This paper examines the extent to which the information on Social Responsibility (SR) that managers of firms in the Autonomous Community of Extremadura in Spain have determined their positive predisposition towards the practical exercise of environmentally responsible actions. With the theoretical background of Market Orientation (MO), a conceptual model of causal relationships is defined and is contrasted empirically with a structural equations model for a sample of 758 SME's in Extremadura. The results verify that the greater the concern for seeking and receiving information about SR, the greater the tendency towards environmentally responsible management, and the greater the importance given to the disclosure of the SR the firm itself practises. Consequently, the provision of information, awareness, and training related to SR promoted by managers or fostered by business organizations and public administrations will have a positive effect on the orientation towards environmental protection.

Current concerns about expanding financial accounting information to include social and environmental issues are related to the evolution of ethics in business. This management approach defends that the values of honesty, justice, and human rights must be reconciled with economic goals under the prism of “ethical economic rationality” (Agliata et al., 2010: 209). This new trend takes a clear risk in that firms will focus on the development of external documents to communicate their achievements (Dye, 1985, 1986). While this may be helpful in reducing information asymmetries between firms and their stakeholders (Baginski et al., 2000), it can also be applied as part of an opportunistic strategy that may even manipulate information in order to create a good image (Hooghiemstra, 2000; Yuthas et al., 2002; Baginski et al., 2004). An important group in which to examine whether more responsible firms are those which conduct more disclosure activities is that of SME's. This is because responsible behaviour in SME's is generally motivated by the will of their managers rather than their firm's image, and their tendency is to focus on internal stakeholders (Perrini, 2006) because they have difficulties in communicating externally their responsible actions (Murillo and Lozano, 2006), especially in regard to environmental aspects (Del Baldo, 2010).

The objective of this research was to obtain an explanatory model that allows one to analyze the relationship between the different components of the environmental responsibility of SME's, determining whether their actions in this sense are more or less related to their disclosure of that responsibility. The main contribution of the paper is to demonstrate empirically with a large sample of SME's that voluntary orientation to the environment with the implementation of proactive actions is translated into broader disclosure of those actions, thus coherent with and verifying the Theory of Incremental Information. The general objective of the paper may be broken down into the following specific objectives:

- •

To analyze the components of the orientation to environmental responsibility of SME's with the development of a conceptual model based on the concept of Market Orientation described by Kholi and Jaworski (1989, 1990) and Narver and Slater (1990). With this objective, a theoretical framework is defined for the analysis of environmental orientation.

- •

To approach the measurement of components through indicators adapted to the case of SME's. This objective will allow employers to diagnose their orientation to the environment, and academics to have validated measurement scales available in the field of SME's.

- •

To evaluate potential causal relationships between the variables of the model in order to determine the effect of environmental measures on the level of disclosure. With this objective, it is demonstrated that the efforts of information, awareness, and training in SR in the management of these firms, of public administrations, or of business organizations have a positive effect on the orientation towards respect for the environment.

The contribution of this work to the field of environmental management is to address a research area in SR that has lacked consistent empirical evidence in the particular area of SME's. So we can claim this to be a pioneering work that ends by finding that, for SME's, both the levels of SR information and the actions they carry out are predictors of their level of SR disclosure. Hence, SME's are free of any effect of opportunism that is more typical of large enterprises. The work is intended to contribute to advancing the line followed by studies on SR in environmental performance – a topic of great current interest.

Following this Introduction, the relevance for SME's of information on SR is addressed, and some of the literature corresponding to work in the environmental field is discussed. The following section explains the orientation to a strategy of environmental responsibility from a market-based perspective. Then the methodological approach used in the present study is described, together with the technical data of the study and of the sample. After presenting an analysis and discussion of the results, the study concludes with its key findings, and reflections on its limitations and the need for further research in this direction.

Social responsibility and environmental management in SME'sSince 2001, with the publication by the European Union of the Green Paper: Promoting a European Framework for Corporate Social Responsibility, there have been many advances in this line. Social Responsibility (SR) is defined as “a set of commitments of various types, economic, social and environmental, adopted by enterprises, organizations and public and private institutions that add value to fulfil their legal obligations, contributing both social and economic progress within the framework of sustainable development” (MTAS, 2005). Very recently, the European Union in its renewed strategy notes “the responsibility of enterprises for their impacts on society”, with specific reference to the need for collaboration with stakeholders to “integrate social concerns, environmental and ethical, compliance with human rights and consumer concerns into their business operations and core strategy” (European Commission, 2011: 7).

The importance of the above concept, increasingly widespread in organizational practice, coupled with the globalization of markets and the need to be competitive in the new international context, has positioned SR as a source of competitive advantages (Bagnoli and Watts, 2003; Galbreath, 2006; Porter and Kramer, 2006; Bies et al., 2007; Maxfield, 2008; Weber, 2008; Siltaoja, 2009; Fernández-Kranz and Santaló, 2010; Marcus et al., 2011; Apospori et al., 2012). A positive association between SR and economic growth is observed (Navarro and González, 2006). There is no doubt that achieving better positions against the competition is an objective of every business, not just large firms. Indeed, SME's are also working to achieve a good market position by promoting their SR (Longo et al., 2005; Perrini, 2006; Sweeney, 2007; Fisher et al., 2009; Vidal et al., 2010; Gallardo-Vázquez et al., 2013; Ladzani and Seeletse, 2012; Apospori et al., 2012; Frai-Andrés et al., 2012; Sánchez-Hernández and Gallardo-Vázquez, 2012). In particular, SME's are voluntarily orienting themselves towards the environment (Aragón-Correa et al., 2005; Fenwick, 2007; López-Gamero et al., 2008; Martín-Tapia et al., 2010).

The increasing research in the field of SR reflects its multidimensionality, i.e., the breadth of the concept and the variety of different aspects or actions that it incorporates. Based on the well-known “Triple Bottom Line” approach (Elkington, 1994, 1998), the research that followed in that line shows it to be at the origin of the focus of SR issues (Wood and Jones, 1995; Carroll, 1999; Maignan and Ferrell, 2000; Turker, 2008; Orlitzky, 2011). According to Elkington (1994), firms should pursue three distinct but complementary types of objective – economic, social, and environmental. In this paper, we focus on the environmental dimension of SR for SME's as a sub-construct with its own identity.

The SR approach in the environmental dimension for SME's has been addressed by authors such as Petts (2000), Rutherfoord et al. (2000), Biondi et al. (2002)Patton and Worthington (2003), Gumede (2004), and McKeiver and Gadenne (2005), Mir (2008), Clarkson et al. (2008), Martín-Tapia et al. (2010). Clarkson et al. (2008) noted that a still unresolved research issue is the empirical association between the level or quantity of environmental disclosures and performance in this area of a firm's operation. Although empirical research on SR focused on the environmental field is extensive, there is insufficient evidence in the sense of the above association, so that the present study is an attempt to fill this gap. There have been contributions that support the influence of SR information on the outcomes of environmental actions. Thus, Shrivastava (1995), Parkinson (2003), Solomon and Darby (2005), and Ortiz de Mandojana et al. (2011) analyze the effect of a firm's possession of SR information on its proceedings or environmental responses. The results showed this effect to be clearly positive, lending support to the relationships that we propose in the present work which have been less frequently addressed in the literature, but have a theoretical logic that we shall attempt to substantiate.

