This article seeks to clarify the impact of human capital on the innovation capacity of companies. We employ the literature review and some personals interpretations. Results have relevant implications for managers of companies that are interested in promoting their innovation activity. By considering how human capital is related with the innovation process, this article attempts to provide a useful guide of human capital indicators within the intellectual capital framework. We consider that the basic contribution of our work is the development of a system of indicators for human capital management with the objective of allowing for a clear picture of links between strategic human resources and the innovation capacity of companies. Moreover, it can be easily adapted to a given type of organization and, therefore, serve to compare companies belonging to the same sector of activity.

El objetivo de este artículo es definir el impacto del capital humano en la capacidad innovadora de las empresas y para ello hemos recurrido a la revisión de la literatura y a nuestras interpretaciones personales. Los resultados demuestran implicaciones de peso para los directores de empresas que se muestran interesados en promocionar la actividad innovadora. Mediante esta consideración de la forma en la que el capital humano influye en el proceso de la innovación, este artículo pretende servir de guía útil sobre los indicadores del capital humano dentro del marco del capital intelectual. Consideramos que la aportación fundamental de nuestro trabajo consiste en el desarrollo de un sistema de indicadores para la gestión del capital humano con el objetivo de ilustrar claramente una serie de vínculos entre los recursos humanos estratégicos y la capacidad innovadora de las empresas. Además, puede adaptarse fácilmente a un tipo determinado de organización y, por tanto, servir para comparar empresas que pertenezcan al mismo sector de actividad.

1. Introduction

The nature of world economic growth is, in part, due to innovation speed. This is possible given the rapid technological evolution, shorter product life cycles and to the higher rate of development of new products (Plessis, 2007). Obviously, in a globalized world the international division of work is not a consequence of relative salary costs, but of quality differentials in products and/or productivities. Specifically, in the knowledge society these differentials depend on the use of science and technology applied to its creation, this is, on the quantity of incorporated intelligence (Urrutia, 2007). In this sense, innovation can be defined as the process that allows companies to accumulate knowledge and technological capacities to improve productivity, cost reduction and prices while, at the same time, contributes to the creation of new products and to the quality increase of existing ones.

At the present moment, we must keep in mind that the capacity a company has to innovate depends, in great extent, on intangible assets and knowledge it possesses and, of course, on the manner it is able to employ these (Alegre & Lapiedra, 2005; Subramaniam & Youndt, 2005). This perspective of innovation depends on certain factors, such as the possession of adequate professional competencies, attitudes, aptitudes and intellectual agility, good relations within the workforce, adequate organizational technology, the capacity to bring in and retain the best professionals, etc. These intangible assets are commonly called intellectual capital (IC) and most papers establish that it consists of three elements: human capital (HC), structural capital (SC) and relational capital (RC) (Edvinsson & Malone, 1997; Bontis, 1998).

In this paper we attempt to identify the elements of IC that can contribute to guaranteeing the innovation capacity of companies. With this aim, we pay special attention to HC (which includes experience, skills, employee professional development, teamwork, etc.) We present a guide of indicators to manage this item taking into account aspects related both to the development and renovation of HC and to its efficiency and stability. From a business perspective, we consider that results have important implications for managers of companies committed to innovation, especially in knowledge-intensive activities. The basic objective is that managers, taking into account the specific characteristics, objectives and strategies of their firms, and the sectors to which they belong, decide which indicators are the most appropriate to each case.

2. Relevance of human capital in determining company innovation capacity

Innovation is definitely one of the basic pillars of company competitiveness. We are all aware of the positive effects of technological innovation, given the possible productivity improvements, new product development, quality and differentiation increases, cost and price reductions, etc. Therefore, it can be considered that innovation is critical to increase company value (Tseng & Goo, 2005).

However, investments in research and development are necessary but not sufficient to develop innovation capacity (Martín et al., 2009). In this sense, it must be combined with investment in HC (this would allow for the transformation of innovation potential into productive realities), SC (this contributes to have the full command of processes related to assets owned) and RC (related to knowledge included in relations with stakeholders). Taking into account this definition, innovation can be considered as the most knowledge intensive organizational process, given that it depends both on individual employee know-how and internal and external company knowledge (Aramides & Karacapilidis, 2006).

Within the three components of intellectual capital, human capital, understood as both individual and group knowledge of company employees, is especially important in determining innovation capacity of firms. We therefore consider a broader definition of HC to include not only individual knowledge, but also the part of knowledge that arises from relations between company personnel (Broking, 1996; Edvinsson & Malone, 1997; Euroforum, 1998).

Littlewood (2004) noted the importance of HC when they established that, nowadays, HC is one of the factors that determine organizational competitiveness, given that competencies, knowledge, creativity, capacity to resolve problems, leadership and personal compromise are some of the assets required to meet the demands of turbulent environments and reach organizational goals. For Carson et al. (2004), HC includes tacit knowledge and communications skills, the entrepreneur spirit and other personal attributes such as disposition or aptitudes for life long learning. European Commission (2006) in its RICARDIS report establishes that HC is given by knowledge, skills, experiences and abilities of employees.

Within HC, two streams of thought exist. One is basically economic and the second one makes reference to management of these assets.

