more importance to ethic values. On the other hand, Carrasco and Meroño (2011) point out that managers with a university education increase work motivation in the position of work of family SMEs as opposed to those without university studies.

The fact of having a university education does not mean in itself that a person will be ethical and responsible, but shows some link, since, as Pérez (2010) points out, universities push for development as well as impulse social transformation at the same time. It is through them that it seeks to ensure the training of competent professionals on the base of ethical principles that guarantee sustainable and social development. In particular, there is a major presence of CRS subjects in curriculums related to enterprises and marketing. This fact is extremely important, owing to the fact that these students will be the future enterprise managers (Larrán Jorge, Andrades Peña, & Muriel de los Reyes, 2014).

In short, following the previous reasoning and studies, we set out the following hypothesis:H3.1 SMEs women managers conduct more socially responsible management than male colleagues. family SMEs managers with a university education carry out more socially responsible management than colleagues without a university education. family SMEs female managers with a university education carry out a more socially responsible management than male colleagues with university education, as well as those, either men or women, without a university education.

This study intends to know whether family SMEs are more socially responsible than non-family ones. To achieve this goal a structured survey has been used, which was provided to family and non-family SMEs managers at the end of a course about Efficient Management of Enterprises, which took place in Alicante, in March 2015. During that course, the surveys were given to the total number of 142 participants in the course, achieving a total of 123 valid surveys from managers of enterprises located in the southeast of Spain.

Regarding the design of the survey, firstly, the commercial activity of the enterprise has been asked to know whether the reason why enterprises which are more involved with socially responsible practices could be linked to their activity sector. As well, the community which the enterprise belongs to has been asked, in addition to the size of the enterprise, depending on the number of employees and the annual turnover, to discard those enterprises which are not SMEs. In the same way, the personal characteristics of the manager have been measured (gender and level of studies) to know whether these variables influence a more socially responsible behaviour from the enterprise they run.

On the other hand, to know if a training policy of human resources is being carried out and if the enterprise carries out actions related to CRS, two 10-point grading Likert scales have been used. And lastly, questions related to the family condition of SMEs have been established, differentiating if the company is a family one. In addition, in the case of family SMEs, it asks about the existence of protocol and family council.

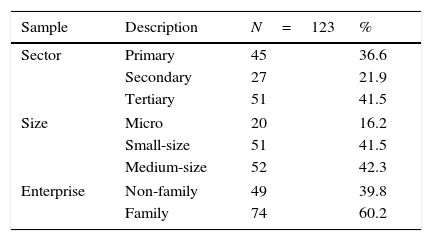

With respect to the sample group, Tables 1 and 2 show its characteristics. If we analyze the business sector we can notice that companies in the tertiary (41.5%) and primary sector (36.6%) predominate over the secondary sector (21.9%). In the same way, all the companies in the sample are SMEs, in particular, medium-sized (42.3%) and small-sized (41.5%) enterprises predominate, to the detriment of micro-enterprises (16.2%). As regards family condition of SMEs, family enterprises (60.2%) predominate over non-family ones (39.8).

Characteristics of the sample depending on the manager.

| Sample | Description | N=123 | % |

|---|---|---|---|

| Autonomous communities | Castilla la Mancha | 31 | 25.2 |

| Valencian community | 48 | 39.0 | |

| Balearic Islands | 5 | 4.1 | |

| Murcia region | 39 | 31.7 | |

| Gender | Male | 75 | 61.0 |

| Female | 48 | 39.0 | |

| Education | Non-university | 59 | 48.0 |

| University | 64 | 52.0 |

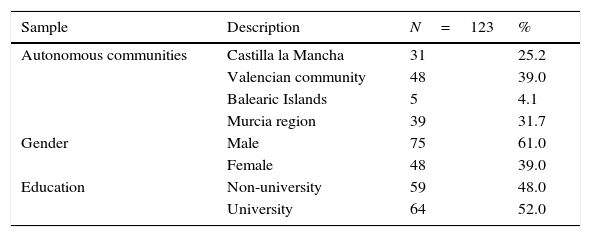

In this context, the sample SMEs are mainly from the Valencian Community (39%) and the Murcia region (31.7%). Even so, there is also presence of SMEs from Castilla la Mancha (25.2%) and, to a lesser degree, from the Balearic Islands (4.1%). As regards the managers’ gender, men (61%) stand out compared to women (39%). While focusing on training level, there is a slight majority of a university education (52%) as opposed to non-university (48%) as shown in Table 2.