Finally, there is no consensus on what links can be established between the disclosure of SR and environmental response. There is evidence supporting a positive effect of the action or performance achieved with the disclosure of SR (Dye, 1985; Verrecchia, 1983; Al-Tuwaijri et al., 2004; Clarkson et al., 2008). However, one cannot affirm the existence of any positive effect in the opposite direction. Thus, Ingram and Frazier (1980) found a lack of association between disclosure and environmental performance, and Bewley and Li (2000) observed a negative relationship.

From an analysis of the relationship existing between the three sub-dimensions to be addressed in the next section forming what we call the orientation to environmental responsibility consisting of SR information, the organization's environmental response to their stakeholders, and the disclosure/dissemination the firm conducts of its own SR, the aim is to provide answers to two major questions in research: Is the SR information owned by the firm a determinant of the environmental actions it carries out and of the disclosure it makes of those actions? And, are the firm's environmental actions the determinant of the degree of disclosure?

Market orientation from the SR perspective: an environmental approachA market oriented organization carries out actions under the current marketing concept of satisfying customer needs (Kholi and Jaworski, 1989, 1990; Narver and Slater, 1990; Atuahene-Gima, 1995; Lukas and Ferrell, 2000; Matsuno et al., 2002; Jiménez-Jiménez and Cegarra-Navarro, 2007; Ledwith and O¿Dwyer, 2009). Kholi and Jaworski (1990) established that Market Orientation (MO) was made up of three interrelated sub-constructs: (i) the generation of market intelligence on current and future needs of customers; (ii) the disclosure of such intelligence within the organization; and (iii) the organizational ability to respond to this market intelligence. According to those authors, the generation and disclosure of market intelligence are the elements necessary for the organization to respond satisfactorily to its needs. Narver and Slater (1990), with a more strategic approach, highlight the ability of MO to integrate and coordinate the functions within the organization and build competitive advantage. For those authors, MO is a type of organizational culture that promotes the behaviours necessary to create more value for customers and, consequently, a higher profit for the organization long term. In both approaches, MO is conceived of as a philosophy of action, a way of operating in markets that goes beyond the marketing department and that pervades all departments of the organization, promoting cross-functional collaboration towards the organizational goal of satisfaction of market needs and value creation for the organization.

In addressing the construct of MO from the perspective of SR, the concept of market expands so that it is no longer enough to satisfy customers (agents of interest, among others, as indicated by Stakeholder Theory).1 In this new framework for action the organization aims to meet the demands of its key stakeholders (Kaler, 2004; Orlitzky and Swanson, 2012). The academic literature shows that SR satisfies not only external agents, whether clients (Brown and Dacin, 1997; Sen and Bhattacharya, 2001; Luo and Bhattacharya, 2006) or shareholders (Clarkson, 1995; Griffin and Mahon, 1997; Orlitzky et al., 2003), but also internal agents, whether managers (Lerner and Fryxell, 1994; Mahoney and Thorne, 2005) or employees (Turban and Greening, 1997; Albinger and Freeman, 2000).

As in the classical conception of MO, our expanded concept of orientation to stakeholders is closely related to the use of information, in our case information on SR. In the discipline of marketing, the tools of market research are particularly relevant. Therefore, if the firm wants to create value for their markets through its SR actions, to coordinate resources, and to provide effective organizational responses, its actions should be based on information from these markets and variables that may affect their satisfaction.

Before going into the analysis of the indicated causal relationships, it is necessary to address in depth various aspects that have been mentioned above. We first refer to the importance to businesses of the SR information they receive. The European Commission (EC) issued a report entitled “European SME's and social and environmental responsibility” (2002) which justifies the importance of the topics covered to these types of businesses, including information. Later, the study “CSR Communication: talking to people who listen” (APCO, 2004) also highlighted the importance for firms of the transmission of information on SR, an aspect that has subsequently been treated by many authors (Capriotti and Moreno, 2007; Nielsen et al., 2009; Fisher et al., 2009; Hammann et al., 2009; Vidal et al., 2010; Patenaude, 2011). With the same emphasis on the importance of information, the Industrial Development Organization of the United Nations (2002) published the report “Corporate Social Responsibility: Implications for small and medium enterprises in developing countries”. At the Spanish level, the Ministry of Industry, Tourism and Trade (2009) issued the report “CSR and SME's. From speaking to implementation. A European perspective”. It identifies actions that, at the European level, are being made to support the implementation of SR in SME's, and among which may be mentioned the ones related to the disclosure of SR, the development of policies tailored to SME's, the creation of mechanisms for disclosure, the development of guidelines and other means, as well as training in these businesses.

In connection with the disclosure of information, it is notable that, after the publication of the Corporate Report (ICAEW, 1975), social information disclosure by firms has grown considerably. Furthermore, Roberts (1998) indicates that the activities of SR and disclosure of information constitute a part of the strategic initiatives of the firm. Another aspect to consider endorsing the importance of disclosure is the acquisition of legitimacy on the part of the firm (Hooghiemstra, 2000; Deegan, 2002; Capriotti and Moreno, 2007), and good communications help in this sense. The literature indicates that the purposes of seeking legitimacy often constitute a strong motivation for internal and external communication about positive developments to the agents of interest, since those groups have the right to know (Deegan, 2002; Galetzka et al., 2008; Mobus, 2012; Orlitzky and Swanson, 2012). In this sense, the acquisition of legitimate behaviour by the firm with respect to society involves the development of constant change, and therefore the firm is responsible for its actions within the context in which it operates (Deegan, 2000; Mobus, 2012).

Being able to communicate socially responsible actions constitutes a factor with which to measure social legitimacy, allowing one to discriminate successful firms from others which have not succeeded. Clearly the inclusion of economic, social, and environmental information data within the decision-making processes is a significant progression for any organization (Adams and Frost, 2008). Failure to consider such data would make it difficult to see how the organization could improve its sustainable development.

With regard to the environmental response, and in line with the significant line of study based on the correlation between business performance and the actions of SR, which is termed in the Anglo-Saxon world “the business case for corporate responsibility” (Weber, 2008; Hart, 2010; Carroll and Shabana, 2010), the present work assumes that SR can be as strategic as any other business orientation that seeks profit maximization. This implies that a social approach could coexist with a purely economic approach. By supporting this idea, there are studies that attempt to integrate the concept of SR and corporate strategy (Galbreath, 2006; Bies et al., 2007; Maxfield, 2008) which recommend using the same framework of analysis to determine the core of a business and convert the orientation to SR into a source of competitive advantage (Porter and Kramer, 2006). Bagnoli and Watts (2003) state that the implementation of good citizenship strategies leads firms to maximize their profits. Fernández-Kranz and Santaló (2010), for example, have shown empirically that the most competitive firms have the highest levels of SR. They explain this circumstance based on the strategic nature that SR has in these firms, independently of other considerations of additional social altruism.

In the strategic consideration of SR, the current economic crisis should not be attributed merely to a change in the economic cycle but also to the lack of values and ethical principles in the functioning of organizations as Melé et al. (2011) noted. Furthermore, the solution to the crisis can come from the social innovations and responsible behaviour (Goldsmith et al., 2010) in which SR reaches it highest strategic value. Within the strategic approach of SR and the Triple Bottom Line perspective (Elkington, 1994, 1998), we are especially interested in focusing on the environmental dimension. We do not want to downplay the social and economic aspects which also shape SR strategy. However, we believe that, the environmental approach has received a specific and very thorough treatment, which is certainly a cause requiring its independent study for various reasons.