From an economic point of view, Gary S. Becker in the early nineteen sixties and, later, Denison (1964) and Mincer (1974) made some of the most relevant contributions to HC. The central hypothesis is that educational level increases productivity of individuals. As these individuals reach higher educational levels, they suffer certain transformations that evidence relevant differences in their productive capacity compared to others that have not reached the same level. This idea was considered innovative and even revolutionary at that moment because education became an investment in humans and this, in turn, meant the existence of a wider conceptual definition for capital. Therefore, the traditional dichotomy for productive factors is substituted with a new trilogy: non¿qualified work, HC and material capital (Freire et al., 2007).

The second stream of literature is focused on HC management. It is based on the fact that people are a tangible resource in organizations and that their value depends on the knowledge and skills they have. Existing work in this field reinforces the idea that in developing economies, the different mechanisms that can be employed to accumulate HC (formal education, on-going training and occupational training) play a key role in improving competitiveness and creating knowledge (Barro & Lee, 2001).

Traditionally, management models have basically included tangible assets and have failed to capture the value of the intangible ones. However, over the last decades, models have highlighted the importance of incorporating intangible assets, such as HC, relational capital or structural capital. Furthermore, it has been estimated that IC accounts for most of the market value of a given organization although this is not recorded in financial statements (Nonaka & Takeuchi, 1995; Brennan & Connell, 2000; Heng, 2001; Watson et al., 2005; Martínez¿Torres, 2006). Difficulties related to the valuing of this type of resources are not a general impediment to finding increasing organizational proposals to manage and power them. Effective administration in this sense has great potential for value creation and, therefore, intangible assets cannot be ignored (Brennan & Connell, 2000; Cañibano & Sánchez, 2003; Bozbura et al., 2007; Sánchez, 2008). Several papers have focused on the importance of HC to create sustainable competitive advantages and on the direct impact it has on innovation (Hayton, 2005; Leiponen, 2006; Díaz et al., 2006; Hedge & Shapira, 2007; Pizarro et al., 2007; Dakhli & De Clercq, 2004; Zerenler et al., 2008; Martín et al., 2009), although empirical evidence is quite limited up to date.

The key to managing IC is to monitor its transformation from the beginning (Lynn, 1998), when it is simple information, until it provides organizational value. Knowledge (individual or organizational) can be considered part of IC only when it is used and shared to create value (Salas & Cannon-Bowers, 2001; Martínez Ramos, 2003). We consider it is more important to analyze the strategic effects; this is, in the long run, instead of the trade-off effects present in the short term.

In this paper, as specified above, we will focus on one of the components of IC; this is, HC. One of the basic problems of HC management is the difficulty in measuring it, as it includes individual elements such as education, work experience, capacity, motivation, etc. Moreover, as with any other asset, obsolescence must be taken into account and it is rather surprising that very few empirical papers include it. De Grip and Van Loo (2002) distinguish, from an economic view, two types of depreciation:

• Technical depreciation: refers to decreases in the value of HC due to physical deterioration (skill atrophy, lack of new skills...) given situations such as inactivity or unemployment, low motivation for work, etc.

• Economic depreciation: related to the loss in market value of employee qualification, basically as a consequence of specific skill obsolescence, rapid technological change, changes in sector structure and lack of organizational skill adaptation.

In this paper, we focus on indicators to measure HC that are directly related to company innovation.

3. Components and dimensions of human capital: A descriptive analysis from intellectual capital theories

In this section we outline the basic elements of IC models with respect to their contribution to HC, taking into account connections with company innovation.

3.1. Integral Credit Scorecard Model (Kaplan & Norton, 1992)

This model notes that intangible assets must be aligned with business strategy (those that are not will not create much value although investments made may be high) and that, at the same time, they must be integrated (they must be created using capacities built through other intangible and tangible assets and not through independent capacities that do not allow for synergetic effects to arise).

For these authors, HC represents the availability of skills, talent and know-how of employees to undergo fundamental internal processes that guarantee strategic success. Innovation is not considered as a capital alone but it constitutes an internal process that increases the value of HC, informational capital and organizational capital. The influence of innovation on HC is centred on how key employees reach the specified objectives, given the human resources they have and the optimal personnel needs (Trillo & Rodríguez, 2007).

3.2. Skandia Navigator Model (Edvinsson, 1997)

The Skandia model constitutes a strategic and operational management system based on the fact that the performance of a company comes from its capacity to create sustainable value, given the strategic vision and mission of the firm. The concept Edvinsson and Malone include within IC is that all assets are valuable for the organization, including HC and structural capital.

From a human approach, they include all individual capacities, knowledge, skills and experience of employees and managers as well as the creativity and innovation capacity of the organization. This constitutes the core of the model, although it is perhaps the most difficult part to measure given that it includes assets that are not owned by the company.

Innovation in this model is linked to the contribution of human resources to the organization. Professional experience and innovation are considered to be the foundations of the future while they support the burden of organizational structure.

3.3. University of Western Ontario Model (Bontis, 1996)

Bontis considers that IC is the sum of HC, structural and relational capital.

With regard to HC, the author considers that innovation is the result of the communication and learning processes of individuals that take place in the organization. We can say that HC is a source of innovation, strategic renovation and value for the company and that it is made up of knowledge stock, both of tacit and explicit type, which members have. Bontis considers that HC explains the other two components of IC.

3.4. Intangible Assets Monitor (Sveiby, 1997)

In this model, intangible assets are valued with regard to business strategy. Sveiby considers that these resources include the internal and external structure of the company and the competencies of employees.