In conclusion, the sample is characterized by enterprises from the Valencian Community (39%), medium-sized (42.3%) in the tertiary sector (41.5%) and family ones (60.2%), which are managed by men (61%) with a university education (52%). To sum up, it should be noted that if we only consider the family enterprises in the sample, we can also highlight that those enterprises are characterized by the lack of family protocol (63.5%) and, even to a higher degree, of family council (93.2%).

Results analysisAt this point, we are going on to analyze the results obtained from the survey, verifying if the hypothesis formulated in this study are accepted or rejected. In order to do this, the statistical software SPSS, version 20, has been used. First of all, it should be pointed out that both 10-point grading Likert scales, the one that measures employees training as the one measures the CRS, the last one being an adaptation of the one suggested by Deshpandé et al., show high reliability and have been successfully used in other studies.

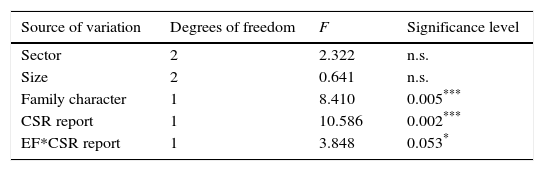

The hypothesis test has been conducted using Analysis of variance (ANOVA), which is a statistical technique, to compare the median of more than two data sets (Martín Castejón, Lafuente Lechuga, & Faura Martínez, 2015). Firstly, CRS has been considered as a dependent variable while the independent variables considered are the sector, size, family condition and the existence of a CSR report in the company. Results shown in Table 3 reveal that family enterprises have a greater orientation to CSR (6.25) than non-family enterprises (5.88), what represents a significant difference at 1% (0.005<0.01). As regards the CSR report variable, we can note that the existence of CSR report in the companies make them more socially responsible (6.35) than those without this report (5.90), with significance at 1% (0.002<0.01). However, neither the sector nor the size has an influence on the enterprise CSR.

ANOVA dependent variable: CSR.

| Source of variation | Degrees of freedom | F | Significance level |

|---|---|---|---|

| Sector | 2 | 2.322 | n.s. |

| Size | 2 | 0.641 | n.s. |

| Family character | 1 | 8.410 | 0.005*** |

| CSR report | 1 | 10.586 | 0.002*** |

| EF*CSR report | 1 | 3.848 | 0.053* |

| Average values of the variable | No. | FE | No. | nFE | Total no. of cases | Total (average values) |

|---|---|---|---|---|---|---|

| With CSR report | 45 | 6.36 | 11 | 6.31 | 56 | 6.35 |

| Without CSR report | 29 | 6.08 | 38 | 5.76 | 67 | 5.90 |

| Total | 74 | 6.25 | 49 | 5.88 | 123 | 6.10 |

Moreover, the interaction between the family character factor and CSR report, with significance at 10% (0.053<0.10), reflects that family enterprises with CSR report (6.36) are found to have a stronger orientation towards CSR than those family enterprises without this report (6.08). Likewise, they tend to CSR more than non-family enterprises which have CSR report (6.31) or not (5.76). These differences can be more clearly seen in Fig. 4, where it can be noted that just because of being family enterprises they have an orientation towards CSR, especially when having CSR report. However, in the case of non-family enterprises the existence of CSR report is a determining factor to be concerned about aspects related to CSR.

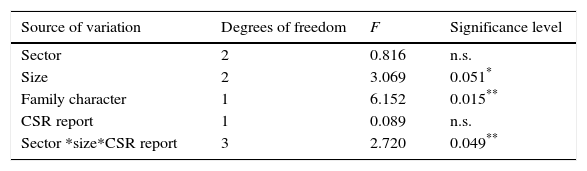

On the other hand, the analysis has been made taking into consideration the dependent employee training variable, and keeping the independent variables for the previous case (sector, size, family character and CSR report), as shown in Table 4. In this case, the size of the enterprise has an influence on the willingness for better staff training, micro-enterprises standing out (6.59) and very closely medium-sized enterprises (6.52), with significance at 10% (0.051<0.10).

ANOVA dependent variable: staff training.

| Source of variation | Degrees of freedom | F | Significance level |

|---|---|---|---|

| Sector | 2 | 0.816 | n.s. |

| Size | 2 | 3.069 | 0.051* |

| Family character | 1 | 6.152 | 0.015** |

| CSR report | 1 | 0.089 | n.s. |

| Sector *size*CSR report | 3 | 2.720 | 0.049** |

| Variable average values | No. | FE | No. | nFE | Total no. of cases | Total (average values) |