Firstly, in recent years, there have been many firms that have adopted an Environmental Management System,2 defining a management system whose goal was to encourage organizations to manage and reduce their environmental impact. This practice has been carried out very extensively, being a clear example of manifest environmental responsibility, with awareness of the need to use a tool with the potential to introduce an eco-efficient behaviour and vision into the firm's existing management systems. Secondly, more recently, concerns about the environmental dimension are being compounded by the constant and increasing environmental degradation. Numerous major landmarks, such as the oil spill of British Petroleum (BP) in the Gulf of Mexico in 2010, floods, pests, the disastrous Ok Tedi copper and gold mine contamination (New Guinea), among others, demonstrate the need for organizations to move away from negative and defensive positions, and begin to use new instruments for environmental protection on a voluntary basis within the philosophy of SR (Fernández de Gatta Sánchez, 2004).

In general, the disclosure of SR information, and therefore also environmental information, is part of the branding of corporate identity, an aspect of its behaviour that distinguishes one firm from another and strategically differentiates it from the competition (Marwick and Fill, 1997; Gray and Balmer, 1998; Olutayo Otubanjo and Melewar, 2007; Holtzhausen and Fourie, 2008; Bewley and Li, 2000; Patenaude, 2011; Mobus, 2012). In this sense, environmental responsibilities are factors that govern the formation of opinions about a firm's reputation (Capriotti and Moreno, 2007). For this purpose it is necessary to have indicators of environmental development that demonstrate what actions are being carried out by firms which show a strong orientation to SR. On this view, initially put forward by Elkington (1998), other opinions have later emerged pointing out that it represents an important means with which to evaluate and compare current corporate environmental developments.

There are many aspects that determine differences in firms’ environmental responses: from membership in Associations (King and Lenox, 2000) to the pressure of the media (Bansal and Clelland, 2004) or environmental regulation (González et al., 2006), for example. Although different, all of them involve the possession and use of socially responsible information capable of determining the orientation of the firm's actions. However, in this sense, Ortiz de Mandojana et al. (2011:223), and based on Shrivastava's work (1995), state that “because the benefits from the commitment to sustainable development are usually long-term, the lack of information, … usually manifests as a certain discouragement regarding this type of strategies”. From that, in a positive sense, one deduces that the availability of information on SR determines a predisposition to act pro-actively in sustainable development, and therefore achieve a better response in the environmental field.

Parkinson (2003) has pointed out that information can provide improvements in SR practices. In addition, Solomon and Darby (2005) added that firms that have more information about SR have, through their managers, a solider reflection process. This leads them to adopt higher standards of performance, including their environmental perspective.

Another determinant factor of performance is the type of ownership of firms. Thus, following Ortiz de Mandojana et al. (2011), firms who have more knowledge and information about initiatives to carry out as well as more training to understand their implications will in turn be better able to provide economic incentives that promote those initiatives. This usually is the case when the ownership is distributed in the hands of institutional investors, given the economies of scale that are generated in benefit of the profitability of the actions undertaken. Therefore, the type of ownership determines the type of information and the environmental performance.

But also, in relation to the incorporation of new owners to the firm, some authors have found that environmental information is very valuable when investors are seeking to know about the environmental performance generated (Cournier and Magnan, 1997; Li and McConomy, 1999; Richardson and Welker, 2001; Clarkson et al., 2004). All the comments in the literature reflect the strong relationship between the SR information held by the firm and its environmental responses. Clearly, a strong response in this aspect of SR is motivated by the possession of a high level of information.

Furthermore, Parkinson (2003) suggested that increased SR information affects corporate behaviour, which leads us to posit a link between environmental response and disclosure. Solomon and Darby (2005) reported that disclosures served for the firm to gain awareness of the aspects that are required of it within the area of SR. However, in the literature on the various components of the orientation to environmental responsibility, there does not exist any empirical evidence linking the environmental responses observed in firms with the dissemination of SR at a general level. One finds some studies that relate environmental performance to disclosures of this nature, but there is a lack of consensus (Al-Tuwaijri et al., 2004; Hughes et al., 2001; Patten, 1992). On one hand, the theory of voluntary disclosure (Dye, 1985; Verrecchia, 1983; Al-Tuwaijri et al., 2004) indicates a positive association by stating that firms that have a good performance will reflect it in indicators, and will provide this information to other firms through disclosure. Also, Clarkson et al.’s paper (2008) analyzed the relationship between environmental performance and the level of disclosure of this nature in the social and environmental reports or Web pages, finding a positive relationship in this sense. On the other hand, references of a lack of relationship are found, such as Ingram and Frazier's work (1980) which concludes that there is a lack of any association between disclosure and environmental performance. Also in this sense, Bewley and Li (2000) examined the factors associated with environmental disclosures in Canada, and found that firms with lower environmental performance were more likely to disclose, so that the authors therefore deduce a negative relationship.

In this context and as noted previously, since SME's are a priori less subject to pressure from stakeholders than large firms, they would be less conditioned when internally and externally disclosing their environmental achievements. Thus, under the theoretical approach of legitimacy theory and driven by the motivation of their managers, the SME's that are most environmentally responsible are those that most report their findings. Given the above, we believe it is important to determine the direction of causality between the components of the orientation to environmental responsibility with the empirical study to be presented in the next section.