The problem with the measurement of intangible assets is related to the need to identify the specific flows that change or influence the market value of the company. The author establishes three types of indicators for each block of intangible assets: first, indicators of growth and renovation (considering the potential future of a company); second, efficiency indicators (inform about the productivity of intangibles) and, third, stability indicators (show the degree of permanence of these assets in the company). Innovation is considered to be a first¿class factor in accordance with the previous indicators.

The author considers that not all employees must be taken into account within HC, only those that are true experts. Therefore, the remaining workers are left aside. He also establishes the existence of a dimension called employee competencies,1 which are defined as the capacity of organizational members to act consequently in different situations and create both material and immaterial assets.

3.5. Nova Model (Camisón et al., 2000)

The basic objective of this model is to measure and manage IC in any type of organization regardless of its size. The structure of IC is determined by four components (human, organizational, social, and innovation capital and learning). Innovation is considered as an individual capital on its own.

Human capital includes assets related to individuals' knowledge (tacit and explicit) which is divided into: technical knowledge, experience, leadership skills, teamwork skills, employee stability and managing skills with regard to prospective activities and advancing challenges.

3.6. Intellect Model (Euroforum, 1998)

Intellectual capital is integrated in three basic blocks: HC, structural capital and relational capital. Each one must be measured and managed over time and towards the future.

Human capital is tacit and explicit knowledge that is useful for the organization and that people and teams belonging to a company possess, along with the capacity to generate it. They agree that although that which has this type of capital is the employee and not the organization, it is a part of company value and, therefore, must be considered organizational capital. For these authors HC is the basis for the generation of the other two types of IC.

Intangible assets belonging to HC are categorized in the present or future dimension.

• Within the present dimension, we would have personal satisfaction, employee typology, competencies of workers, leadership, teamwork, and stability or risk of losing stability;

• Within the future dimension, the model considers the improvement of employee competencies and the innovation capacity of people and teams.

The model establishes several indicators to measure each element of HC. This proposal can serve as a guide for each particular case of a given organization.

3.7. Organizational Learning Model of KPGM Consulting (Tejedor & Aguirre, 1998)

This model was developed as part of the "Logos Project: Research relating to the learning capacity of Spanish firms" by KPMG Peat Marwick Management Consulting. Three factors are considered relevant to explain organizational learning:

• The strong and conscious commitment of the organization to continuous learning at all levels of the company.

• The learning behaviours and mechanisms at all levels.

• The development of infrastructures that determine company operation and the behaviour of people and groups to favour learning and permanent change.

According to this model, an organization can only learn if its employees learn. However, even if this happens, the knowledge gained may not be a useful asset for the organization. To achieve organizational learning, specific mechanisms should be developed to create, capture, store, transmit and interpret knowledge. This will make the most of and adequately use individual and team learning.

3.8. Stewart Model (Stewart, 1998)

Intellectual capital is seen as an intangible material that can be a source of wealth. It is the sum of HC, relational capital and customer capital.

The author establishes a series of principles that should guide IC administration. Those related to HC are the following:

• Firms do not own HC and customer capital. They share ownership of the former with employees and of the latter with suppliers and customers. To effectively manage these resources, the company must be aware of this sharing situation and think that inadequate managing will destroy value.

• To create usable HC, the organization must promote teamwork and other forms of social learning. Interdisciplinary teams learn, formalize and capitalize talent because they spread it and make it less dependent on the individual. This reduces the risk of losing talent if the individual leaves the firm.

• To administer and develop HC, we must consider that wealth is created through skills and talent. These are strategic resources for the firm due to their capacity to create value that, in the last stage, customers are willing to pay for. Talented people who do not create company value should be treated as costs to be minimized, while those that do generate value must be seen as investment assets.

• Human capital and structural capital mutually reinforce themselves when the organization has its mission straight and the enterprising spirit surfaces. Symmetrically, these capitals also destroy each other when many of the organizational activities do not have value for customers or if the firm is concerned, to a greater extent, with conducts instead of with strategies.

With respect to indicators, Stewart presents an open model that serves as a guide and allows each organization to elaborate a proposal closer to its own needs.

3.9. Intellectus Model (Bueno et al., 2004)

Intellectus is presented as an evolutionary model, based on social capital. The latter is the sum of present and potential resources that arise from individual or social relations.

Intellectual capital is subdivided into HC, structural (organizational and technological) and relational capital (business and social).

Each of these five components involves basic elements that define their characteristics. At the same time, each element is analyzed through a series of variables that are the central object to measure and that must be managed with great efficiency, effectiveness and to the satisfaction of the parties involved. Each variable is associated with different indicators that help determine and create value.

Human capital makes reference to knowledge (explicit or tacit and individual or social) that people or groups possess and to the capacity of creating knowledge and, therefore, it is useful for the organizational mission. This capital is integrated by what people and groups know and by their capacity to learn and share this knowledge in benefit of the organization.

Innovation is generated through technological capital (within others factors) and it acts as a link between internal values that arise from HC and organizational capital and external values related to business and social capital.

From these models, the following conclusions are reached:

• They have many similarities. The concepts of HC are virtually identical and the real differences come from the emphasis given to some elements. In whatever manner IC is categorized, HC is always present and this is due to its importance to business structure and function;

• With regard to innovation, signs of controversy become more visible. In this manner, some models consider this item a part of the internal processes of the organization that increases firm value, while others see HC itself as a source of innovation.

4. A system of indicators for HC management within an innovation context

The knowledge of an employee is based upon his or her skills, experience and ability to absorb new knowledge. Therefore, while knowledge is a resource in its own right, the way in which knowledge is managed and used will affect the quality of services that can be leveraged from each resource owned by the firm (Darroch, 2005) and also means an increase in productivity.