|---|---|---|---|---|---|---|

| MicroSME | 14 | 6.74 | 6 | 6.23 | 20 | 6.59 |

| Small sized enterprise | 28 | 6.53 | 23 | 6.01 | 51 | 6.29 |

| Medium sized Enterprise | 32 | 6.78 | 20 | 6.09 | 52 | 6.52 |

| Total | 74 | 6.68 | 49 | 6.07 | 123 | 6.44 |

With regard to family character, family enterprises (6.68) develop more policies related to staff training in contrast with non-family ones (6.07), with significance at 5% (0.015<0.05). Additionally, if we go into detail about average values shown in Table 4, it's worth mentioning that family enterprises are more concerned about staff training, be it micro (6.74), small-sized (6.53) or medium-sized enterprises (6.78), since all have very similar results. However, in the case of non-family enterprises, micro-enterprises (6.23) have the greater tendency to staff training. It could be due to the fact that in micro-enterprises a reduced number of employees must do many different tasks. Therefore, because of the necessity of versatile workers with knowledge in different areas of the enterprise, these enterprises value employee training much more.

In addition, it is significant at 5% (0.049<0.05), the interaction between sector, enterprise size and the existence of CSR report. In this case, let me just point out that enterprises in the tertiary sector, medium-sized and with CSR report (7.51) are more concerned about employees training.

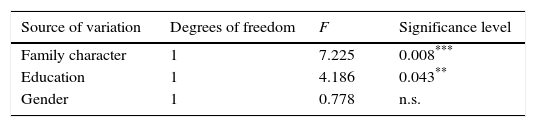

On the other hand, another ANOVA has been carried out taking into consideration the dependent CSR variable (Table 5), with independent variables the family character (family vs. non-family enterprise), education level (university vs. non-university) and gender (man vs. woman). The results evidence, with significance level at 1% (0.008<0.01) and at 5% (0.043<0.05), that family enterprises are more socially responsible (6.25) than non-family ones (5.88). Besides, this is also influenced by the level of education, as managers with a university education (6.24) have greater orientation towards CSR than their colleagues without a university education (5.96). In contrast, the fact of being a man or a woman has no influence on the CSR. Nevertheless, no significant differences have been found while analyzing with the dependent employee training variable.

ANOVA dependent variable: CSR.

| Source of variation | Degrees of freedom | F | Significance level |

|---|---|---|---|

| Family character | 1 | 7.225 | 0.008*** |

| Education | 1 | 4.186 | 0.043** |

| Gender | 1 | 0.778 | n.s. |

| Variable average values | No. | FE | No. | nFE | Total no. of cases | Total (average values) |

|---|---|---|---|---|---|---|

| With university education | 55 | 6.26 | 9 | 6.11 | 64 | 6.24 |

| Without university education | 19 | 6.22 | 40 | 5.83 | 59 | 5.96 |

| Total | 74 | 6.25 | 49 | 5.88 | 123 | 6.10 |

Therefore, it should be pointed out that what really conditions orientation towards CSR and better staff training is the fact of being a family enterprise, as up to the moment analysis carried out reveals, what makes us accept hypothesis H1: family SMEs are more concerned about their employees and their training than non-family ones and H2: family SMEs are more socially responsible than non-family ones. However, it has not been proven that gender influences either CSR or a higher level of staff training, discarding H3.1 and H3.3, since the interaction between gender and education level has not turned out to be significant. Nevertheless, we do accept H3.2: family enterprise managers or owners with a university education carry out more socially responsible management than those without a university education, as it's evident that a university education has a positive influence on the position towards the CSR.

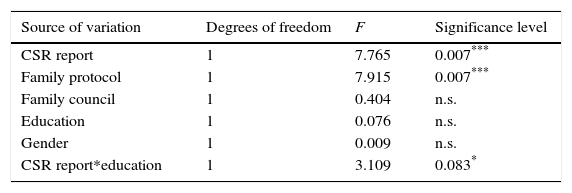

All things considered, an additional variance analysis has been carried out considering just family enterprises to check which factors have an influence on the social responsibility of those companies. As is shown in Table 6 CSR has been considered as a dependent variable while the independent variables are the CSR report, family protocol family council, as well as the gender and level of education; whereas there is no significant difference as regard staff training.

Dependent variable ANOVA: RSC (only family SMEs).

| Source of variation | Degrees of freedom | F | Significance level |

|---|---|---|---|

| CSR report | 1 | 7.765 | 0.007*** |

| Family protocol | 1 | 7.915 | 0.007*** |

| Family council | 1 | 0.404 | n.s. |

| Education | 1 | 0.076 | n.s. |

| Gender | 1 | 0.009 | n.s. |

| CSR report*education | 1 | 3.109 | 0.083* |

The results, significant at 1% (0.007<0.01), reveal that the existence of CSR report and family protocol make family SMEs orient towards CSR. It should be pointed out that in the case of family council it might not be significant since few companies in the sample count on one. Thus family SMEs with family protocol and CSR report (6.46) have greater orientation towards CSR. It has been plotted on a graph, making clear that the fact of having CSR report make family SMEs with or without protocol more socially responsible, but increasing like parallel lines, revealing that there is no difference between having protocol or not, which explains no such significant interference in both factors (Fig. 5).