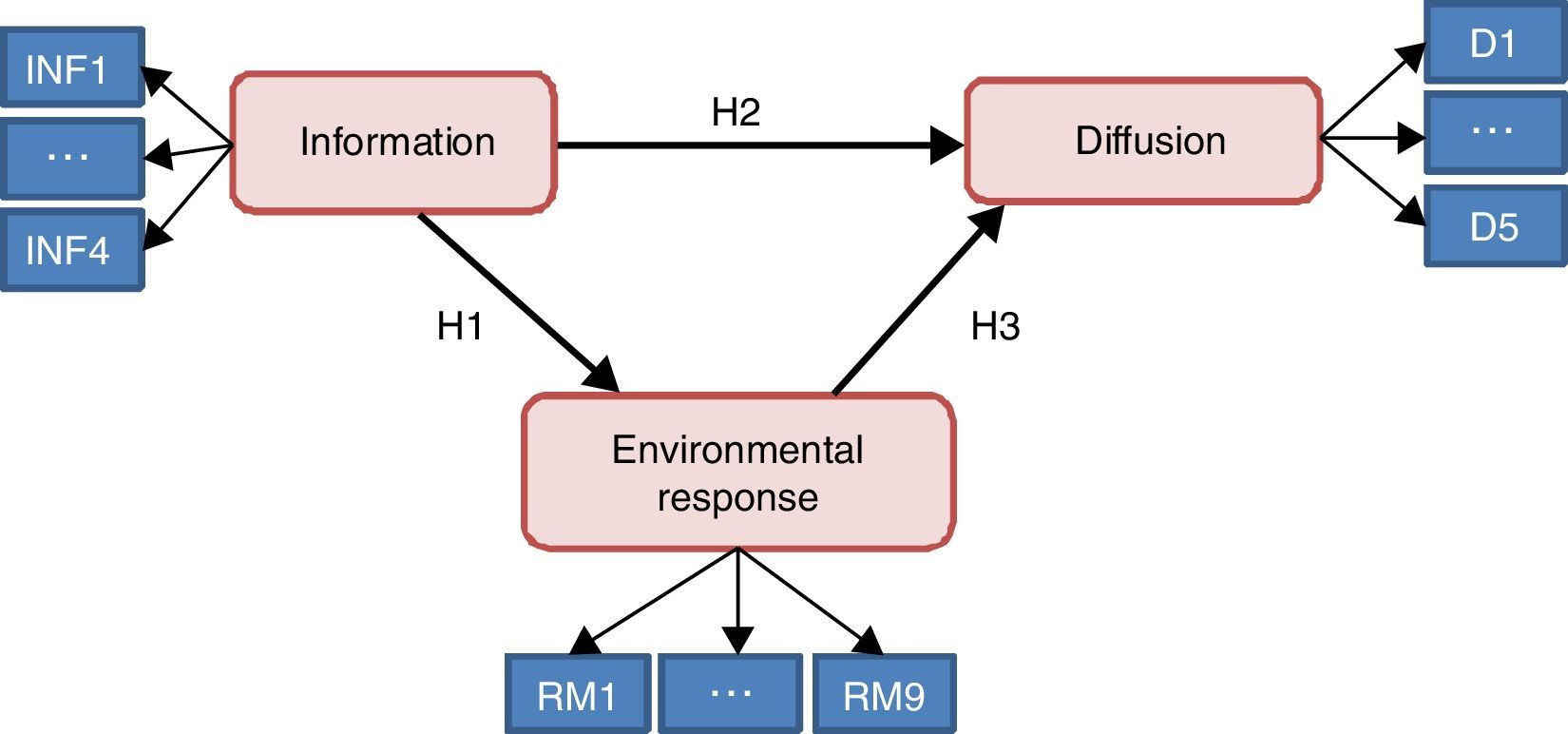

Thus, and based on the review of the academic literature and the research gaps identified, the following hypotheses are formulated which will be tested below:H1 There is a direct and positive relationship between the SR information received by SME's and their environmental action. There is a direct and positive relationship between the SR information received by SME's and the disclosure they make of their environmental action. There is a direct and positive relationship between environmental actions undertaken by SME's and the extent to which they disclose environmental information.

The conceptual model we propose (Fig. 1) presents three related latent variables that conformate the orientation to environmental responsibility, in which the SR information which is received by SME managers appears as an independent variable. In parallel with the original postulates of Kholi and Jaworski (1990), the information will have a direct and positive effect both on organizational response on the environment and on the disclosure made of the information received. In the model presented, disclosure is understood broadly, both internally within the organization and externally fulfilling the role of informing society about the actions the firm carries out. Finally, and focusing the model on the environmental dimension, the third variable refers to the positive attitude towards conservation and preservation of the environment, which expresses a greater or lesser degree of the firm's environmental performance.

MethodsSample and procedure

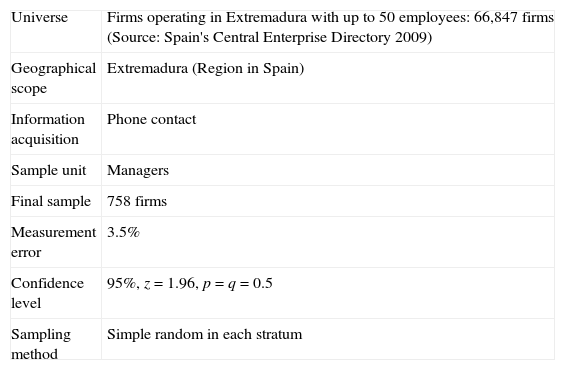

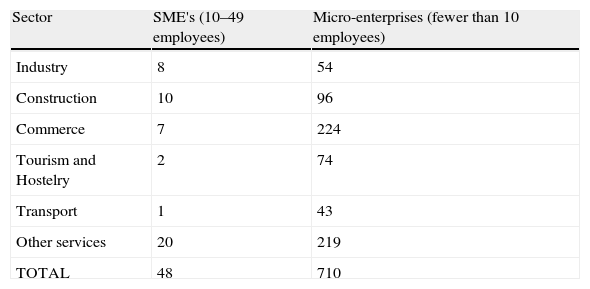

In the empirical analysis, we have analyzed the relationship between the three sub-domains of environmental responsibility orientation, as an expression of corporate environmental performance: SR information, the organization's environmental response to stakeholders (understood as the form of managing and minimizing the organization's impact on society, which is an objective of any firm aware of environmental issues), and SR disclosure. The sample selected for the study was 758 small representative firms of the businesses of the Autonomous Community of Extremadura with the corresponding default replacement firms to control the rate of non-response. The objective universe was drawn from the Central Companies Directory (CCD). Before the study, the representativeness of the sample of firms that participated in the survey was calibrated according to the objective universe by setting weights according to the strata defined. In order to justify the validity and representativeness of the sample, and to identify possible biases regarding the characteristics of the population under study, statistical tests were conducted comparing the structure of the sample with population data from the CCD. The specifications of the study are presented in Table 1, and the characterization of the sample by sector and number of employees distinguishing between small businesses and micro-enterprises in Table 2.

Study data sheet.

| Universe | Firms operating in Extremadura with up to 50 employees: 66,847 firms (Source: Spain's Central Enterprise Directory 2009) |

| Geographical scope | Extremadura (Region in Spain) |

| Information acquisition | Phone contact |

| Sample unit | Managers |

| Final sample | 758 firms |

| Measurement error | 3.5% |

| Confidence level | 95%, z=1.96, p=q=0.5 |

| Sampling method | Simple random in each stratum |

The field work was based on phone calls to the heads of the firms during the month of May 2010 using CATI (Computer Aided Telephone Interviewing). Managers were contacted previously to mark the day and time of conducting the survey to ensure that it took place at an appropriate time so as not to interfere with their activities or obligations or priorities, noting that the average time duration of each interview was 14.35min. At the time of the call, the survey questions were displayed on the screen of the interviewer, who read the questions to the manager. The responses were introduced by the interviewer into a computer application, ensuring that there were no mistakes in registering the data. The participation rate was 11.07%, which corresponds to the percentage of firms in which it was possible to locate an interlocutor who agreed to participate in the study.

To achieve the objective of 758 surveys, it was necessary to contact 6850 firms in Extremadura. There were a total of 18,820 calls, as follows: 59.30% of the firms did not answer the call; 13.66% of the firms expressed a lack of interest or refusal to participate in the study; 12.20% of the cases corresponded to an out-of-range or invalid response; and 3.77% of the firms had a wrong phone or non-existent. At a later stage it was found, with a random sample of 5% of the participating firms, that the questionnaire was answered fully and effectively by the manager responsible for the firm.

MeasuresFor the measurement of the constructs, different items were defined and collected in a questionnaire. Firstly, the questionnaire was sent to 20 selected executives for pre-test, and then it was adjusted according to their specifications, in particular correcting the wording of the statements to allow the respondent a clear understanding of what was being asked. It was found that the questions were clear and direct because the respondents answered quickly, securely, naturally, and spontaneously. However, we proceeded to incorporate small adjustments to the content adapted to the reality of the SME to finally determine that the questionnaire was realistic. Later,3 a qualitative study with some of the firms participating in this study satisfactorily confirmed the meaning of what they wanted to express when they were responding to the various questions, and that they did so with a high degree of homogeneity. The questionnaire consisted of 18 questions on a Likert scale of 10 points where the managers had to choose according to their perceptions between “strongly disagree” to “strongly agree”.