Although the potential value of HC is usually recognized by company managers, it is necessary to identify which of these investments actually have an effect on innovation capacity and how these connections take place.

This information, in the case of HC, is difficult to obtain because we are working with individual virtues such as attitudes, motivation, learning capacities, etc. Moreover, these elements are not owned by the organization, so they can be lost if qualified employees leave the company. The organization must convert this knowledge into organizational knowledge. This leads us to include the value of all those elements that can favour value creating employee commitment apart from factors that help transform HC in structural capital, that is, assets belonging to the organization and not to individuals.

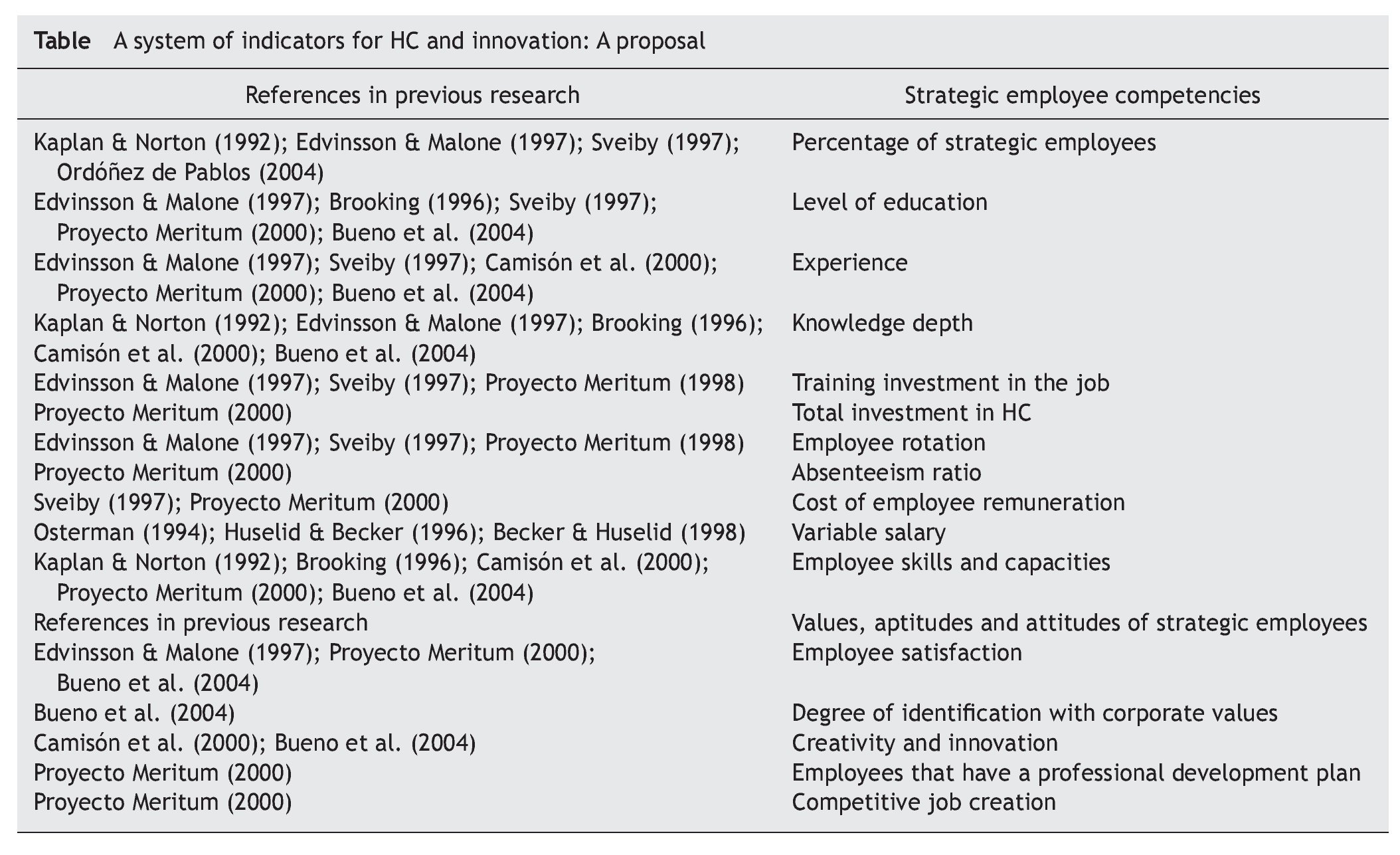

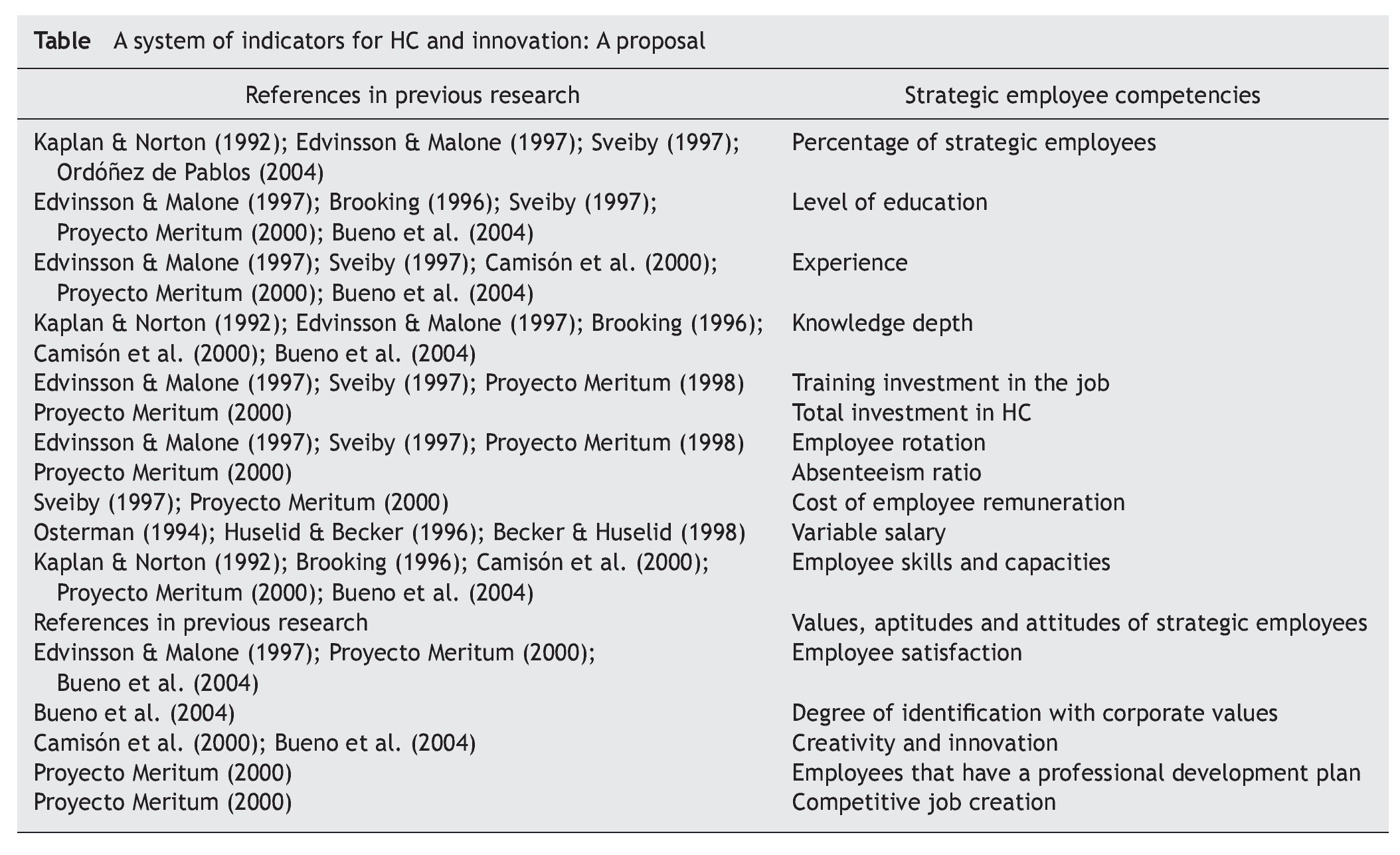

Nevertheless, the fundamental aim of a system of indicators for HC is not only to value or measure knowledge directly, but to improve the capacity to create and exploit it. We will keep this in mind in our proposal and will pursue clear connections between intangible resources and activities and consequent wealth (see Table). With regard to the frequency in the elaboration of indicators, it will depend on factors like the type of organization, the dynamics of the industry, or on strategy, although we recommend a minimum of once a year.

Our proposal classifies HC indicators into two large groups: those that belong to competencies of strategic employees and those that make reference to values and attitudes.

To discover key employee's competencies, it is necessary to take into account the following indicators:

1. Percentage of key employees: this measure informs of the level of HC concentration. Because HC only includes knowledge that has the potential to create organizational value, not all employees are taken into account.2

2. Educational level: most models measure this through the number of professionals with higher education. A higher value of educational level has a positive effect on the probability of new product and service development. However, high educational levels are relevant only in relation with specific aims and sectors of each organization. Therefore, not all companies need professionals with higher education and each one should establish objectives taking strategy into account and measure educational level of HC in relation to those objectives.