.")

It is of interest that the education level analyzed together with other different factors isn’t significant in itself, in contrast to its interaction with the CSR report that shows significant differences at 10% (0.083<0.10). So we can notice in Fig. 6 how family SMEs with CSR report and whose managers have a university education (6.431) take aspects related to the CSR more into account than colleagues without a university education (6.105). In the same way, they are more socially responsible than managers either with a university education (6.105) or without (6.222) who work for family SMEs without CSR report.

.")

It should be pointed out that when managers have no university education, these have almost the same behaviour either with or without CSR report. Obviously, showing a greater orientation towards CSR with the aforesaid report. However, the case of managers with a university education is where there are real differences between having or not CSR report. So, managers with a university education who run family enterprises with CSR report take more advantage of its existence with a greater orientation towards CSR.

Conclusions and recommendationsIn the last years CSR has become object of attention by academics and professionals, gaining great relevance not only in education but also in the corporate world. It is worth noting that CSR is a way of managing a company, so it must be integrated into its strategy, it is the right way to proceed, taking into consideration the responsibilities and duties of the company with its stakeholders. Likewise, CSR must be strengthened and be included in the company raison d’être, be assumed and put into practice, obtaining in this way more responsible managers and companies and, as a consequence, a more balanced and fair socio-economic system.

After the limited number of studies about CSR in family SMEs and their importance, the aim of this study has been to reveal whether family SMEs are more socially responsible than non-family ones. As well as finding out whether gender and level of studies are influential factors in this behaviour, among others. The results obtained, on a sample of 123 family and non-family SMEs, indicate that family SMEs are more orientated towards CSR than non-family ones, as well as getting paid for previous work related to family enterprises (Cabeza et al., 2014; Cabrera et al., 2002, 2011; Garcés et al., 2014; Herrera et al., 2013, 2014). This fact is reinforced by the existence of CSR report in the SME, so companies which elaborate a CSR report seem to be a sign of their greater social responsibility, being more concerned about aspects related to social and environmental issues, and as a consequence, this is supported by the publication of that report as indicated Herrera et al. (2013).

On the other hand, it is proven that family SMEs are more concerned about their staff and their training as opposed to non-family ones, agreeing with several authors (Carrasco & Sánchez, 2014; Martín, 2015). More specifically, in the case of family SMEs, they are concerned about their staff training either in micro, small sized or medium sized enterprises, whereas in the case of non-family SMEs micro enterprises are the ones which back staff training, since a reduced number of workers must do many different tasks, valuing further training more. Nevertheless, if we do not make a difference between family and non-family SMEs it should be highlighted that medium-sized companies in the tertiary sector and with CSR report are more concerned about staff training.

As regards the personal characteristics of managers, those with a university education have a greater orientation towards CSR, specifically in the case of family SMEs, as claimed by Herrera et al. (2014). While the fact of being a man or woman does not make any significant difference as regards more socially responsible behaviour, as opposed to the existing evidence in the literature. To sum up, it is proved that a greater CSR of family SMEs is triggered by the existence of CSR report and family protocol. Furthermore, managers with a university education who run family enterprises that count on CSR report know how to take better advantage of its existence with a greater orientation towards CSR.

In conclusion, the results obtained in this study allow us to recommend SMEs counting on trained managers and executives with a university education, as well as elaborate CSR report in order to divulge their social responsibility practices. At the same time, in the specific case of family SMEs the existence of a greater CSR and family council is advisable. Due to the fact that these signs will contribute to a greater CSR, which will have an indirect effect on several benefits, above all on the improvement of the image and reputation, as well as on the relationship with employees and customers.

However, it must be pointed out that this study is not free from limitations, since the sample is just composed of four autonomous communities, predominating SMEs from the Valencian community, so the data cannot be generalized for SMEs all around the nation. Moreover, the concept of CSR is multidimensional and includes many aspects that have not been gathered in the survey due to their range. In this line, it should also be pointed out that we have not been able to draw conclusions regarding the family council due to its absence in the enterprises on the sample. Therefore, it would be interesting for future studies to extend it to other Autonomous Communities, making it possible to contrast whether cultural factors have an influence on results. Moreover, more aspects related to CSR should be considered due to the wide range of activities this concept covers.

Conflicts of interestThe authors declare no conflicts of interest.