Four questions were devoted to collecting data on the independent latent variable information to measure the extent to which employers were concerned about information and were aware of issues of SR.

The following nine questions were devoted to the perceptions of managers on aspects of environmental responsibility measuring the variable Response. The issues addressed in this mediating latent variable were mixed. The variable includes two kinds of items: environmental actions and other items related to intentions such as the acceptance of the importance of undertaking environmental actions if possible or necessary. Thus, this variable broadly observed whether the environmental response of entrepreneurs in small businesses was positive or not.

Finally, the questionnaire included five questions for the dependent variable dissemination covering matters relating to the inclusion of SR in the strategy and the degree of SR disclosure.

Technique: structural equationsIn order to empirically analyze the proposed conceptual model, we selected structural equation modelling (SEM) as the appropriate methodological tool because it offers the possibility of combining and confronting theory with empirical data, performing multiple regressions between several latent variables (not directly observable, expressed by a set of observable variables that serve as indicators) so as to provide scientific causal explanations beyond description and associations (Fornell and Larcker, 1981). In this study, we used the software developed by Ringle et al. (2005) and available by subscription and authorization of the authors, called Smart-PLS (Partial Least Squares). It is based on parameter estimation, and it has the ability to minimize residual variances of the endogenous variables by maximizing the variance explained (R2) of the dependent variables. In this way, one achieves the primary objective of this technique which is to predict the dependent variables.

The orientation to environmental responsibility of business managers in Extremadura was analyzed in detail following the MO logic orientation of Kholi and Jaworski (1990) (information, disclosure, and responsiveness), considering the willingness to respect and preserve the environment and the environmental performance of firms.

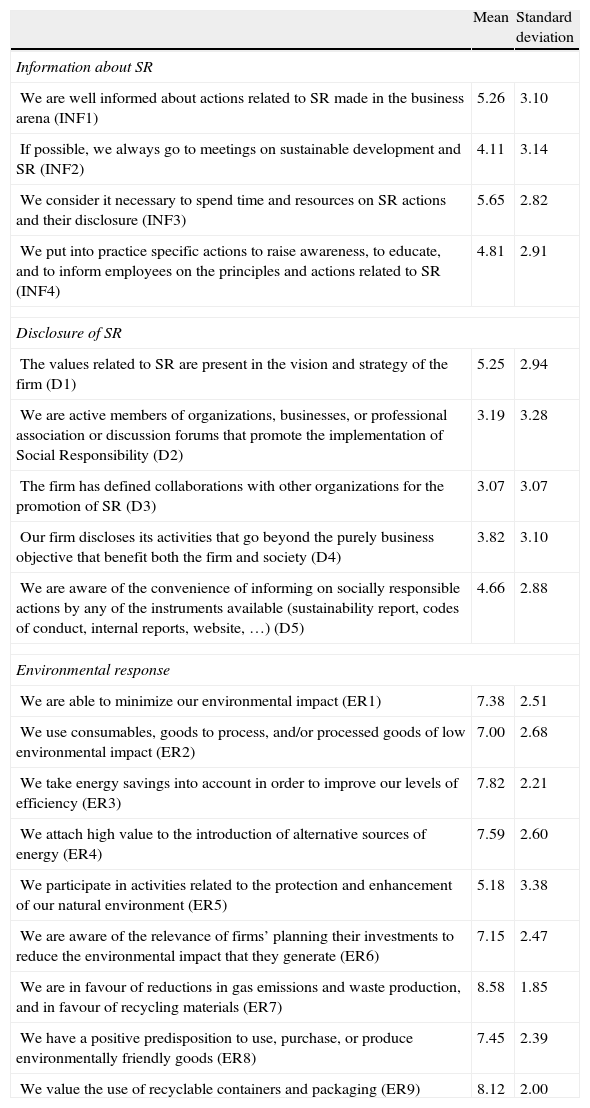

Analysis and discussion of resultsDescriptive statisticsBefore addressing the structural analysis, we show in Table 3 the measurement items used for constructs with the descriptive statistics of mean and standard deviation.

Model indicators.

| Mean | Standard deviation | |

| Information about SR | ||

| We are well informed about actions related to SR made in the business arena (INF1) | 5.26 | 3.10 |

| If possible, we always go to meetings on sustainable development and SR (INF2) | 4.11 | 3.14 |

| We consider it necessary to spend time and resources on SR actions and their disclosure (INF3) | 5.65 | 2.82 |

| We put into practice specific actions to raise awareness, to educate, and to inform employees on the principles and actions related to SR (INF4) | 4.81 | 2.91 |

| Disclosure of SR | ||

| The values related to SR are present in the vision and strategy of the firm (D1) | 5.25 | 2.94 |

| We are active members of organizations, businesses, or professional association or discussion forums that promote the implementation of Social Responsibility (D2) | 3.19 | 3.28 |

| The firm has defined collaborations with other organizations for the promotion of SR (D3) | 3.07 | 3.07 |

| Our firm discloses its activities that go beyond the purely business objective that benefit both the firm and society (D4) | 3.82 | 3.10 |

| We are aware of the convenience of informing on socially responsible actions by any of the instruments available (sustainability report, codes of conduct, internal reports, website, …) (D5) | 4.66 | 2.88 |

| Environmental response | ||

| We are able to minimize our environmental impact (ER1) | 7.38 | 2.51 |

| We use consumables, goods to process, and/or processed goods of low environmental impact (ER2) | 7.00 | 2.68 |

| We take energy savings into account in order to improve our levels of efficiency (ER3) | 7.82 | 2.21 |

| We attach high value to the introduction of alternative sources of energy (ER4) | 7.59 | 2.60 |

| We participate in activities related to the protection and enhancement of our natural environment (ER5) | 5.18 | 3.38 |

| We are aware of the relevance of firms’ planning their investments to reduce the environmental impact that they generate (ER6) | 7.15 | 2.47 |

| We are in favour of reductions in gas emissions and waste production, and in favour of recycling materials (ER7) | 8.58 | 1.85 |

| We have a positive predisposition to use, purchase, or produce environmentally friendly goods (ER8) | 7.45 | 2.39 |

| We value the use of recyclable containers and packaging (ER9) | 8.12 | 2.00 |

On one hand, about the information that managers in Extremadura have regarding SR aspects, it can be said that it is poor, but that the managers stressed that it necessary to spend time and resources in developing responsible actions and improving the disclosure of SR (INF3), which reaches a mean of 5.65 on a scale of 0–10. Although this is above the average, one cannot ignore that it is a highly interesting aspect that should be improved in the future. On the other hand, more than half of these managers appear not to be well informed about the actions of SR that are taking place in the business arena (INF1), and only 48% score more than 5 points on this scale. Bearing in mind the importance of information for action, it seems relevant for regional policy to start taking steps to raise firms’ awareness and insightful information on the benefits of SR, encouraging the adoption of appropriate actions.