3. Experience: this is a very important measure of HC, especially for organizations with high percentages of workplaces that require a wide range or specific knowledge regarding functions and technology used. It seems logical to think that more experienced employees will supply more new strategies or ideas for new products, among others, based on the experience acquired over time, compared to new workers.

Experience must not be understood as learned knowledge in the present organization only, but also as experience acquired in other companies, workplaces, cultures, nationalities, etc. The emphasis is placed on the advantage of having a workforce with diverse experience because this should result in more flexible and productive organizations.

4. Knowledge depth: one of the measures used to value this is HC value added, which reflects what part of the value added is due to each monetary unit invested in employees. It is calculated as the sum of all income minus all expenses not due to employees divided by the sum of wages and social fringe benefits.

5. Investment in workplace training: Workplace training should have a positive effect on the probability of innovation in products/services. Improvement of working skills of employees is essential to maintain high quality of workforce, being able to adapt to changes in demand and to secure the introduction of innovations continuously. One way of influencing employee learning is to invest in formal training programmes and processes. Within the different ways of measurement, we propose the investment in initial training (number of average hours of training needed to have productive workers) and the investment in workplace training (average number of hours of training per year).

6. Total investment in HC: this reflects the degree of organizational commitment to HC. It is the sum of expenses of the human resource department and the cost of employee selection, hiring, professional development, motivation strategies, etc., plus salaries (including travel expenses and social services). The comparison of this indicator with that of other companies of the same sector can give us an idea of our relative HC allocation.

7. Employee rotation: as we explained in the second section, one of the most threatening elements for HC deterioration is the voluntary abandonment of employees with high knowledge levels. Therefore, the index of personnel rotation must be included. We define it as the proportion of employees that leave the company each month.

8. Absenteeism ratio: the measure of absenteeism usually identifies workers with personal problems, such as dissatisfaction or lack of motivation. This has adverse effects for companies, especially if it affects key workers. This highlights the importance of its evaluation and tracking. We propose the percentage of unexpected absenteeism of employees as a measure for this.

9. Remuneration cost per employee: It is necessary to recruit the best professionals. Moreover, it is also necessary to listen to them and avoid losing them. This can be achieved through motivation/remuneration programmes. Therefore, it is important to analyze relative category of professional salary that each organization offers in relation to the market sector. It is also possible to calculate this variable for each department or section.

10. Variableremuneration: With respect to employee remuneration, innovative organizations are more likely to include a variable component of salaries depending on firm results. This should strengthen the tie between workforce and organizational objectives and innovations achieved. (Osterman, 1994; Huselid & Becker, 1996; Becker & Huselid, 1998). Our calculation proposal is the proportion of employees that have a variable component of salary, based on objectives.

11. Skills and capacities of employees: this refers to the knowledge related to the manner in which duties are performed, know-how, that is, employee skills acquired through work experience. To measure it, the immediate superior or the human resources department must elaborate a questionnaire, based on a scale of 5 points, where employee skills and capacities are evaluated. The following items should be taken into account:

• Employee skills related to cooperation, teamwork, interpersonal communication, problem-solving, information management, and decision-making;

• Employee capacities to apply knowledge to practice, analyze and synthesize, organize and draw up plans, criticize and auto-criticize, work in interpersonal teams, learn, lead a team, and adapt to dynamic changes in the organization.

To discover the values and attitudes of key employees, the following indicators must be taken into account:

1. Employee satisfaction: it is related to the employee's attitude at work and, of course, it is a rather subjective measure because it includes, along with other factors, the existence of equilibrium between contributions and compensations, workplace recognition, the degree of connection and participation in strategic activities, the equilibrium between work and private life, work insecurity (due to the type of contractual arrangements), etc. Those workers with higher levels of satisfaction will, more probably, present higher performance measures and, therefore, are more productive. The relevance of this measure has grown over the past years because several researchers have demonstrated the link between this variable and the retention of workers within the organization and adequacy of customer services. To value employee satisfaction, we propose a personal survey with scales of 5 points.

2. Identification with corporate values: The existence of an adequate internal environment favouring innovation, creativity, intuition and acceptance will allow for the creation of a unique objective shared by all organizational members. We consider that a personal survey, with a scale of 5 points, should be used to identify the degree of employee identification with organizational objectives. We consider that a personal survey, with a scale of 5 or 7 points, should be used to value personnel satisfaction.

3. Creativity: creativity is considered a precursor of innovation. For most organizations it entails a very important measure that determines product and service differentiation in the mid- and long-term. We suggest the following indexes:

• Employee creativity through the analysis of suggestions and new ideas they present.

• Innovation through the percentage of those new ideas that have succeeded.

4. Number of employees that have a professional development plan: the aim of professional development plans is to allow employees to have the possibility of being promoted within the organization. This directly influences motivation and commitment.

5. Creation of competitive workstations: as with personal development plans, the increase of strategic workplaces in the organization is important to retain HC and attract new competent employees. We establish the following measures:

• Number of competitive workplaces created during the last year.

• Percentage of employees promoted.

These indicators highlight the importance of HC in a given organization along with its capacity for innovation.

5. Conclusions

Human capital management is a key organizational element for obtaining sustainable competitive advantages and its effective administration sets up an enormous potential for value creation in the organization and, therefore, has a direct effect on innovation (Bozbura et al., 2007). The difficulties in the measurement of intangible resources are not an impediment for organizations to take them into account, manage and power their value increasingly. In this manner, employee competencies and their values and attitudes at work are prime elements to accomplish organizational missions in dynamic environments. Organizational capacities are, to a great extent, determined by the possession of these intangibles; and to improve these, it is necessary to identify and manage the latter (Marr et al., 2004). Those related to knowledge resources can be considered a combination of processes, comprehension of the context and experience that is submitted to continuous accumulation. However, only those that add value and are rare, inimitable and do not have equivalent substitutes are able to generate sustainable competitive advantages (Barney, 1986, 2002).

In this paper, we have examined the most relevant contributions made by IC models with respect to HC and its relation to organizational innovation capacity. We have also gathered the most extended indicators used to measure it. Although the first research papers on IC date back to the middle of the previous century, the literature review reveals that there is still some confusion regarding the term HC and its relation to innovation. In this sense, some models consider the latter a consequence of investment decisions in HC, while others understand innovation as another capital, individually considered, although most models accept the importance of HC as a powering factor of innovation in organizations.

From a strategic point of view, HC reveals employee knowledge as a key factor to develop innovation and commercialize it and, in this manner, it may determine the organization's competitive position, especially in technology-intensive activities. Therefore, managers must have reliable, relevant and timely information regarding HC to make efficient management decisions and promote innovation.