With regard to SR disclosure, managers in Extremadura are still not very aware of the importance of communicating their social outcomes to stakeholders either through a social report or through other dissemination mechanisms that are available. Although responsible values are present in the vision and strategy of the firm (D1), 67% of the respondents did not give more than 5 points to this aspect.

Regarding the environmental response, we found that, in general, the business orientation is positive. Issues related to environmental impact have fairly high scores, showing the business managers’ awareness of this area and the degree of commitment that firms have with respect to the reduction of their environmental impact, which we interpret as a good environmental orientation.

One can make some more detailed reflections on the perceptions of managers that show the drawbacks and support they found when faced with the management of SR. Regarding the item “Developing specific actions to raise awareness, to educate and to inform employees on the principles and actions related to SR” (INF4), and taking into account that the vast majority of firms in the study have few or no employees, we highlight the fact that the answer is given by the owner/manager in person. We can say that the managers surveyed are beginning to worry about their own training in SR, and this may trickle down, from their own conscience, to informing and training their employees. In addition, if small size can be understood as a problem for implementing SR, we can say that SME's are not alone. Thus, in relation to the item indicating that the firm has defined collaboration with other entities for the promotion of SR (D3), the respondents refer to collaboration with Social Economy organizations. In some cases analyzed, and of particular interest, collaboration is so intense and frequent that we could even say that these organizations are part of the value chain of the firm surveyed. However, in relation to the item “Our firm disclosed the activities that go beyond the natural object of business but benefit both business and society” (D4), the study indicates that managers in Extremadura have not yet considered the disclosure of their responsible actions.

However, for the item “We are aware about the convenience of collecting socially responsible actions with the instruments available (sustainability report, codes of conduct, internal reports, Web page …)” (D5), there is evidence of an awareness of SR, the need to put the firm's responsible actions into practice, and the convenience of disclosure in a document or on the Web page of the firm. In summary, one can speak optimistically about the perceptions of business managers of the need for greater disclosure of SR.

After this discussion of the details of the survey, the proposed theoretical model will be analyzed and interpreted in three stages. The first two are devoted to explaining the validity of the overall model, and the third to analysing the results of causality that were found in the relationships between constructs to verify the hypotheses.

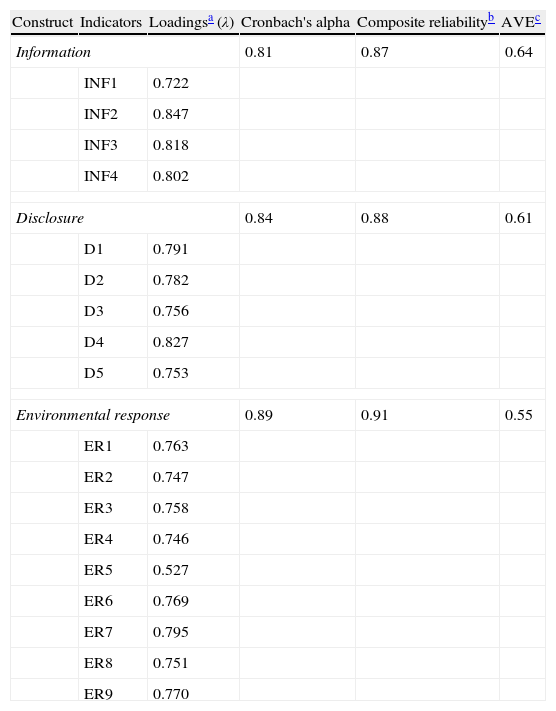

Validity and reliability of the modelThe measurement model evaluates whether the theoretical constructs are properly measured by the observed items. This analysis was done regarding attributes of validity (whether they really are measuring what we wanted to measure) and reliability (whether they are stable and consistent). To this end, we proceeded to calculate the individual item reliability, the internal consistency of the scales, and the analysis of the average variance extracted (AVE). This information is included in Table 4.

Measurement model.

| Construct | Indicators | Loadingsa (λ) | Cronbach's alpha | Composite reliabilityb | AVEc |

| Information | 0.81 | 0.87 | 0.64 | ||

| INF1 | 0.722 | ||||

| INF2 | 0.847 | ||||

| INF3 | 0.818 | ||||

| INF4 | 0.802 | ||||

| Disclosure | 0.84 | 0.88 | 0.61 | ||

| D1 | 0.791 | ||||

| D2 | 0.782 | ||||

| D3 | 0.756 | ||||

| D4 | 0.827 | ||||

| D5 | 0.753 | ||||

| Environmental response | 0.89 | 0.91 | 0.55 | ||

| ER1 | 0.763 | ||||

| ER2 | 0.747 | ||||

| ER3 | 0.758 | ||||

| ER4 | 0.746 | ||||

| ER5 | 0.527 | ||||

| ER6 | 0.769 | ||||

| ER7 | 0.795 | ||||

| ER8 | 0.751 | ||||

| ER9 | 0.770 | ||||

Scale reliability is considered satisfactory when composite reliability is above 0.70 (Nunally, 1978).

It can be seen that all items considered to measure the latent variables or constructs of the model – except RM5 related to planning investment for environmental impact reduction – meet the strictest criterion for the acceptance of an indicator as part of a construct. That is by possessing a loading greater than 0.707 (λ>0.7). This implies that the variance shared between the construct and its indicators is greater than the error variance (Carmines and Zeller, 1979). However, some authors believe that this rule should not be so strict, and consider that loadings of 0.5 or 0.6 (Falk and Miller, 1992) are acceptable in the early stages of development of a scale (Chin, 1998) or when the scales are applied in different contexts (Barclay et al., 1995). In this study all the indicators considered in the model reflected the constructs defined and therefore accepted. That is, it was not necessary to eliminate items from the model because all of them met the criterion of individual reliability.

Regarding the composite reliability of constructs, which is a more demanding criterion than Cronbach's alpha, as recommended by Nunally (1978), it would have been considered acceptable and sufficient to have values above 0.7, given the embryonic nature of the structural analysis in the field of SR. However, the proposed model yields very satisfactory values greater than 0.80 (0.87 information; 0.88 disclosure; 0.91 environmental response) as required in basic research to validate scales. Therefore, the internal consistency of the constructs of the model is verified.

To evaluate the convergent validity, we used the average variance extracted (AVE) developed by Fornell and Larcker, 1981. This parameter expresses the amount of variance that a construct obtains from its indicators as against the amount due to measurement error. It should be greater than 0.5 (Fornell and Larcker, 1981), ensuring that 50% or more of the variance of the indicators is accounted for. In the model, the AVE of the constructs exceeds the recommended minimum of 0.5 (0.64 information; 0.61 disclosure; 0.55 environmental response). In each case, the indicators account for more than fifty percent of variance of the constructs, specifically, and referring to the best result, 64% in the case of information.

Assessment of the structural modelOnce the measurement model has been satisfactorily evaluated (valid and reliable measures regarding the constructs), it is necessary to carry out a correct interpretation of the internal or structural model in order to verify that this model includes the relationships between the latent variables pointed to by the theory.

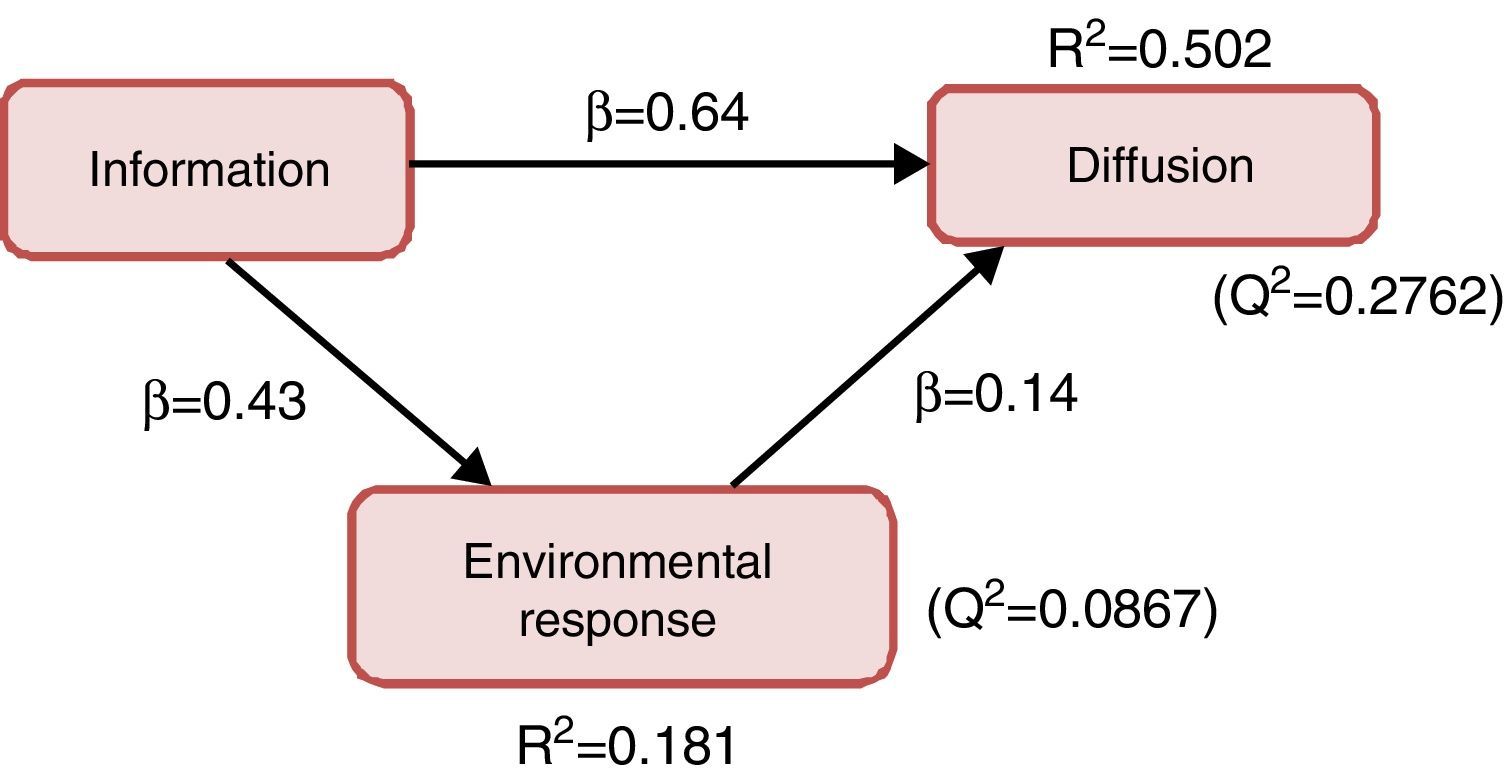

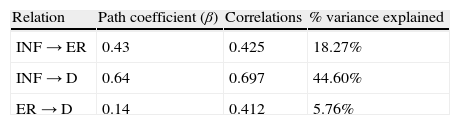

The structural model evaluates the weight and magnitude of the relationships between variables. To carry out this assessment, we analyzed the explained variance of the endogenous variables (R2), the path coefficients or standardized regression weights (β), and their significance levels. Given that the main objective of PLS is prediction, the goodness of a model is determined by the strength of each structural path. This was analyzed by using the R2 value (explained variance) for the dependent latent variables. Thus, for each path between constructs, the desirable values should be at least equal to or greater than 0.1 (Falk and Miller, 1992). As shown in Fig. 2, which presents the R2 values, the model has high predictive power.

Supporting the main hypothesis of this work, one can see that the latent variable information can explain up to fifty percent (R2=0.50) of the environmental dissemination of the firms surveyed. When we add the environmental response to the effect of information (R2=0.18) we get an explanation of about seventy percent of the environmental response, highlighting the importance of managing these variables. To measure the relevance of the prediction of the dependent construct, PLS uses the Q2 index of Stone–Geisser that is calculated as a cross product of commonalities (λ2) with the AVE indicators. According to Chin (1998), we can say that there is significance in the prediction of the constructs because we obtained positive Q2 values.

However, focusing on the analysis of the standardized regression weights, they must be interpreted, as in the case of the β coefficients of traditional regressions, as indicators of the relative strength of the statistical relationships. In this regard, Chin (1998) proposed that the analysis should provide standardized path coefficients exceeding values greater than 0.2 and ideally 0.3. But Falk and Miller (1992) are less demanding and proposed as a rule of thumb for accepting the predictor effect of a variable on another that it should explain at least 1.5% of the variance of the endogenous variable. To calculate the variance explained, the path coefficient β was multiplied by the corresponding correlation coefficient between the two variables.

In the model, we can only clearly confirm the predictive power of the information variable on the endogenous variable dissemination in the small firms under study. In Table 5 we see that information accounts for up to 18.27% of the environmental response of these small firms and 44.6% of the dissemination, constituting an important result of the investigation. Meanwhile, the variable environmental response accounts for only 5.76% of the variance of the dissemination, which can be interpreted as a satisfactory result even if the variable reveals itself to be less significant than expected. These results will be discussed later when testing the hypotheses.

Although in principle, as argued by Cepeda and Roldán, 2004, there are no proper measures in PLS goodness-of-fit, Tenenhaus et al. (2005) have developed a global criterion for goodness-of-fit that values both the quality of the measurement model through the mean AVE of the latent variables with reflective indicators and the quality of the structural model using the mean of the R2 of the endogenous variables. The indicator called GoF (goodness-of-fit), as does R2, ranges between 0 and 1. Since no quality thresholds have been determined for this index, it is understood that the higher the value, the better the model fit. In this analysis the GoF was 0.444, a positive value that will be helpful in future extensions of this research to compare the goodness of the current model with other alternative models.

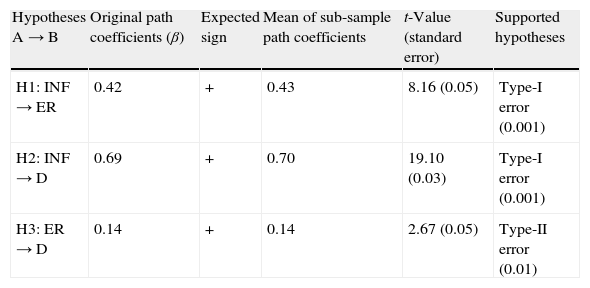

Hypothesis testingIn this third and final stage of analysis, related to the goodness-of-fit of the model, but now in order to confirm the working hypotheses, PLS employs a nonparametric resampling technique that offers both the standard error and the values of Student's t-statistic. Thus, to calculate the significance of the path coefficients, a bootstrapping test was performed with 500 subsamples using a two-tailed t-distribution with n−1 degrees of freedom, where n is the number of sub-samples. Results were very satisfactory. Table 6 reveals that all structural paths outlined in the model are significant, although with different levels of meaning, so all hypotheses are confirmed. The positive signs of the coefficients β for the relations of the information variable with the other two variables in the model show the expected behaviour according to the theory.