In this context, we have developed a system of indicators for HC management with the objective of allowing for a clear picture of links between strategic human resources and wealth generation. The basic contribution of our study is its usefulness for managers; as it may help them face up to existing challenges. We are, of course, aware of the ambitiousness of this idea although we also detect the need for organizations to have a common and easy-to-understand guide for HC and its implications on innovation.

We have taken into account several aspects related to HC. First, growth and renovation through indicators such as level of education, experience of key employees, the creation of competitive workplaces or the investment in HC. Second, we have also included factors regarding efficiency using indicators such as value added or the variable component of salary. Third, we considered the importance of stability of HC and, therefore, included, for example, key employee rotation, level of satisfaction or identification with corporate values. The originality of this system of indicators is that it is presented in a clear and brief manner and that it opens the possibility for decision makers to adapt it to a given organization and make comparisons between different companies.

Of course, a future line of research should include an empirical study to check the importance of these indicators. In this sense, we are now working on the design of a survey and collecting data.

To conclude, it is important for managers to take into account that not only HC has an effect on innovation, but also SC and RC. The innovation process of an organization depends, in great extent, on the incorporation of HC to productive realities and this, in turn, is supported by organizational structure and organizational external relations. Therefore, mastery of processes, organizational routines, customer accounts or ownership rights are a source of innovation success.

1. For the specific case of individual competencies, indicators proposed are: a) growth and renovation indicators (experience, educational level, training costs, personnel rotation, customers that promote competitiveness); b) efficiency indicators (proportion of professionals, value added by professionals) and c) stability indicators (average age, length of service, remuneration position, rotation of professionals).

2. From here on, all indicators are based on key employees, that is, on personnel whose knowledge creates value or HC.

Received July 29, 2011; accepted May 22, 2012

*Corresponding author.

E-mail address:mercedes.teijeiro@udc.es (M.M. Teijeiro-Alvarez).

References

Alegre, J., Lapiedra, R., 2005. Gestión del conocimiento y desempeño innovador: un estudio del papel mediador del repertorio de competencias distintivas. Cuadernos de Economía y Dirección de la Empresa 23, 117-138.

Aramides, E.D., Karacapilidis, N., 2006. Information technology support for the knowledge and social process of innovation management. Strategic Management Journal 27, 621-639.

Barney, J.B., 1986. Strategic factor markets: expectations, luck and business strategy. Management Science 32, 1231-1241.

Barney, J.B., 2002. Gaining and Sustaining Competitive Advantage, vol. 2. Prentice Hall, New York.

Barro, R.J., Lee, J.W., 2001. International data on educational attainment updates and implications. Oxford Economics Papers 53, 541-563

Becker, B.E., Huselid, M.A., 1998. High performance work systems and firm performance: A synthesis of research and managerial implications. Research in Personnel and Human Resources Management 16, 53-101.

Bontis, N., 1996. There is a price on your head: managing intellectual capital strategically. Business Quarterly 60 (4), 40-47.

Bontis, N., 1998. Intellectual capital: An exploratory study that develops measures and models. Management Decision 36, 63-76.

Bozbura, F.T., Beskese, A., Kahraman, C., 2007. Prioritization of human capital measurement indicators using fuzzy AHP. Expert Systems with Applications 32, 1100-1112.

Brennan, N., Connell, B., 2000. Intellectual capital: current issues and policy implications'. Journal of Intellectual Capital 1 (3), 206-240.

Brooking, A., 1996. Intellectual capital. Core asset for the third millennium Enterprise. 1.ª ed. International Thomson Business Press, London.

Bueno, E., Ordóñez de Pablos, P., Salmador, M.P., 2004. Towards an integrative model of business, knowledge and organizational learning processes. International Journal of Technology Management 27 (6/7), 562-574.

Camisón, C., Palacios, D., Devece, C., 2000. Un nuevo modelo para la medición del Capital Intelectual en la empresa: El modelo Nova. X Congreso Nacional ACEDE. Oviedo, September.

Cañibano, L., Sánchez, P., 2003. Measurement, management y reporting on intangibles: State of the art. In: Cañibano, L., Sánchez, M.P., Readings on intangibles & intellectual capital. AECA, Madrid, pp. 81-113.

Carson, E., Ranzijn, R., Winefield, A., Marsden, H., 2004. Intellectual capital. Mapping employee and work group attributes. Journal of Intellectual Capital 5, 443-463.

Dakhli, M., De Clercq, D., 2004. Human capital, social capital and innovation: a multi-country study. Entrepreneurship & Regional Development 16, 107-128.

Darroch, J., 2005. Knowledge management, innovation and firm performance. Journal of Knowledge Management 9 (3), 101-115.

De Grip, A., Van Loo, J., 2002. The economics of skills obsolescence: a review. In: De Grip, A., Van Loo, J., Mayhew, K. (Eds.), Research in Labor economics, understanding skills obsolescence. JAI Press, Amsterdam/Boston. vol. 1, pp.1-26.

Denison, E., 1964. Measuring the contribution of education (and the residual) to economic growth. In: The Residual Factor and Economic Growth. OCDE, Paris.

Díaz, N.L., Aguiar, I., De Saá, P., 2006. El conocimiento organizativo tecnológico y la capacidad de innovación. Evidencia para la empresa industrial española. Cuadernos de Economía y Dirección de la Empresa 27, 33-60.

Edvinsson, L., 1997. Developing intellectual capital al Skandia. Longe Range Planning 30, 336-373.

Edvinsson, L., Malone, M.S., 1997. Intellectual capital. Realizing your company's true value by finding its hidden brainpower. Harper Collins Publishers, Inc., New York, 1st ed.