Hypothesis testing with a bootstrap procedure.

| Hypotheses A→B | Original path coefficients (β) | Expected sign | Mean of sub-sample path coefficients | t-Value (standard error) | Supported hypotheses |

| H1: INF→ER | 0.42 | + | 0.43 | 8.16 (0.05) | Type-I error (0.001) |

| H2: INF→D | 0.69 | + | 0.70 | 19.10 (0.03) | Type-I error (0.001) |

| H3: ER→D | 0.14 | + | 0.14 | 2.67 (0.05) | Type-II error (0.01) |

The hypotheses H1 and H2, which determined the structural path between information and the other variables in the model, response and disclosure, were robustly confirmed with just a 0.1% probability of making the mistake of rejection. Similarly, the hypothesis H3 that determined the structural path that relates environmental response with dissemination also is supported with an error slightly higher than 1%. These results confirm the validity and reliability of both the measurement model and the structural model proposed.

In view of the results, we can say that the three hypotheses are verified in the SME environment. This confirms the theoretical approach which advocates the need for businesses, including SME's, to gain legitimacy with their stakeholders through a voluntary disclosure of information on SR and specifically on environmental issues.

Similarly, the environmental response made with specific actions and environmental protection management measures, that aim to minimize and compensate stakeholders for the impact on the environment in which they operate, seems to be significantly related to the degree of disclosure, and one can say that SME's carrying out responsible actions are the best in disclosure. However, this causal force, measured by the predictive power of one variable on another, is not too relevant, as was indicated before. We understand, therefore, that the relationship exists and is positive, confirming the theory and the proposed model, although there are many other reasons for the degree of disclosure of environmental information in SME's that have not been explored in this work and that deserve to be investigated as a continuation of this first approach to the topic.

Conclusions and limitations of the studyAs a conclusion and the principal contribution to environmental management, we can affirm that both the levels of SR information and the actions carried out explain to some extent the level of disclosure. This empirical evidence, in an area of SR research that has lacked studies on SME's, contributes to the generation of knowledge on the responsible behaviour of these firms. As demonstrated, SME's, which are under less pressure than large firms to carry out voluntary disclosure of social and environmental information, appear to be quite consistent. Thus, their disclosure, beyond the opportunistic demonstration effect, is directly related to their reality in the environmental sense, legitimizing them with their agents of interest.

Additionally it should be noted that the results of the proposed model should be interpreted bearing in mind the limitations of this type of analysis, primarily due to the selection of a sample, although large in our study, which was limited to a single Spanish Autonomous Community with results not directly extrapolatable to other environments that may differ greatly in their defining variables. Since the predominance of SME's is characteristic of the whole Spanish territory, as is the context of promoting SR, we can confirm the good behaviour of the model and indicate that the results have been very satisfactory. The results allow us to affirm that the information that small businesses get on SR plays a determinant role in their environmental response and the dissemination of it that they make. To be knowledgeable about the actions of SR that take place in the business, to be aware of the events, meetings, and conferences for the promotion and development of responsible practices and allocate time and resources to SR, constitute an antecedent of a firm's environmental response and disclosure conducted voluntarily and oriented to its stakeholders with the intention of gaining legitimacy with them. Additionally, the environmental response contributes to increasing their disclosure of information, both inside and outside the firm.

The inclusion of SR values in vision and strategy, active participation and cooperation with associations and organizations that promote it, can lead the firm towards more responsible behaviour with respect to the environment, translated into actions and voluntary business practices which are communicated through sustainability reports or other less demanding media. These results invite business organizations and public institutions not to neglect the work of awareness and sensitization of small businesses to SR. Every effort put into in promoting and training in SR will encourage small businesses to participate in the preparation of sustainability reports. We have noted that the literature on environmental management and performance had not addressed the focus of the present work. We thus consider that it complements and extends existing studies on SR and environment by taking a novel and currently very appropriate focus.

As regards the usefulness and the implications that this work may have for firms’ managers, we believe that the paper facilitates their identification and development of indicators that can measure the variables involved in diagnosing their position in the environment. In addition, as mentioned above, the results confirm that the information received on SR will play a role in their firm's environmental response, and later in the disclosures they make. When entrepreneurs are aware of this situation, they will surely want to follow the path of information, environmental response, and consequent disclosure of their actions as leading to the attainment of good results.

With regard to the scale of measurement, we can conclude firstly that it provides the possibility of a set of indicators tailored to SME's which can explain the relationship between the variables proposed. The research existing thus far did not offer any indicators that we could have considered for each of the constructs used, so that there was a need to look more deeply into the definitions themselves. Secondly, and based on the above, a starting point is provided for further work in this direction, investigating other variables that may potentially determine the degree of voluntary environmental disclosure conducted by SME's. We here are referring to different variables complementary to those used in the present model, and which can enrich knowledge about the motivations of SME's in the disclosure of their social and environmental results, allowing one to obtain an analytical framework of broader scope and applicability in favour of a more sustainable development.

This work was partially funded by the Regional Research ProjectPRI08A055, entitled “Diagnosis of Corporate Social Responsibility as a factor for innovation and development in Extremadura”, within the framework of the III PRI+D+I (2005–2008) and given to the INVE BUSINESS RESEARCH GROUP, registered in the list of groups of the Government of Extremadura; by the Regional Research Project PRIIB10030, “Survey of attitudes to Social Responsibility and measurement of the degree of interaction between Extremadura business and their agents of interest. A focus on small and medium enterprise”, within the framework of the IV PRI+D+I (2010–2013), and granted to the EXTREMADURA MARKETING AND OPERATIONS MANAGEMENT GROUP, registered in the list of groups of the Government of Extremadura; and finally by the grant in aid to Research Groups GR10041, received in 2010 under the IV Action Plan 2010–2014.

Freeman (1984:25) notes that these agents are “those groups or individuals who can affect or are affected by the achievement of the entity's objectives". Also, Johnson and Scholes (2001:193) indicate that they are “those individuals or groups whose goals depend on what the organization does and on whom, in turn, the organization depends".

One can include the following models of Environmental Management Systems: Responsible Care Programme (Responsible Action) (Canada, 1984); STEP (Strategies for Today's Environmental Partnership) (American Petroleum Institute, API, 1990); BS 7750 (Specifications for Environmental Management Systems, 1994); EMAS (Eco-Management and Audit Scheme, European Commission, 1995, 2001<***>); and ISO 14001 (Strategic Advisory Group on Environment, SAGE, 1996).

The research project IB10030 entitled "Attitudes to social responsibility to measure the degree of firms interaction with their stakeholders in Extremadura. A focus on small and medium enterprises" within the framework of the IV PRI+D+I (2010–2013) carried on by The Marketing and Operations Management Group in Extremadura (Merk@do) is being developed with firms in the sample. With a qualitative approach, with the focus group technique, and supported with software AtlasTi 7.0, the research is analysing perceptions of managers in Extremadura about SR.