Euroforum, 1998. Proyecto Intelect. Medición del capital intelectual. Instituto Universitario Euroforum, Escorial, Madrid.

European Commission, 2006. Reporting intellectual capital to augment research, development and innovation in SMEs. European Communities, Luxembourg.

Freire, M.J., Teijeiro, M., Blázquez, F., 2007. Evolución de la economía de la educación y su relación con el empleo. Tórculo, Coruña.

Hayton, J.C., 2005. Competing in the new economy: The effect of intellectual capital on corporate entrepreneurship in high-technology new ventures. R & D Management 35, 137-155.

Hegde, D., Shapira, P., 2007. Knowledge, technology trajectories, and innovation in a developing country context: Evidence from a survey of malaysian firms. International Journal of Technology Management 40, 349-370.

Huselid, M.A., Becker, B. E., 1996. Methodological issues in cross¿sectional and panel estimates of the human resources¿firm perfomance link. Industrial Relations 35 (3), 400-422.

Kaplan, R., Norton, D., 1992. Balanced scorecard¿measures that drive performance. Harvard Business Review January¿February, 71¿79.

Leiponen, A., 2006. Managing knowledge for innovation: The case of business-to-business services. Journal of Product Innovation Management 23, 238-258.

Littlewood, H., 2004. Análisis factorial conformatorio y modelamiento de ecuación estructural de variables afectivas y cognitivas asociadas a la rotación de personal. Revista Interamericana de Psicología Ocupacional 23 (1), 27-37.

Lynn, B., 1998. Intellectual capital. Key to value added success in the next millennium. CMA Magazine 72 (1), 10-15.

Marr, B., Schiuma, G., Neely, A., 2004. Intellectual capital defining key performance indicators for organizational knowledge assets. Business Process Management Journal 10 (5), 551-569.

Martín, G., Alama, M., Navas, J.E., López Sáez, P., 2009. El papel del capital intelectual en la innovación tecnológica. Una aplicación a las empresas de servicios profesionales de España. Cuadernos de Economía y Dirección de la Empresa (40), 83-110.

Martínez Ramos, M., 2003. De la contabilidad de los recursos humanos al capital intelectual. Una ampliación necesaria. Dirección y organización: Revista de dirección, organización y administración de empresas 29, 134-144.

Martínez-Torres, M.R., 2006. A procedure to design a structural and measurement model of intellectual capital: an exploratory study. Information and Management 43 (5), 617-626.

Mincer, J., 1974. Schooling, experience, and earnings. Columbia University Press, New York.

Nonaka, I., Takeuchi, H., 1995. The knowledge creating company: How Japanese companies create the dynamics of innovation. Oxford University Press, Oxford, UK.

Ordóñez de Pablos, P., 2004. El capital estructural organizativo como fuente de competitividad empresarial: un estudio de indicadores. Economía Industrial 357, 131-140.

Osterman, P., 1994. How common is workplace transformation and who adopts it? Industrial and Labor Relations Review 47 (2), 173-188.

Pizarro, I., Real, J.C., De La Rosa, M.D., 2007. El papel del capital humano y la cultura emprendedora en la innovación. XVII Congreso Nacional De ACEDE. Oral presentation, Seville.

Plessis, M., 2007. The role of knowledge management in innovation. Journal of Knowledge Management 11 (4), 20-29.

Proyecto Meritum, 2000. Guidelines for the Measurement and Disclosure of Intangibles. Paper presented Meritum meeting. Sevilla, 27-29 Enero.

Salas, E., Cannon-Bowers, J.A., 2001. The science of training: A decade of progress. Annual Review of Psychology 52, 471-499.

Sánchez, M.P., 2008. Papel de los intangibles y el capital intelectual en la creación y difusión del conocimiento en las organizaciones. Situación actual y retos de futuro. Arbor, Ciencia, Pensamiento y Cultura 732, 575-594.

Stewart, T.A., 1998. La nueva riqueza de las naciones: el capital intelectual. Granica, Buenos Aires.

Subramaniam, M., Youndt, M.A., 2005. The influence of intellectual capital on the types of innovative capabilities. Academy of Management Journal 48, 450-463.

Sveiby, K.E., 1997. The intangible assets monitor. Journal of Human Resource Costing and Accounting 2 (1), 73-97.

Tejedor, B., Aguirre, A., 1998. Proyecto Logos: investigación relativa a la capacidad de aprender de las empresas españolas. Boletín de Estudios Económicos LIII (164), 231-249.

Trillo, A., Rodríguez, O., 2007. La influencia de la innovación en el capital intelectual de una empresa. Propuesta de un modelo. Conocimiento, innovación y emprendedores; camino al futuro. pp. 1419-1431.

Tseng, C., Goo, Y.J., 2005. Intellectual capital and corporate value in an emerging economy: empirical study of Taiwanese manufacturers. R&D Management 35, 187-201.

Urrutia, J., 2007. La innovación y las grandes empresas. Cuadernos de Economía 30 (84), 5-22.

Watson, A., Stanworth, J., Healeas, S., Purdy, D., Stanworth, C., 2005. Retail franchising: An intellectual capital Perspective. Journal of Retailing and Consumer Services 12, 25-34.

Zerenler, M., Burak, S., Sezgin, M., 2008. Intellectual capital an innovation performance: empricial evidence in the Turkish automotive supplier. Journal of technology management & innovation 3 (4), 31-40.